Quarterly Letter

“The Fed is navigating by the stars under cloudy skies.”

– Jerome Powell, Fed Chairman

Every year the Kansas City Fed invites all Fed Governors and senior personnel to Jackson Hole, Wyoming for an economic confab. The highlight of the meeting is when the Fed Chairman lays out current thoughts about a wide variety of factors impacting Fed policy. This year’s event was particularly closely followed given a variety of conflicting signals regarding the health of the U.S. economy. Then, subsequent to the meeting additional pressures were added with the Israeli-Gaza engagement – the newest entrant in the growing list of global combat zones.

Let’s take a look at a scorecard of some of what we are watching:

Recession:

The U.S. economy is showing surprising strength despite the Fed having raised interest rates a dozen times since March, 2022. Historically, large scale interest rate increases tame inflation by reducing corporate profits, driving unemployment higher and creating at least a few quarters of negative GDP (Gross Domestic Product) growth. That scenario typically creates a recession, and one still might be coming in the first or second quarter of 2024, as recent Fed monetary policy changes will take time to have full impact. So far, however, the economy has proven surprisingly resilient.

Fed Tightening:

The Fed’s interest rate increases seem to be nearing an end, with perhaps a maximum of one or two more quarter point interest rate bumps on the horizon. Whether or not they increase interest rates again, the Fed seems likely to keep the Fed Funds rate higher-for-longer than the consensus expectation.

Inflation:

While not fully tamed, inflation has moderated from nine percent to around three percent. Nonetheless, higher energy costs are the latest inflationary headwind, helping keep inflation elevated.

Corporate Earnings:

Down a bit from last year, but better than expected a year ago. A 2024 earnings recovery is being predicted by many.

U.S. Dollar:

Surprisingly strong, particularly in recent weeks. The dollar’s strength against other major currencies is a challenge for corporations with significant overseas business.

Banking:

After the drama of the Silicon Valley Bank failure in the first quarter, the banking sector seems to have stabilized.

Consumer Spending:

Some cracks are beginning to show; many will need to resume student loan repayments in the fourth quarter and credit card balances are growing while consumer savings are shrinking. Be that as it may, wage increases have been impressive and there are still a lot of jobs available. It is no secret we have a strong stock market bias in managing client portfolios. We have that bias because owning common stocks has always been the simplest, most efficient and least expensive method of building wealth over time. (That is not an opinion, it is an incontrovertible fact. Equities have returned approximately seven percent net of inflation for the past few hundred years and the comparable return for bonds is less than half that.)

This has been true through multiple wars, controversial election cycles and numerous recessions. All that said, the uncertainties of today, for many, seem unique. In truth, it has always been so. No matter the uncertainties, companies in free-market economies quickly adapt and move forward to greater profitability.

Even so, there are reasons to hold bonds in many portfolios. In the current environment the question is how to invest in bonds when short-term fixed-income investments, including money market funds, are paying significantly higher rates than intermediate and longer-term bonds. The dilemma creates what is known as rollover risk. If an investor buys a very short-term bond in order to take advantage of current interest rates, what happens when the investment matures in a year if rates are lower? That is the conundrum, and opinions on how long to extend maturities greatly vary. We favor keeping maturities short, maximizing yield today while providing portfolio flexibility for the future.

There is a great documentary on Amazon Prime about St. Louis native and baseball Hall of Famer, Yogi Berra. Yogi famously said, “If you don’t know where you are going, you will end up someplace else.” Like many of Yogi’s malapropisms, this actually makes some sense. With equities, we are always long-term investors, not speculators – we know where we are going and that we will get there with patience.

We understand that stock prices month-to-month can be unsettling but see nothing in the current situation that would cause us to deviate from our long-term investment strategy of remaining fully invested in stable, profitable, financially sound companies. The skies might be a little cloudy in the short-term, but overall, most economic indicators reflect an encouraging resiliency.

Market Commentary – October 2023

August and September proved to be challenging months for markets, resulting in a down quarter for nearly all investments, as interest rates climbed and seem poised to stay higher-for-longer. Nonetheless, stock markets remain in positive territory and 2023 continues to be a welcome rebound from 2022.

