[button link=”https://monetastl.com/cwcj/cwcj-insider/#signup” type=”big” color=”black”] Sign-up to receive these pieces in your inbox[/button]

Manager of Marketing & Business Intelligence – Megan Merriss

As a marketer by trade, I spend a lot of my day trying to put myself in the minds of my team’s clients. What is most important to them? What do they enjoy doing? What keeps them up at night? I do this in the hopes of creating meaningful content that speaks to them. I do not come from a finance background, except for a few college courses I was required to take to graduate. However, since beginning my journey with CWCJ, I have been fascinated by this business and what financial service means.

CWCJ Insider was born out of the idea that we have vast knowledge and extensive experience on our team that we can share with our clients and beyond. I wanted to create a space to dig deeper into topics those on our team are passionate about or discuss topics less common. (Like our article on QSTs. If you haven’t read this one, it’s an interesting read.)

For series 3 of CWCJ Insider, I wanted to offer a different perspective. An angle of someone on our team that doesn’t directly handle financial activity but is nonetheless fascinated by it all. Especially one lesser talked-about aspect of the financial world that is also shared with marketing. Psychology – let’s discuss the psychology of money!

Navigating Biases: Unlocking the Path to Smarter Investing

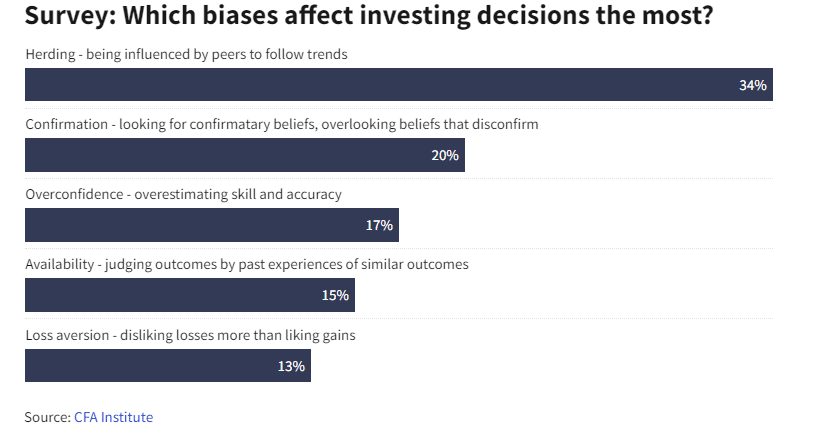

Investing can be a rewarding endeavor, but it is not without challenges. Many of these challenges stem from biases that can cloud judgment and affect decision-making. There are two main types of biases we encounter. Cognitive investing biases and emotional investing biases. Cognitive investing biases stem from established concepts that may be inaccurate, while emotional investing biases arise from personal feelings and experiences. In this article, we will explore some common biases, their impact on investment decisions, and strategies to overcome them.

COGNITIVE INVESTING BIAS EXAMPLES:

