Markets cruised through the halfway point of 2024 and as we take stock of the year-to-date numbers, we find ourselves with the S&P 500 up 15.3%, the Nasdaq Composite Index up 18.6%, and the Dow Jones Industrial Average Index up 4.8%. These numbers reflect a big picture view of investor optimism and improving economic conditions around the world: the global economy is stabilizing with real global GDP growth expected to post a solid 3.0% for the year. Within the headline numbers though, there is a lot of noise. After seeing the headline S&P 500 numbers, many investors find themselves perplexed that their portfolio has failed to keep up with “the broader market”. Additionally, the strong returns from the S&P 500 Index have, in almost equal proportion, generated concerns that (1) one’s portfolio “does not have enough US Large Cap” on the belief that the performance will continue or (2) that one’s portfolio “has too much US Large Cap” on concerns that we are in a 1999-like bubble that could pop at any moment.

In this quarterly report, we’ll seek to dissect the numbers and find the “devil in the details”, while not losing sight of the big picture that warrants excitement: technology, science, and medicine are all colliding; investment dollars are flowing through to the real economy and life-changing advances are happening. As always, there are risks in investing, but there is also plenty to be excited about.

Let’s dive in.

Economic Update

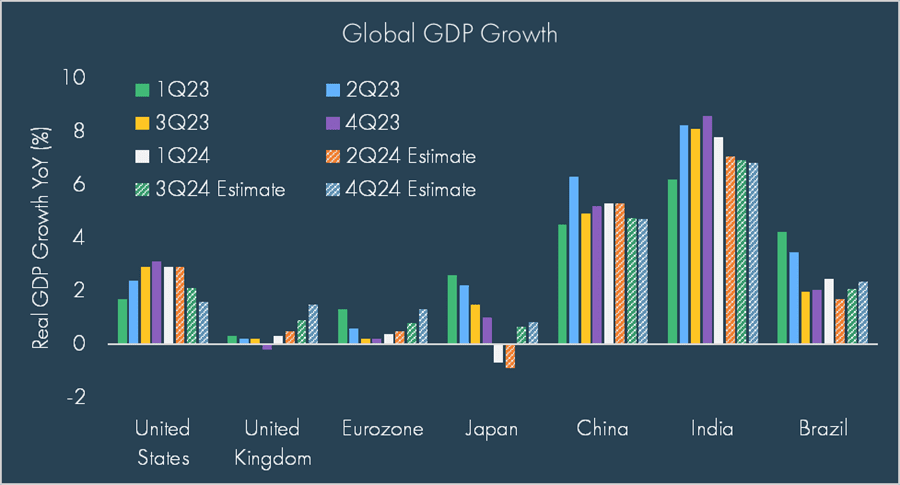

A quick look around the world shows that not much has changed in the economic narrative: global growth continues to chug along while some of the more concerning areas such as Europe and China appear to be experiencing pockets of green shoots, with the former welcoming rate cuts from the European Central Bank (ECB) and Swiss National Bank in response to falling inflation. Recession fears appear to have faded into the background, as a Bloomberg story count has shown the lowest number of “recession” hits since the fourth quarter of 2021 – the lowest on record.

The U.S. economy continues to be the growth engine of developed markets, though some slowdown is expected as stretched consumers, the backbone of the economic growth, are starting to show signs of fatigue and wariness of higher prices, despite a slowdown in inflation. However, an economic slowdown does not necessarily equate to a contraction, as economists expect real US GDP growth to slow to 2.3% in 2024.

The key to this consumer “strength” has been a strong labor market, which continues to print monthly job gains above 200,000 and an employment rate hovering near “full employment” at 4.1% as of June. The participation rate has increased alongside a drop in job openings, helping bring a better balance to the labor picture. Yet under the hood, these employment numbers may not be as strong as one would hope, with the bulk of the job gains coming from part-time jobs in government and healthcare sectors.

The other side of the economic equation, at least as far as the Federal Reserve is concerned, is inflation. Globally, inflation has come down from post-COVID highs and the US is no exception. However, nuances have begun forming, as most clearly evidenced by the ECB’s rate cut in June – the first time since its creation in 1999 that the ECB cut rates before the Fed. With June’s inflation print coming in at 3.0% year-over-year, there is clearly some work to be done to getting back down to the Fed’s long-term target of 2% average inflation, though this most recent inflation print was taken as a significant leap towards that goal. Additionally, the psychological impact of inflation on consumers over the last few years cannot be discounted. While the Fed believes inflation is on its way to their targets – and so do markets given five-year breakeven rates of 2.3% at quarter end – May’s University of Michigan Consumer Report indicates that the average American consumer expects inflation to run at 5% for the next five years.

