Executive Summary

The first quarter of 2026 was defined by a sharp shift in narrative. What began the year with optimism around steady growth, supportive fiscal dynamics, and expected Federal Reserve rate cuts quickly gave way to a more uncertain environment dominated by geopolitical conflict and its downstream effects. The escalation of the US/Israel–Iran conflict, now several weeks in duration, introduced a meaningful supply shock to global energy markets and forced investors to reassess inflation, policy, and growth expectations in real time. Despite the noise, the underlying economy has remained relatively resilient and corporate fundamentals continue to provide support. Markets, however, have become more sensitive to headline risk, with a clear shift toward risk-off behavior late in the quarter. The result is a quarter where downside volatility returned, narratives shifted quickly, and investors were reminded how rapidly conditions can change.

Economic Update

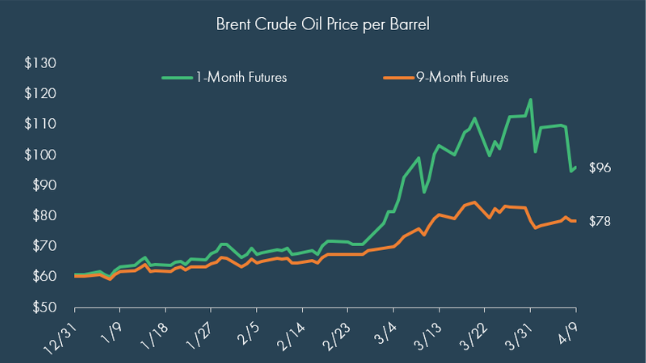

The dominant macro story this quarter was largely tied to the outbreak of outright war in the Middle East and emergence of supply-driven inflation upside risk. The conflict in the Middle East disrupted a critical global energy corridor, with the Strait of Hormuz experiencing significant military activity, significantly constraining both oil and liquified natural gas exports. The resulting supply shock has driven energy prices higher and raised concerns about broader inflation pressures, particularly if the disruption proves persistent. At the same time, markets have had to contend with additional crosscurrents, including evolving tariff policy, renewed attention on AI-driven labor dynamics, and a shifting outlook for US monetary policy.

As noted, inflation came back into focus after a period where it appeared the trend was toward flatlining to moderating. Historical precedent suggests that second waves of inflation are not uncommon following an initial spike, particularly when driven by energy shocks. The current environment reflects that risk, with near-term inflation expectations moving higher even as longer-term expectations remain more contained; this suggests markets still view the shock as potentially temporary as oil futures sit below current oil spot prices.

What is a definite known is the Federal Reserve will have its work cut for itself as it now faces a more complicated backdrop, even as the changing complexion of the Fed leadership and make-up remains in the backdrop. At the start of the year, expectations centered around multiple rate cuts in 2026, but this view has shifted meaningfully.

Market-implied expectations for monetary easing this year has largely dissipated, and there are even marginal expectations for tightening as policymakers balance emerging inflation pressures against signs of a moderating labor market.