The recovery has navigated a range of challenges including debt-ceiling negotiations, persistent inflation, tightening monetary policy, a resilient labor market, several bank failures, and relatively flat – although better than anticipated – corporate earnings.

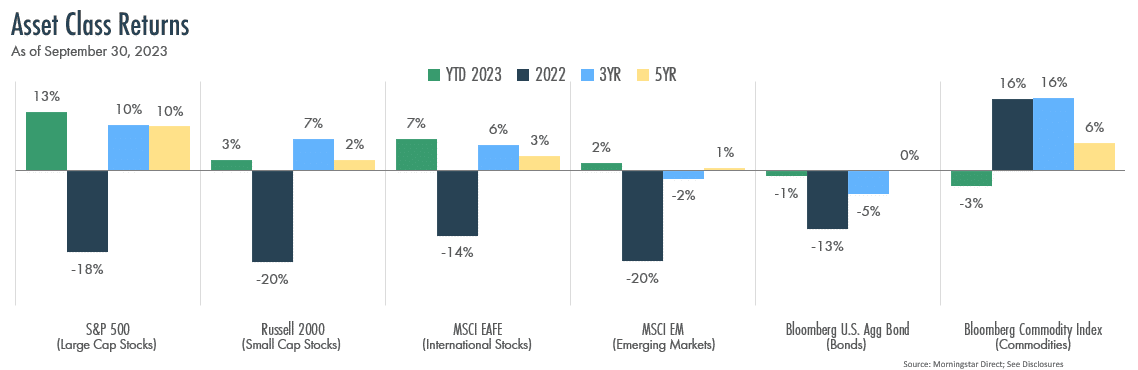

U.S. Large Cap stocks as measured by the S&P 500 Index are up 13% year-to-date, while Small Cap stocks are up just 3%. Top performers remain concentrated, primarily in and around the Technology sector, although many of these stocks fell in the third quarter. Battered in 2022, Growth stocks have rebounded, while Value and dividend-oriented strategies are lagging the broader market. International Developed and Emerging Markets stocks are also lagging, up 7% and 2%, respectively.

The uptick in interest rates has been the primary headwind for the markets. Interest rate concerns were reinforced in the third quarter as the Fed indicated there may be a longer period of restrictive monetary measures than anticipated. Fed officials now suggest that time and patience, rather than additional rate hikes, is essential for bringing inflation back to their 2% target. The Fed remains in the extremely difficult position of trying not to do too much, while not doing too little, to normalize inflation without causing a recession.

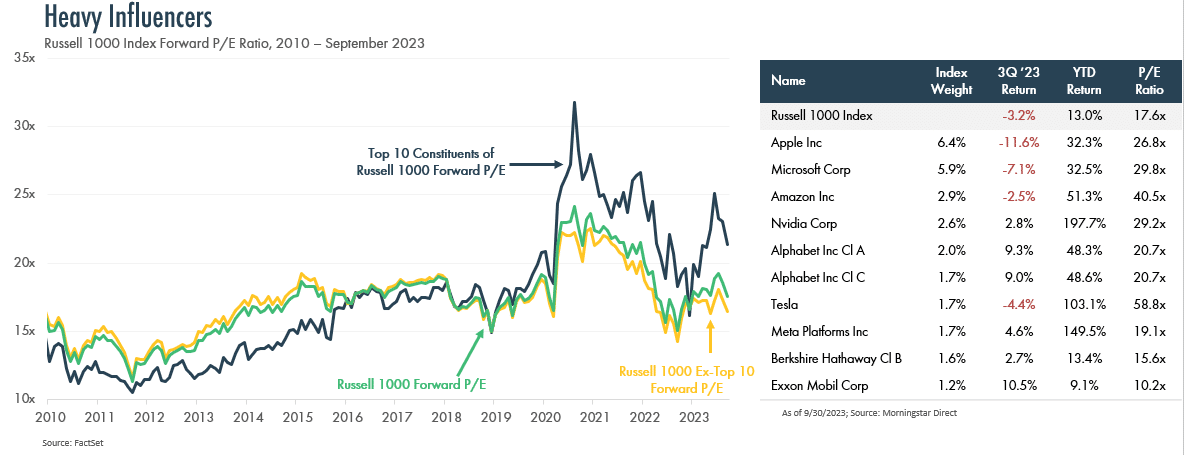

Top Performing Stocks – Opportunity Or Risk?

