Compardo, Wienstroer & Janes – Garrett Reeg, MBA, CFP®

High-net-worth families can face unique challenges when it comes to retirement accounts and estate planning. The combination of the Secure Act’s 10-year rule and high tax brackets for both individuals and trusts can create a perfect storm of tax inefficiency.

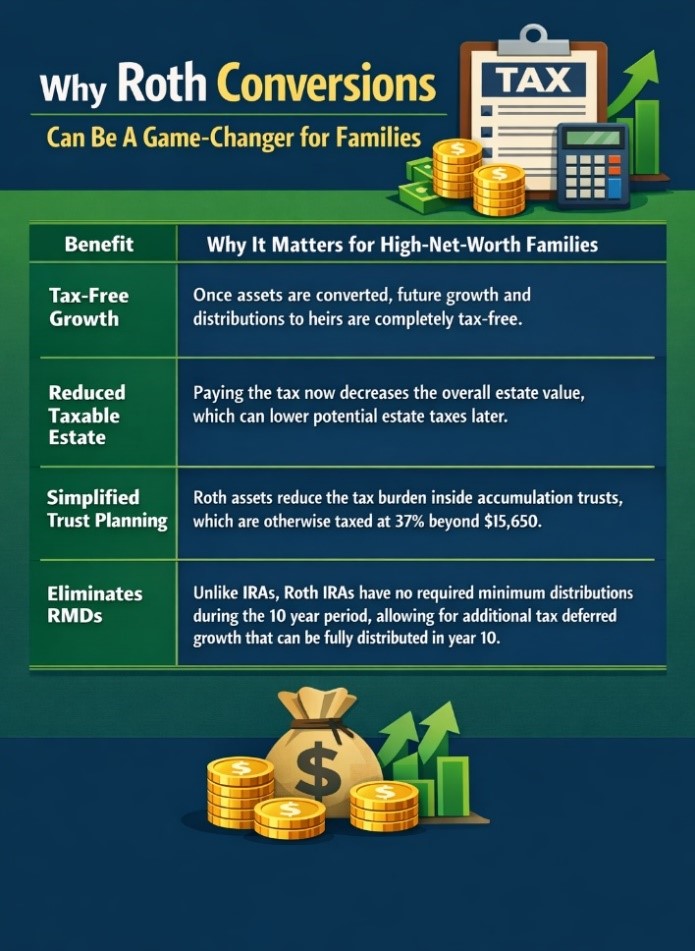

Many families have benefited from decades of tax-deferred growth inside traditional IRAs. Today, those IRAs often represent one of the largest embedded tax liabilities for the family. Without proactive planning, that liability is simply transferred to the next generation – often at less efficient tax rates.

One of the most effective strategies to combat this is a Roth conversion — intentionally paying taxes now to create tax-free growth for future generations.

Strategic Conversion Planning for High-Net-Worth Estates

- Evaluate Tax Brackets – Your own and your Beneficiaries

Roth conversion planning is highly customizable and rarely an all-or-nothing decision. Spreading conversions over several years can help manage exposure to higher tax brackets, or other unintended consequences. It is equally important to evaluate the likely tax situation of your beneficiaries. Under the SECURE Act, inherited IRAs generally need to be distributed within 10 years, often during beneficiaries’ high earning years. Comparing their projected tax brackets, based on expected inherited IRA balances and distributions, can materially impact the optimal conversion strategy. - Consider “Hidden” costs

Higher income from conversions can increase Medicare Part B/D premiums (IRMAA). Model this impact carefully. Recent tax law changes introduced potential tax benefits such as the Enhanced Senior Tax Deduction and expanded State and Local Tax (SALT) cap. Many of these benefits are subject to income phase-outs, further underscoring the importance of thoughtful planning when executing conversions. - Use Non-IRA Funds to Pay Taxes

Paying taxes from the conversion using non-IRA assets preserves the full converted balance for tax-free growth. However, the tax consequences of liquidating investments to fund the tax should be carefully evaluated, as they can materially impact the overall effectiveness. - Coordinate with Trusts

Align conversion strategy with trust structures to maximize protection and minimize tax drag. In many cases, naming a trust as the beneficiary of a Roth IRA can be beneficial. Because qualified Roth distributions are not subject to income tax, a trust can retain those assets without incurring trust-level tax rates, while still preserving creditor protection, control, and long-term estate planning objectives.

Example: Multigenerational Legacy Planning*

A couple with a $20M estate, including $6M in traditional IRA assets, converts $350,000 per year into a Roth IRA while staying within the 24% tax bracket.

Over time:

- The taxable estate decreases, potentially saving future estate taxes.

- Heirs receive Roth assets that grow tax-free and avoid forced taxable distributions.

- An accumulation trust retains full protection benefits without facing crushing trust tax rates.

For High-Net-Worth families, Roth conversions represent more than a tax strategy – they can also be a legacy-building tool. By paying taxes on your terms, you create flexibility and clarity for the next generation. When combined with thoughtful trust design and proactive planning, Roth conversions can transform retirement accounts from a tax liability into a tax-free, protected transfer of wealth, providing meaningful benefits across generations.

Contact me at greeg@monetagroup.com.

* This example is hypothetical and for educational purposes only. It does not reflect real results or the impact of taxes and fees.

© 2026 Advisory services offered by Moneta Group Investment Advisors, LLC, (“MGIA”) an investment adviser registered with the Securities and Exchange Commission (“SEC”). MGIA is a wholly owned subsidiary of Moneta Group, LLC. Registration as an investment adviser does not imply a certain level of skill or training. The information contained herein is for informational purposes only, is not intended to be comprehensive or exclusive, and is based on materials deemed reliable, but the accuracy of which has not been verified.

Trademarks and copyrights of materials referenced herein are the property of their respective owners. Index returns reflect total return, assuming reinvestment of dividends and interest. The returns do not reflect the effect of taxes and/or fees that an investor would incur. Examples contained herein are for illustrative purposes only based on generic assumptions. Given the dynamic nature of the subject matter and the environment in which this communication was written, the information contained herein is subject to change. This is not an offer to sell or buy securities, nor does it represent any specific recommendation. You should consult with an appropriately credentialed professional before making any financial, investment, tax or legal decision. An index is an unmanaged portfolio of specified securities and does not reflect any initial or ongoing expenses nor can it be invested in directly. Past performance is not indicative of future returns. All investments are subject to a risk of loss. Diversification and strategic asset allocation do not assure profit or protect against loss in declining markets. These materials do not take into consideration your personal circumstances, financial or otherwise.