The DUFF TORNEY Team

If You Receive Restricted Stock or Stock Options, Consider This Tax-Saving Move

Michael Torney, CFP, J.D., LL.M.

Paying taxes when receiving stock grants instead of waiting for shares to vest could help you save thousands of dollars.

Corporate executives often receive restricted stock or stock options as part of their total pay. But it’s possible to save a significant amount of money by taking advantage of section 83(b), a somewhat obscure, but important section of the Internal Revenue Service Code.

Federal law allows individuals to pay taxes in the same year the stock awards are granted, even though the stock hasn’t yet vested. This is done through what’s called an 83(b) election. Why would an investor do this? The stock price at the grant date may be much lower than when the stock vests and is sold; this means the taxes owed can be tens, even hundreds of thousands of dollars less if paid when the stock award is granted. This special 83(b) election can be used for stock awards that have not fully vested, such as restricted stock and stock options.

How Restricted Stock and Stock Options Work

Restricted stock are shares of your company’s stock that will vest at a future date. For example, if you are granted 10,000 shares of stock in January 2023, but the shares don’t vest for three years, you won’t own these shares without restrictions until January 2026. If you anticipate the stock price will be higher in January 2026, you can minimize the tax bill by filing an 83(b) election and paying taxes on the value of the stock in January 2023. That means you’ll pay less in tax if these shares appreciate in value. Stock options are usually either incentive stock options (ISO) or non-qualified stock options (NSO). Stock options give employees the right to buy or exercise shares of company stock at a pre-set price. ISO and NSO options are taxed differently. Both of these options present some tax-saving opportunities with an 83(b) election, though the planning varies for each; 83(b) tax strategies for NSO and ISO options are covered in a different blog. Let’s look at how you can save taxes on your restricted stock using an 83(b) election.

Restricted Stock and an 83(b) Election

If you receive restricted stock, here’s an example of how an 83(b) election can save money. On January 1, 2018, a senior-level executive at Apple, Inc., is awarded 10,000 shares of company stock that will vest in three years. The price at that time was $39.80, so the 10,000 shares are valued at $398,000. If the executive does not make the 83(b) election, there is no tax due. Three years later, on Jan. 1, 2021, Apple’s stock price rose to $130.39. The executive’s shares – which they now own outright – are now worth $1,303,900. There is now ordinary income tax due on $1,303,900. If instead, the executive made the 83(b) election, they would have included the $398,000 as part of their income when filing 2018 taxes. Here’s why that’s important. No taxes are due upon vesting since they have already been paid. Because the stock is now valued at over $900,000 more than when it was granted, the additional $900,000 of gain is deferred.

Selling Your Stock

It’s January 2, 2022. The executive decides to sell their shares one year and one day after the shares vest. The executive waits this long because a person must keep their shares for more than one year prior to selling for any profit to be taxed at more preferential capital gains rates. However, if the 83(b) election was made, then the holding period began at the grant date when the restricted stock compensation was included in income. In this example, the executive would not have needed to wait the extra year to be taxed at long-term capital gain tax rates. At this point, the shares are valued at $1,737,700 – nearly $1.3 million more than when the stock was granted. But once the stock is sold, the executive is only responsible for capital gains taxes – a maximum of 20 percent of profits – rather than the rate for ordinary income taxes, which can be as high as 37 percent. The tax will be applied on any gains above the taxpayer’s cost basis. If the 83(b) election was made, the cost basis is $398,000. If the election was not made, the cost basis is $1,303,900.