This mixed economic data threw a wrench in the market’s expectations of potentially five or more rate cuts from the Fed at the beginning of 2024. At their June meeting, the Fed emphasized their commitment to following the data and accordingly adjusted their expectations for where rates would be at year end – indicating an expectation for just one rate cut in 2024. Markets have been whipsawed a bit by the changing data and narrative, but, as we write, remain optimistic, pricing in 2-3 cuts with the first cut expected in September.

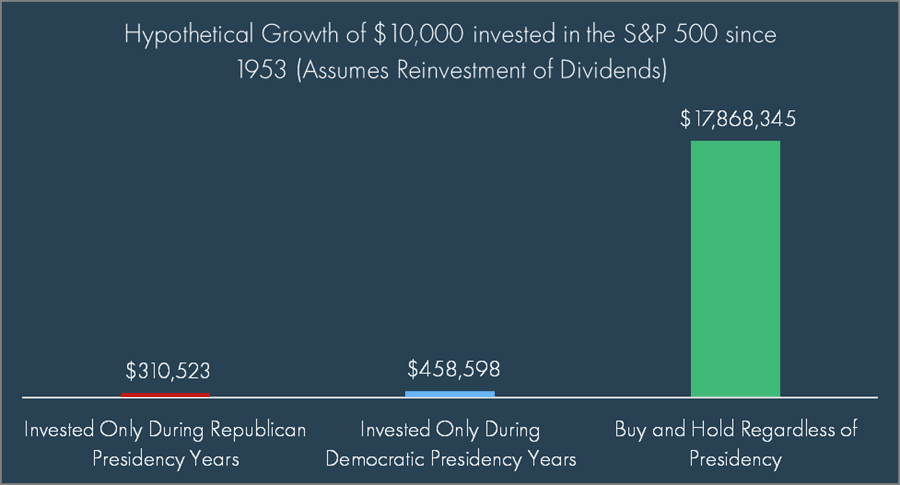

Of course, this mixed picture is coming to a head in the US, which will hold its quadrennial presidential election in November. After questions arose from President Joe Biden’s debate showing at the end of June, what was once a neck and neck race appears to have swung solidly in favor of the Republicans and their presumptive candidate Donald Trump. Who gets elected this November does matter for policies, and as we’ve seen in countries around the world – such as South Africa, Mexico, India, and France – election surprises can clearly have an impact on markets in the short term. Yet, history has shown that over time, it is economic fundamentals, not politics that drive markets long-term.

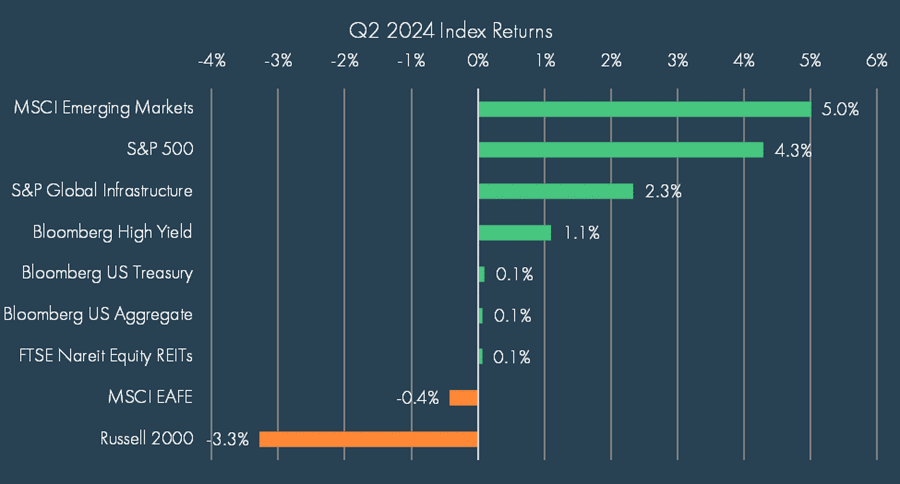

Speaking of markets! Despite political and economic concerns, the S&P 500 punched in another excellent quarter, returning 4.3% in Q2 and bringing its year-to-date return up to 15.3%. Such strong numbers can cause one to forget that the S&P 500 fell more than 4% in April, as a reset in interest rate expectations sent US markets broadly lower before artificial intelligence (AI) optimism, strong earnings, and a less hawkish Fed drove rallies in May and June.