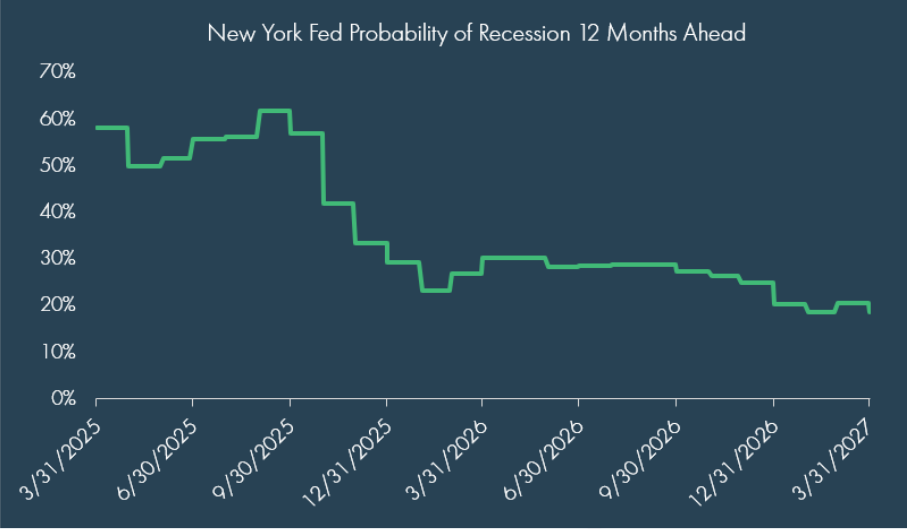

Importantly, for now, the U.S. economy has shown resilience in the face of these shocks. GDP growth expectations remain in the ~2.0–2.5% range across upcoming quarters, while manufacturing and services PMIs remain in expansion territory above 50. The labor market, while uneven month-to-month, continues to produce positive job growth overall and does not yet signal material deterioration. Additionally, recession, while modesty higher on the back of the initiation of the conflict in the Middle East, remained largely contained.

Structural factors also differentiate the current environment from past episodes of energy shocks. The U.S. economy is significantly less dependent on oil than in prior decades, with improved energy efficiency, increased domestic production, and diversification of energy sources helping to mitigate the impact. That said, risks remain. A prolonged disruption could still feed into broader price pressures and weigh on consumer sentiment and spending.

Alongside these developments, AI continues to shape the economic narrative, though its near-term impact appears more evolutionary than disruptive. Productivity gains are evident in sectors with higher AI adoption, but current evidence – despite concerns in the software sector – suggests AI is amplifying output rather than replacing labor at scale. Estimates suggest 6–7% of workers may ultimately be displaced, though the timing and magnitude remain very uncertain.

Markets

Market performance in the first quarter reflected a clear shift toward risk aversion, particularly as geopolitical tensions escalated in March. Market behavior followed a familiar pattern seen in prior geopolitical conflicts. Risk assets initially sold off, while the U.S. dollar strengthened. Real assets were certainly the bright spot and served their diversification role well. Infrastructure returned 8.12% and REITs gained 4.80% for the quarter, benefiting from their income characteristics and relative resilience during periods of equity market stress. That said, gold did not provide the typical diversification benefit, behaving more like a risk asset amid strong retail liquidation.

Volatility increased across both equities and fixed income, though levels remained below those seen during more acute stress periods such as 2022. U.S. large cap equities, as measured by the S&P 500, declined -4.33% for the quarter, while small caps (Russell 2000) posted a modest gain of 0.89%. Within U.S. equities, dispersion was notable between value and growth stocks. Value outperformed growth across market capitalizations as the energy sector benefited from oil prices, with higher-multiple large cap growth down -9.78% year-to-date. International equities were mixed but generally weaker, with MSCI EAFE down -1.24% and Emerging Markets roughly flat at -0.17%.

Fixed income markets were pressured by rising rates. The Bloomberg U.S. Aggregate Bond Index declined -0.05% for the quarter as Treasury yields moved higher across the curve, with the 10-year rising to 4.32% (+15 bps) and the 2-year to 3.80% (+32 bps). The yield curve, which had been deeply inverted, began to normalize as longer-term rates moved higher.

Credit spreads widened modestly, particularly in high yield, though they remain well below levels typically associated with economic stress. Investment grade corporates fell -0.54% and high yield declined -0.50%. This suggests markets are repricing risk but not yet signaling significant concern about credit quality.

Encouragingly, corporate fundamentals remain supportive. Forward earnings growth expectations for the S&P 500 sit around 17%, indicating that despite geopolitical and macro uncertainty, underlying business performance has held up.

Ultimately, markets continue to price in a relatively contained and potentially shorter-duration conflict, though outcomes remain highly path dependent as meaningful day-to-day shifts in sentiment are a common occurrence currently.

Summary

The first quarter served as a reminder of how quickly market narratives can shift. What began as a continuation of the prior year’s steady growth story transitioned into a more complex environment shaped by geopolitical risk, renewed inflation concerns, and evolving policy expectations.