The largest U.S. stocks by market capitalization had mixed returns in the third quarter after generating sizzling returns in the first half of the year. (See chart above.)

The embrace and buzz around AI (artificial intelligence) has swept across the globe and across the stock market. Even companies whose exposure is, at best, tangential happily trumpet their AI initiatives.

Without the benefit of stock price performance of companies involved with AI, the overall stock market is generally flat for the year.

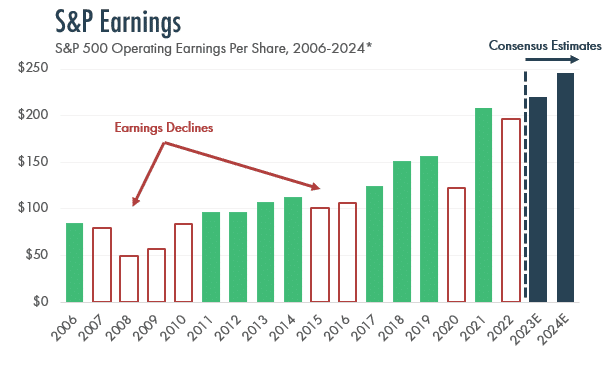

The outlook for S&P 500 earnings (as shown below) remains optimistic as we move into 2024.

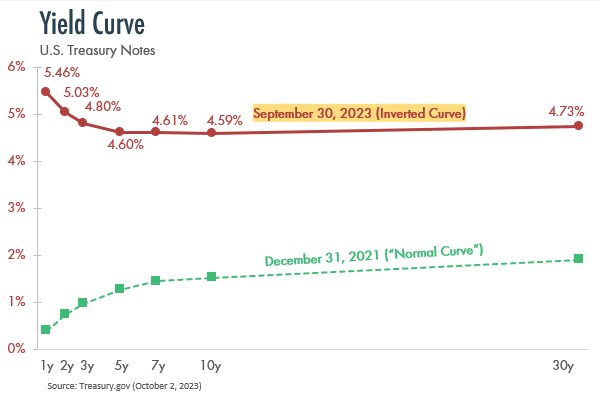

Yield Curve Remains Inverted

For 244 trading days, the longest such streak in history, the indicator known as an inverted yield curve has signaled an economic downturn, with short-term interest rates higher than long-term interest rates. Historically, the inverted yield curve suggests that future economic growth and inflation will slow, resulting in a recession. Thus far, however, the economy has not only avoided a recession, but shows some signs of strength.

The Fed has conveyed its intention to maintain elevated interest rates as long as necessary to steer inflation towards 2.0%. In the third quarter, markets reacted to this “hawkish” stance by pushing Treasury interest rates higher, impacting stock and bond returns adversely. Many now speculate we will see “higher-for-longer” rates which, alongside tighter borrowing standards and elevated oil prices, will likely lead to a phase of weaker economic growth.

