Compardo, Wienstroer & Janes – Garrett Reeg, MBA, CFP®

For many families, particularly those who have high net worth, retirement accounts can often make up a significant portion of total wealth. These accounts are designed to grow tax deferred, but recent legislative changes including the SECURE Act of 2019, later expanded under SECURE 2.0 (2022), introduced many rules that include how certain retirement accounts are treated upon death. The new rules also include the ability to boost retirement savings by expanding access to plans and increasing contribution opportunities. The rules governing inherited IRAs have changed and may create different tax outcomes depending on your family’s situation.

Without careful planning, these rule changes can result in substantial tax liabilities for the next generation, reducing the wealth you’ve worked a lifetime to build. Understanding these new rules is the first step toward protecting your legacy.

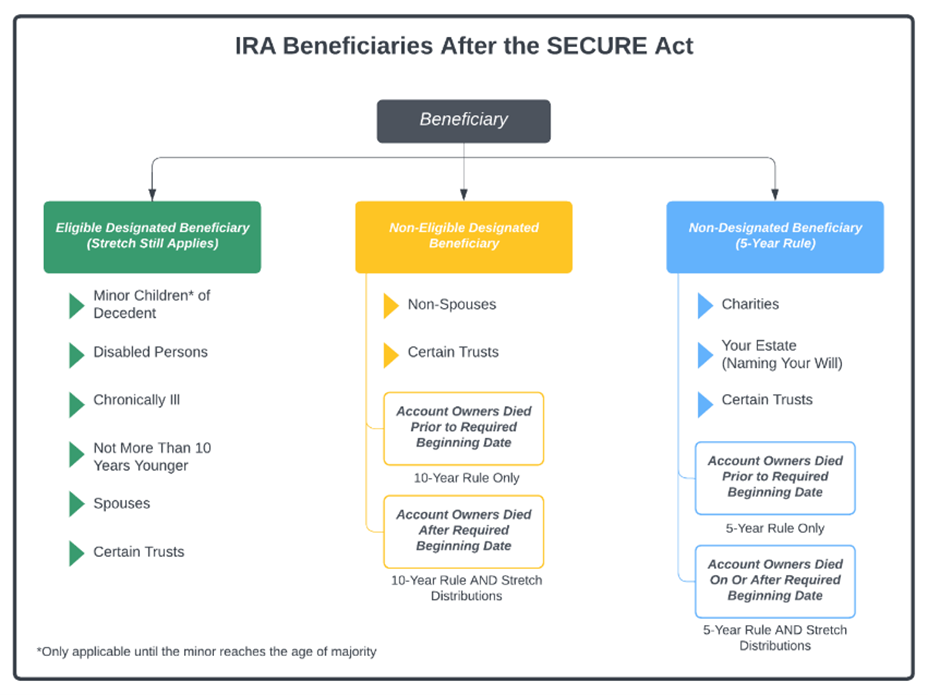

Historically, beneficiaries could “stretch” IRA distributions over their own life expectancy, minimizing annual taxes and allowing assets to grow for decades. The Secure Act eliminated this option for most non-spouse beneficiaries.

Now, inherited IRAs generally must be fully distributed within 10 years of the account owner’s death. In many cases, required annual distributions may also apply during that period.

The compressed timeline can create several challenges for many families.

- Peak earning years: Many heirs inherit in their 40s, 50s, or 60s — their highest earning years — which can push inherited distributions into higher tax brackets.

- Compressed timelines: IRA balances must now be liquidated over 10 years, accelerating taxes in a much shorter timeframe.

- Unexpected complexity: Higher income can trigger higher Medicare premiums, impact capital gains tax rates, and impact eligibility for other deductions or credits.

Example:

A couple passes away in their late 80s with a $5 million IRA. Their 55-year-old daughter, a senior executive, must now withdraw the entire IRA balance within 10 years. Adding $500,000 in annual withdrawals to her existing income could push her into the highest federal tax bracket (37%), resulting in significant tax implications. Prior to these changes, she could have stretched the distributions over her life expectancy, resulting in smaller annual withdrawals and deferring larger distributions until potentially lower-income retirement years*.

What Can You Do? Here are Some Strategic Considerations for Wealth Transfer

HNW families can minimize potential issues with proactive planning:

- Plan Timing of Withdrawals

Encourage beneficiaries to strategically schedule distributions in lower-income years or retirement years within the 10-year window. - Consider Roth Conversions

Converting traditional IRA assets to Roth IRAs during your lifetime can help shift future growth into a tax-free environment. With an accelerated timeline of distributions, you may be able to convert your IRA to a Roth at the same or lower tax rate than your beneficiaries would otherwise face. This can be especially attractive in taxable estate situations. - Evaluate Beneficiary Strategy

While it can add complexity, naming Trusts as a beneficiary (rather than your children outright) may make sense. IRAs are also great assets to fulfil charitable desires, if you have them. - Engage a Multidisciplinary Team

Coordinate with wealth advisors, estate attorneys and tax professionals to integrate IRA planning with your broader estate strategy.

The new rules within the Secure Act can create challenges for many families, particularly those who have high net worth. With larger balances and higher marginal tax rates at play, the consequences of poor planning can be costly. By addressing these rules now, you can protect your heirs from a potentially significant, unnecessary tax burden — and ensure that your legacy supports future generations.

* This example is hypothetical and for educational purposes only. It does not reflect real results or the impact of taxes and fees.

Contact me at greeg@monetagroup.com.

© 2026 Advisory services offered by Moneta Group Investment Advisors, LLC, (“MGIA”) an investment adviser registered with the Securities and Exchange Commission (“SEC”). MGIA is a wholly owned subsidiary of Moneta Group, LLC. Registration as an investment adviser does not imply a certain level of skill or training. The information contained herein is for informational purposes only, is not intended to be comprehensive or exclusive, and is based on materials deemed reliable, but the accuracy of which has not been verified.

Trademarks and copyrights of materials referenced herein are the property of their respective owners. Index returns reflect total return, assuming reinvestment of dividends and interest. The returns do not reflect the effect of taxes and/or fees that an investor would incur. Examples contained herein are for illustrative purposes only based on generic assumptions. Given the dynamic nature of the subject matter and the environment in which this communication was written, the information contained herein is subject to change. This is not an offer to sell or buy securities, nor does it represent any specific recommendation. You should consult with an appropriately credentialed professional before making any financial, investment, tax or legal decision. An index is an unmanaged portfolio of specified securities and does not reflect any initial or ongoing expenses nor can it be invested in directly. Past performance is not indicative of future returns. All investments are subject to a risk of loss. Diversification and strategic asset allocation do not assure profit or protect against loss in declining markets. These materials do not take into consideration your personal circumstances, financial or otherwise.