There are credible arguments on both sides of the outlook. On one hand, the economy remains resilient, earnings expectations are strong, and structural factors — such as reduced energy dependence — can help buffer the impact of external shocks. On the other hand, a prolonged disruption in energy markets could sustain inflation pressures, limit the Fed’s monetary policy flexibility, and weigh on global economic growth.

To date, markets have responded accordingly, with increased volatility and a more cautious tone reflected in lower asset prices. Yet, the broader pattern remains consistent with past episodes: periods of uncertainty tend to produce sharp reactions, but fundamentals ultimately drive longer-term outcomes.

This is where discipline matters most. Portfolios are built with the expectation that environments like this will occur. Diversification has once again demonstrated its value, with real assets and fixed income helping to offset equity weakness. Attempting to reposition portfolios based on short-term developments risks missing the eventual recovery, particularly when outcomes remain uncertain.

Staying invested, maintaining balance, and focusing on long-term objectives remain an effective approach. Periods like this are uncomfortable, but they are also part of the process that long-term investors are prepared to navigate.

Disclosures

© 2026 Advisory services offered by Moneta Group Investment Advisors, LLC, (“MGIA”) an investment adviser registered with the Securities and Exchange Commission (“SEC”). MGIA is a wholly owned subsidiary of Moneta Group, LLC. Registration as an investment adviser does not imply a certain level of skill or training. The information contained herein is for informational purposes only, is not intended to be comprehensive or exclusive, and is based on materials deemed reliable, but the accuracy of which has not been verified.

Trademarks and copyrights of materials referenced herein are the property of their respective owners. Index returns reflect total return, assuming reinvestment of dividends and interest. The returns do not reflect the effect of taxes and/or fees that an investor would incur. Examples contained herein are for illustrative purposes only based on generic assumptions. Given the dynamic nature of the subject matter and the environment in which this communication was written, the information contained herein is subject to change. This is not an offer to sell or buy securities, nor does it represent any specific recommendation. You should consult with an appropriately credentialed professional before making any financial, investment, tax or legal decision. An index is an unmanaged portfolio of specified securities and does not reflect any initial or ongoing expenses nor can it be invested in directly. Past performance is not indicative of future returns. All investments are subject to a risk of loss. Diversification and strategic asset allocation do not assure profit or protect against loss in declining markets. These materials do not take into consideration your personal circumstances, financial or otherwise.

Definitions

The S&P 500 Index is a free-float capitalization-weighted index of the prices of approximately 500 large-cap common stocks actively traded in the United States.

The Russell 2000® Index is an index of 2000 issues representative of the U.S. small capitalization securities market.

The MSCI EAFE Index is a free float-adjusted market capitalization index designed to measure the equity market performance of developed markets, excluding the U.S. and Canada.

The MSCI Emerging Markets Index is a float-adjusted market capitalization index that consists of indices in 21 emerging economies.

Bloomberg U.S. Treasury Bond Index includes public obligations of the US Treasury, i.e. US government bonds. Certain Treasury bills are excluded by a maturity constraint. In addition, certain special issues, such as state and local government series bonds (SLGs), as well as U.S. Treasury TIPS, are excluded.

The Bloomberg U.S. Aggregate Bond Index is an index, with income reinvested, generally representative of intermediate-term government bonds, investment grade corporate debt securities and mortgage-backed securities.

The Bloomberg US Corporate High Yield Bond Index measures the USD-denominated, high yield, fixed-rate corporate bond market. Securities are classified as high yield if the middle rating of Moody’s, Fitch and S&P is Ba1/BB+/BB+ or below. Bonds from issuers with an emerging markets country of risk, based on the indices’ EM country definition, are excluded.

The FTSE Nareit All Equity REITs Index is a free-float adjusted, market capitalization-weighted index of U.S. equity REITs. Constituents of the index include all tax-qualified REITs with more than 50 percent of total assets in qualifying real estate assets other than mortgages secured by real property.

The S&P Global Listed Infrastructure Index measures the performance of global companies that are engaged in infrastructure and related operations. It provides liquid and tradable exposure to 75 companies from around the world that represent the listed infrastructure universe. To create diversified exposure, the index includes three distinct infrastructure clusters: utilities, transportation and energy.