As the chart above highlights, the second quarter was a mixed bag of results. While Emerging Markets performed well due to strength in Taiwan, India, and China, the dominating story revolved around one asset class outperforming most others by a wide margin. That asset class, of course, was US Large Cap, or more specifically, US Large Cap Growth stocks, which benefitted from the AI hype train as key AI names, such as Nvidia, smashed through sky-high earnings expectations. On the flipside, US small cap stocks, or more specifically, US Small Cap Value stocks, performed poorly, unable to recover from the “higher-for-longer” rate mantra. Fixed income posted small gains as the carry from higher yields offset the higher rates

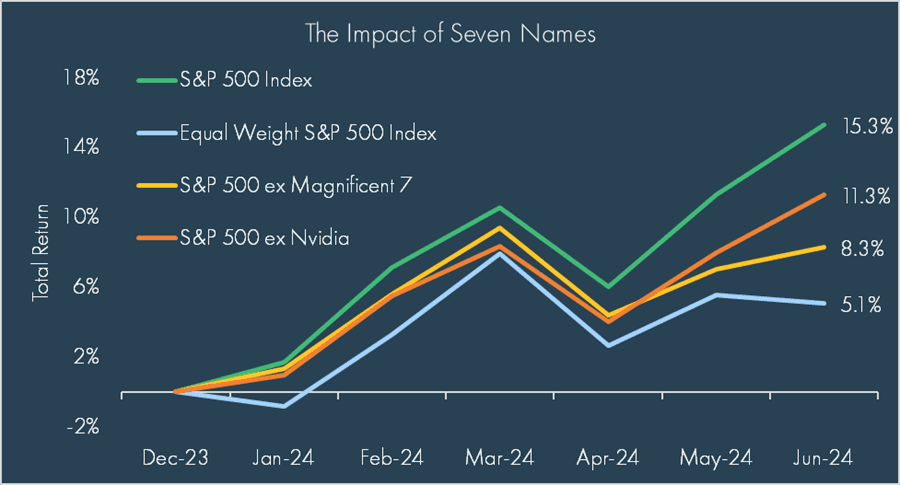

So, what drove the strong outperformance of the S&P 500? Namely, AI stocks. The famed Magnificent 7[1] took a bit of a backseat in Q1 with certain names such as Tesla and Apple performing poorly on weaker sales expectations, but the group was back in vogue in Q2 as the Magnificent 7 group posted an average return of 15.8% in the 2nd quarter.

The dominance of these names can be illustrated in many different ways. Most simply, we can look at the performance of an equal-weighted S&P 500 index (+5.1% YTD) vs the market-cap weighted S&P 500 index (+15.3% YTD), where the 10 largest names make up roughly 37% of the total index. More specifically, we can also look at a cap-weighted S&P 500 Index without the Magnificent 7 names, which would only be up 8.3% YTD.

When it comes to the impact of AI, it is important to note that we are still in the infancy stage. Research from Goldman Sachs showed that stocks benefitting from AI are those involved in the buildout, such as companies building the chips, data centers, servers, and infrastructure needed to make the AI hope a reality. The market knows this, and has rewarded these types of companies. Markets have also rewarded companies who can directly enhance revenue from AI, including companies such as Meta, Uber, and Squarespace. Meanwhile, companies who simply stand to benefit from AI productivity gains via cost savings and greater efficiencies, have yet to enjoy benefits via significant market appreciation.

This distinction is important, since it harkens back to the internet craze of the 1990s. While valuations are not as stretched and the AI winners today do generate sustainable cash flows, the lessons learned from companies like Cisco and Intel in the 1990s should give investors pause before pilling all-in on the winners today. AI promises significant benefits to society; indeed, we are already seeing some of these benefits as entities use AI to improve chat bots, enhance basic skillsets, predict when machinery will break down, identify the shape of DNA replication enzymes, find new classes of antibiotics, and much more. Yet there will also be many losers; companies will spend billions on technology that ultimately fails to deliver the expected return-on-investment (ROI). The market is not universally rewarding a company for “incorporating AI”, but they are rewarding companies who are generating cashflow from AI.