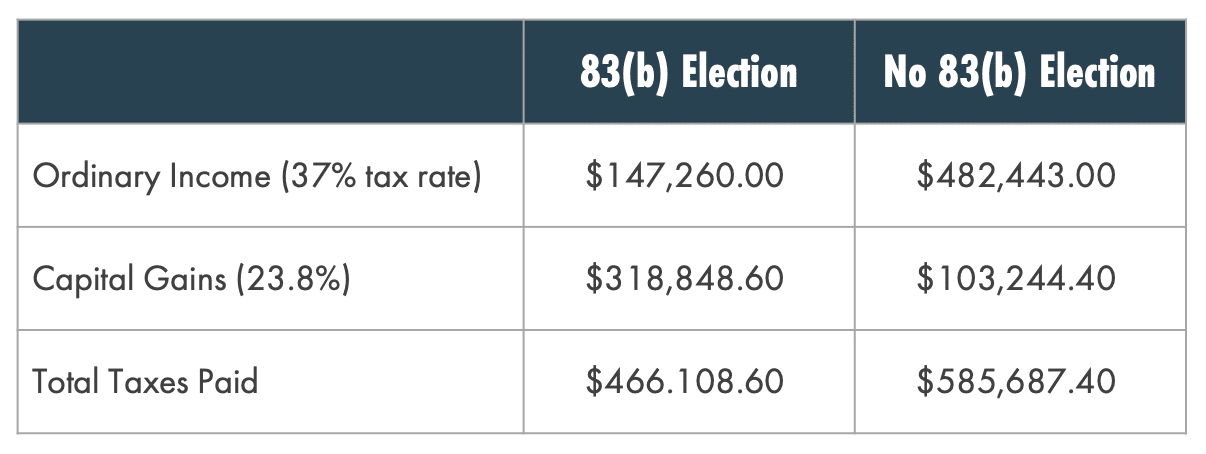

How the Tax Math Stacks Up

We need to make some assumptions about our hypothetical taxpayer to play out taxes. Let’s say he lives in Florida, a state with no state income tax. And he’s in the 37% federal tax bracket (for simplicity, we will ignore the Social Security and Medicare taxes on the ordinary income, which are additional savings in favor of the 83(b) election in this example). This means he will pay 23.8% in capital gains taxes for 2023 (20% capital gain plus 3.8% net investment income tax).

No 83(b) Election: If the executive did not make the 83(b) election, he pays 37% of $1,303,900 (taxes due at stock vesting) and an additional 23.8% of $433,800 ($1,737,700 minus $1,303,900 cost basis). The total tax due is $585,687.40.

83(b) Election: If the executive did make the 83(b) election, he pays 37% of $398,000 (taxes due at stock grant) and an additional 23.8% of $1,339,700 ($1,737,700 minus $398,000 cost basis). Total tax due is $466,108.60.

When It Makes Sense to File an 83(b)

Filing a section 83(b) election makes sense for some people, but not for everyone. Consider making an 83(b) election if:

- You receive restricted stock with a low market value per share at the time of grant or options with a strike price that is close or equal to the market value per share

- You can afford to pay any costs associated with the election;

- You believe the value of the company’s stock will increase significantly over time;

- The risk that you will forfeit the stock is small. For example, you expect to be with the company until the stock vests.

- You believe you will be able to sell your stock later at a higher price

For restricted stock, the election must be made within 30 days of receiving the award. For options, the election must be made within 30 days of exercise. You should confirm that your company’s plan allows you to exercise options before they vest. Making a decision on whether to file an 83(b) election can be a difficult choice. If you have questions about this topic or other issues involving stock compensation, contact our team at DuffTorneyteam@monetagroup.com. We offer a free consultation to discuss how a comprehensive financial plan could help serve you well now and during retirement.

© 2024 Advisory services offered by Moneta Group Investment Advisors, LLC, (“MGIA”) an investment adviser registered with the Securities and Exchange Commission (“SEC”). MGIA is a wholly owned subsidiary of Moneta Group, LLC. Registration as an investment advisor does not imply a certain level of skill or training. The information contained herein is for informational purposes only, is not intended to be comprehensive or exclusive, and is based on materials deemed reliable, but the accuracy of which has not been verified. Trademarks and copyrights of materials referenced herein are the property of their respective owners. Index returns reflect total return, assuming reinvestment of dividends and interest. The returns do not reflect the effect of taxes and/or fees that an investor would incur. Examples contained herein are for illustrative purposes only based on generic assumptions. Given the dynamic nature of the subject matter and the environment in which this communication was written, the information contained herein is subject to change. This is not an offer to sell or buy securities, nor does it represent any specific recommendation. You should consult with an appropriately credentialed professional before making any financial, investment, tax or legal decision. An index is an unmanaged portfolio of specified securities and does not reflect any initial or ongoing expenses nor can it be invested in directly. Past performance is not indicative of future returns. All investments are subject to a risk of loss. Diversification and strategic asset allocation do not assure profit or protect against loss in declining markets. These materials do not take into consideration your personal circumstances, financial or otherwise.