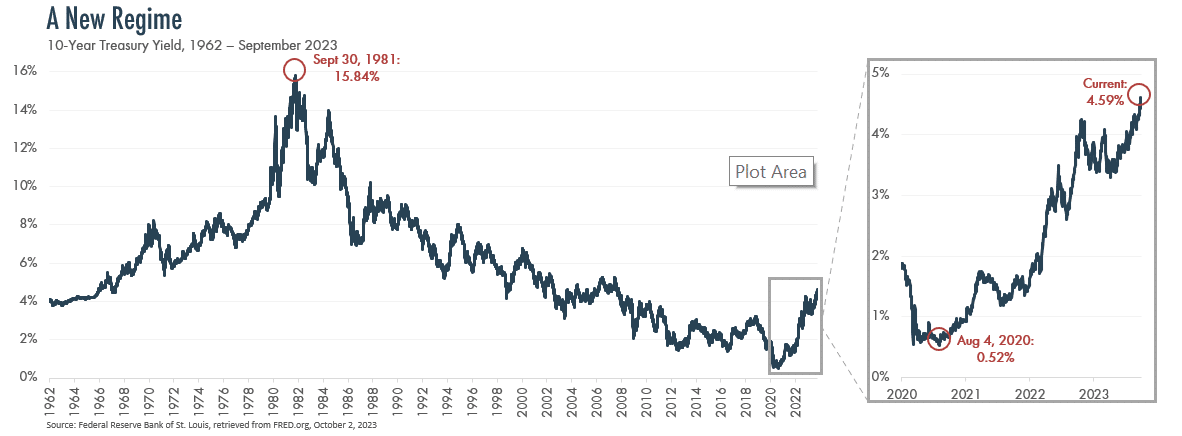

The Burden of Higher Interest Rates

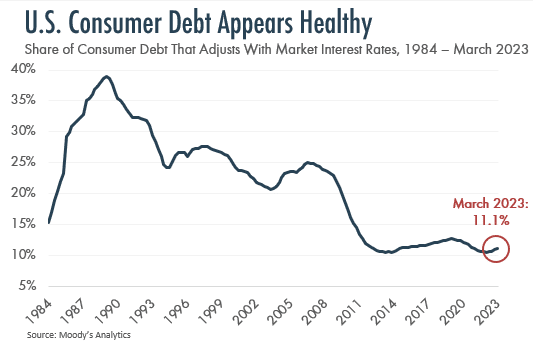

Higher interest rates lead to higher expenses for consumers, reducing purchasing power. Homeowners who secured ultra-low mortgage rates in recent years are understandably reluctant to sell, thereby constraining the number of homes listed and reducing home sales. Surprisingly, however, just 11.1% of consumer debt has a floating rate (largely credit cards) and household debt service payments relative to disposable income remain at healthy levels (as shown at right).

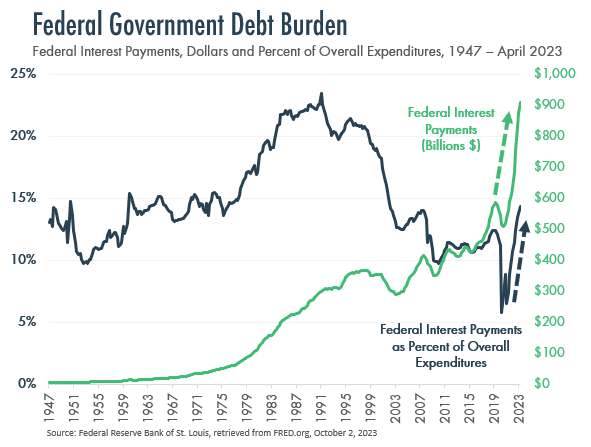

As interest rates climbed, federal government interest payments on the national debt soared past an annualized $900 billion this year, tripling to around 15% of the total budget. With an unbalanced budget since 2001, the government is caught in a cycle of issuing more debt to cover existing debt. As shown below, the blissful few decades of not worrying about government deficits has ended.

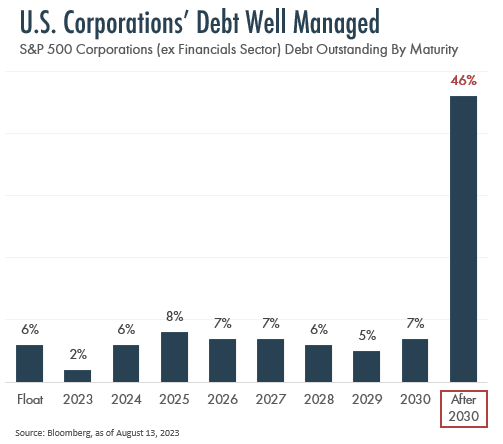

Corporations must prudently manage their debt levels and cash reserves, particularly in a higher interest rate environment. Missteps reduce profit margins and limit spending on innovation and hiring. S&P 500 corporations (excluding Financials) currently must navigate more than $200 billion of debt coming due in each of the next several years. That maturing debt may need to be refinanced at much higher rates. This is termed Rollover Risk. Fortunately, as shown below, 46% of corporate outstanding debt matures after 2030, providing a runway for many to refinance longer-term debt.

