By Benjamin Trujillo, Senior Advisor

The COVID-19 pandemic has been a difficult time for everyone. It has also created a unique atmosphere for estate planning. The unprecedented current economic environment provides a window of opportunity to leverage undervalued equities and low-interest rates into significant estate and gift tax savings.

There are times when we want to gift money to family members; however, loans may be preferable to outright gifts. The choice of a loan or gift is particularly important when there are concerns about treating family members equally or tax planning reasons to forego gifting.

Intra-family loans are useful estate planning tools, especially in low-interest-rate environments. To ensure the IRS does not treat an intra-family loan as a gift, it is essential we follow specific guidelines, most importantly that we charge an interest rate equal to at least the relevant AFR.

Each month the Internal Revenue Service (IRS) releases the Applicable Federal Rate (AFR). The AFR is the lowest rate of interest which may be charged before a loan is considered a gift. The AFR also varies depending on the length of the loan:

- Short-term – Up to three years

- Mid-term – Three to nine years

- Long-term – More than nine years

As the Federal Reserve continues to reduce rates, the AFR has reached historic lows. For the month of June at only .43% and 1.01% respectively, mid-term and long-term rates are the lowest seen since 1989. Conversely, the estate and gift tax exemption has grown to reach a historic high of $11,580,000 per person.

Intra-family loans work particularly well for a category of estate planning strategies referred to as estate freezes. Estate freeze techniques work by transferring from your estate those assets which are expected to appreciate. This transfer effectively freezes the value of the transferred assets for federal estate tax purposes, while removing their growth from your estate. The unprecedented current economic environment provides a window of opportunity to leverage undervalued equities and low-interest rates into significant estate and gift tax savings. The IRS recently released July AFRs and interest rates are increasing so now is the time to act.

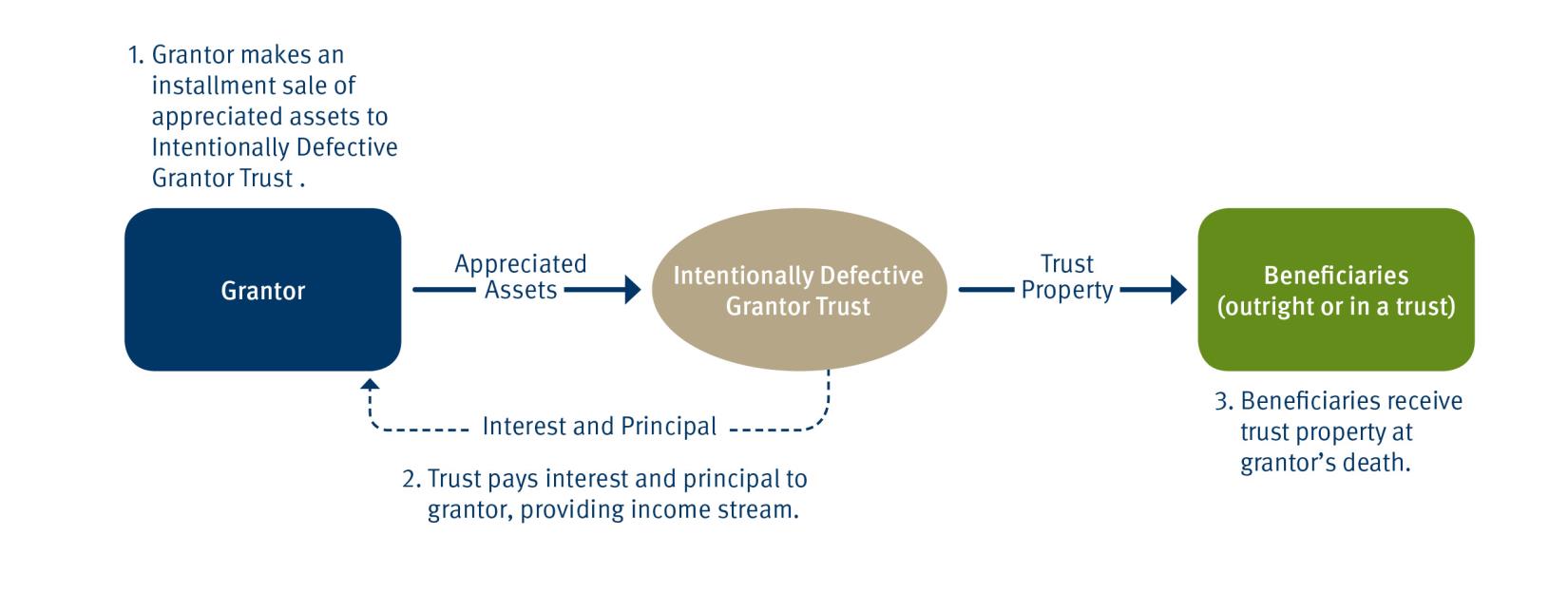

One particularly advantageous freeze technique to consider in low-interest-rate, low-market-value conditions is a sale to an Intentionally Defective Grantor Trust (IDGT). An IDGT is an irrevocable trust structured to allow the grantor to be considered the owner of the trust assets for income tax purposes while removing the assets from the grantor’s estate for federal estate tax purposes. The result is the grantor continues to pay the income taxes generated by the trust property. Once the transfer is complete, the grantor’s estate no longer includes the assets (and any subsequent appreciation). This transfer serves to further reduce the grantor’s estate for estate tax purposes while ensuring that any future appreciation of the assets after the transfer will occur outside of the grantor’s estate.

Take, for example, a sale of $1,000,000 of equities to an IDGT in exchange for a promissory note. Currently, most equities are trading well off their historic highs. If you are bullish in the long-term and expect markets to return to their pre-COVID pricing, and when considered in the context of historically low-interest rates, the cost of a sale is minimal. No capital gain is recognized on the initial sale to the IDGT, and the interest due on the promissory note may be less than 1%.

If the market returns to normal, the effect is to have easily removed 15% to 20% of the value of the equities (calculated using their recovered price less the interest paid on the promissory note) from your estate for federal estate tax purposes. Later, if those equities are liquidated and generate a capital gain, the grantor pays the tax, removing even more assets from the estate.

This can be done with minimal use of your lifetime estate tax exemption. Other strategies can be employed to increase the efficiency of this strategy by further discounting the value of the underlying equities. Even if an estate freeze strategy does not make sense for your needs, consider an intra-family loan to take advantage of today’s exceptionally low-interest rates.

Advisors from Compardo, Wienstroer, Conrad & Janes are ready to discuss the details of these strategies and how they may apply to your specific situation. You can contact us here.