Are we reliving 1995 or 1999? Probably neither, though, there are similarities to both periods. We take comfort in the fact that while optimistic, there does not appear to be broad “irrational exuberance” at play currently, though there may be some specific segments where the market is overly enthused at minimum. Ultimately, any portfolio that diversifies away from the handful of AI winners has likely lagged the S&P 500 over the last 18 months. However, beating the best performing asset class in any given year should never be the goal of a diversified portfolio. At Moneta, we seek to build all-weather portfolios that, in alignment with one’s risk tolerance, can withstand shocks like the one following 1999 or participate in rallies like the one following 1995, providing the best possible chance of meeting one’s investment goals.

[1] The Magnificent 7 refers to the following seven stocks: Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia, and Tesla

Contributors

Andrew Kelsen – Chief Investment Officer

Chris Kamykowski, CFA, CFP® – Head of Investment Strategy and Research

Tim Side, CFA – Investment Strategist

Rich McDonald – Head of Portfolio Management and Fixed Income

Disclosure

© 2024 Advisory services offered by Moneta Group Investment Advisors, LLC, (“MGIA”) an investment adviser registered with the Securities and Exchange Commission (“SEC”). MGIA is a wholly owned subsidiary of Moneta Group, LLC. Registration as an investment adviser does not imply a certain level of skill or training. The information contained herein is for informational purposes only, is not intended to be comprehensive or exclusive, and is based on materials deemed reliable, but the accuracy of which has not been verified.

Trademarks and copyrights of materials referenced herein are the property of their respective owners. Index returns reflect total return, assuming reinvestment of dividends and interest. The returns do not reflect the effect of taxes and/or fees that an investor would incur. Examples contained herein are for illustrative purposes only based on generic assumptions. Given the dynamic nature of the subject matter and the environment in which this communication was written, the information contained herein is subject to change. This is not an offer to sell or buy securities, nor does it represent any specific recommendation. You should consult with an appropriately credentialed professional before making any financial, investment, tax or legal decision. An index is an unmanaged portfolio of specified securities and does not reflect any initial or ongoing expenses nor can it be invested in directly. Past performance is not indicative of future returns. All investments are subject to a risk of loss. Diversification and strategic asset allocation do not assure profit or protect against loss in declining markets. These materials do not take into consideration your personal circumstances, financial or otherwise.

Definitions

Real gross domestic product is the inflation adjusted value of the goods and services produced by labor and property located in the United States. Real GDP forward estimates are the Bloomberg weighted averages of sell side analyst forecasts.

The S&P 500 Index is a free-float capitalization-weighted index of the prices of approximately 500 large-cap common stocks actively traded in the United States.

The Russell 2000® Index is an index of 2000 issues representative of the U.S. small capitalization securities market.

The MSCI EAFE Index is a free float-adjusted market capitalization index designed to measure the equity market performance of developed markets, excluding the U.S. and Canada.

The MSCI Emerging Markets Index is a float-adjusted market capitalization index that consists of indices in 21 emerging economies.

Bloomberg U.S. Treasury Bond Index includes public obligations of the US Treasury, i.e. US government bonds. Certain Treasury bills are excluded by a maturity constraint. In addition, certain special issues, such as state and local government series bonds (SLGs), as well as U.S. Treasury TIPS, are excluded.

The Bloomberg U.S. Aggregate Bond Index is an index, with income reinvested, generally representative of intermediate-term government bonds, investment grade corporate debt securities and mortgage-backed securities.

The Bloomberg US Corporate High Yield Bond Index measures the USD-denominated, high yield, fixed-rate corporate bond market. Securities are classified as high yield if the middle rating of Moody’s, Fitch and S&P is Ba1/BB+/BB+ or below. Bonds from issuers with an emerging markets country of risk, based on the indices’ EM country definition, are excluded.

The FTSE Nareit All Equity REITs Index is a free-float adjusted, market capitalization-weighted index of U.S. equity REITs. Constituents of the index include all tax-qualified REITs with more than 50 percent of total assets in qualifying real estate assets other than mortgages secured by real property.

The S&P Global Listed Infrastructure index measures the performance of global companies that are engaged in infrastructure and related operations. It provides liquid and tradable exposure to 75 companies from around the world that represent the listed infrastructure universe. To create diversified exposure, the index includes three distinct infrastructure clusters: utilities, transportation and energy.