Help Wanted

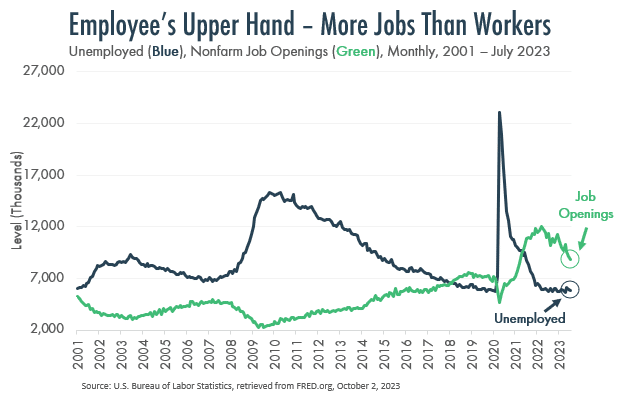

For nearly two years, the U.S. economy has maintained an unemployment rate below 4%. Healthy on the surface, the economy is facing a long-term issue of a shrinking labor force. This is caused by baby boomer retirements, low birthrates, immigration policies and changing worker preferences. Despite softening hiring demand, as shown below, employers still struggle to fill jobs.

The labor force has yet to rebound fully from COVID, with nonfarm payrolls 2 million short of pre-COVID figures. With fewer workers, solutions like immigration, offshoring, and improving workforce productivity (perhaps through technology like Generative AI) are all needed to sustain economic growth.

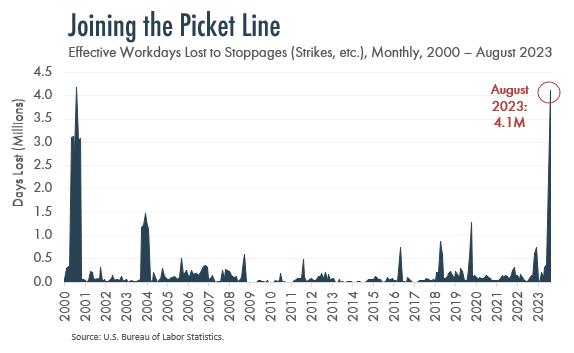

Employees understand the employment imbalance tilts in their favor – the number of workdays lost to stoppages (as shown at the right) has escalated due to a huge uptick in strike activities. In August 2023 alone, over 4.1 million workdays were lost due to work stoppages across the U.S.

Contributors

Important Disclosures and Information

© 2023 The Finerty Team

The S&P 500 Index is a free-float capitalization-weighted index of the prices of approximately 500 large-cap common stocks actively traded in the United States. The Bloomberg US Aggregate Bond Index is a broad base, market capitalization-weighted bond market index representing intermediate term investment grade bonds traded in the United States. The Consumer Price Index (CPI) is a measure of the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services.

Advisory services offered by Moneta Group Investment Advisors, LLC, (“MGIA”) an investment adviser registered with the Securities and Exchange Commission (“SEC”). MGIA is a wholly owned subsidiary of Moneta Group, LLC. Registration as an investment advisor does not imply a certain level of skill or training. The information contained herein is for informational purposes only, is not intended to be comprehensive or exclusive, and is based on materials deemed reliable, but the accuracy of which has not been verified.

Trademarks and copyrights of materials referenced herein are the property of their respective owners. Index returns reflect total return, assuming reinvestment of dividends and interest. The returns do not reflect the effect of taxes and/or fees that an investor would incur. Examples contained herein are for illustrative purposes only based on generic assumptions. Given the dynamic nature of the subject matter and the environment in which this communication was written, the information contained herein is subject to change. This is not an offer to sell or buy securities, nor does it represent any specific recommendation. You should consult with an appropriately credentialed professional before making any financial, investment, tax or legal decision. An index is an unmanaged portfolio of specified securities and does not reflect any initial or ongoing expenses nor can it be invested in directly. Past performance is not indicative of future returns. All investments are subject to a risk of loss. Diversification and strategic asset allocation do not assure profit or protect against loss in declining markets. These materials do not take into consideration your personal circumstances, financial or otherwise.

[/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section]