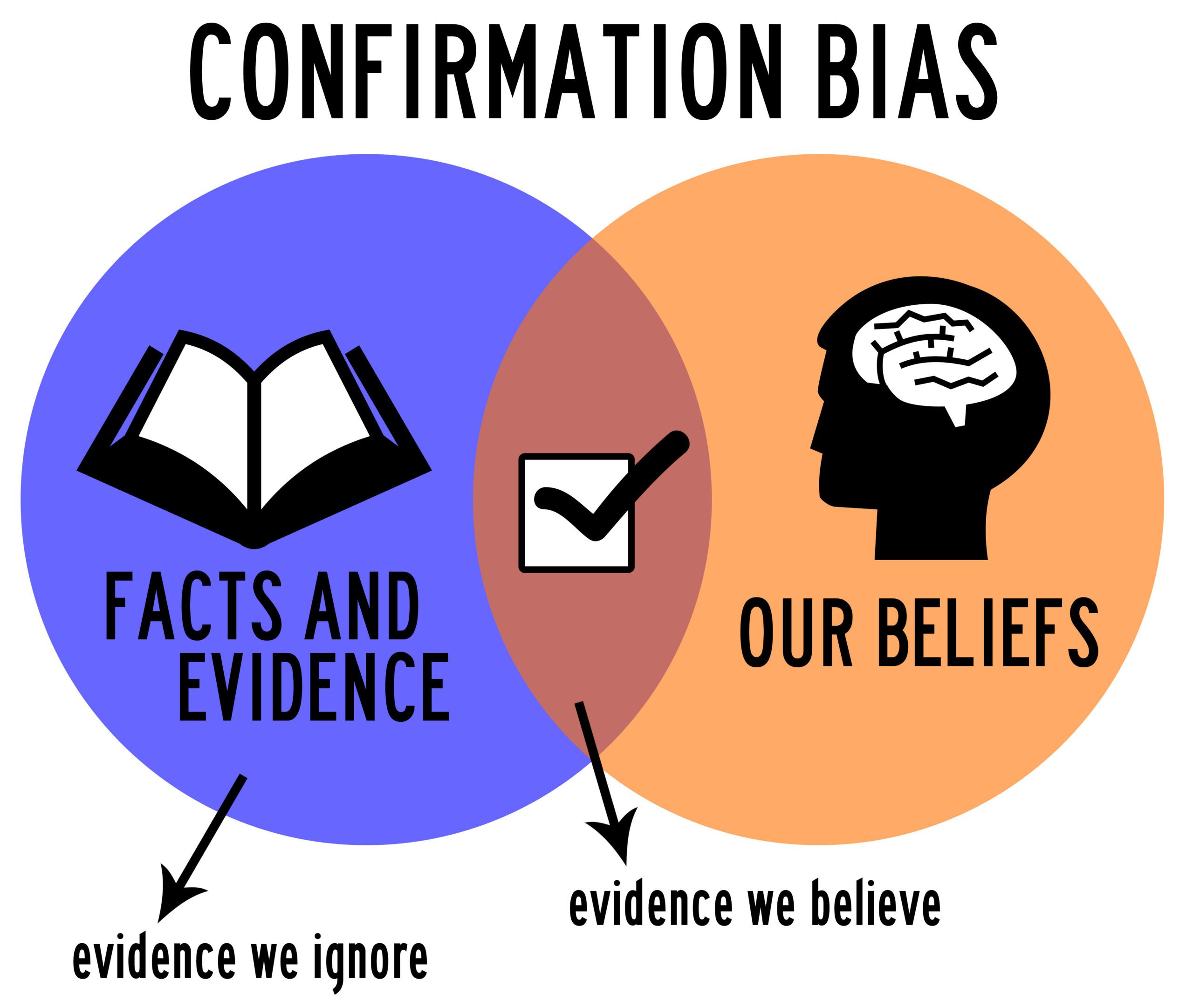

Confirmation bias involves seeking information that aligns with one’s beliefs while disregarding conflicting evidence. We tend to seek out information that we agree with rather than pay attention to information that contradicts our beliefs. It’s important to stay objective when thinking about investments rather than let our subjective thoughts get the best of us.

Herding bias emerges when individuals justify their decisions by observing a widespread adoption of a particular course of action. This tendency can potentially lead to trading assets solely due to their popularity in the market, ultimately contributing to the formation of asset bubbles.

Sunk cost fallacy happens when you continue to invest more money in something because of your previous investments. This bias arises from a natural inclination to avoid losses and seek validation for past decisions, even if those decisions are no longer rational or beneficial.

Sunk cost fallacy happens when you continue to invest more money in something because of your previous investments. This bias arises from a natural inclination to avoid losses and seek validation for past decisions, even if those decisions are no longer rational or beneficial.

Imagine you’ve invested significant time and money into a project that initially seemed promising. As the project progresses, it becomes increasingly evident that its potential for success is dwindling, and the anticipated returns are becoming less likely. Despite this realization, you find yourself hesitant to abandon the project because of the resources you’ve already poured into it. This hesitancy is rooted in the sunk cost fallacy.

Status quo bias leads investors to stick with familiar investments, limiting their profit potential. The allure of the familiar can be remarkably persuasive. However, at Moneta, we have harnessed the collective expertise of an entire investment department to actively unearth novel opportunities. We recognize the significance of diversification, guarding against over-commitment to a single domain. This strategic approach acts as a safeguard, which attempts to shield your portfolio from the tumultuous shifts that characterize volatile market conditions.

EMOTIONAL INVESTING BIAS EXAMPLES:

Risk-averse bias causes investors to give more weight to negative news, potentially overshadowing potential rewards. Recognizing these biases is crucial for making informed investment choices. It’s often easy to become alarmist or worried when it comes to our investments, but that is why we set parameters around investment decisions we make and use data-driven metrics to direct portfolio changes, rather than letting emotional response impact trading.

Loss-aversion bias leads investors to hold onto losing investments, hoping for a turnaround, while overconfidence bias can cause individuals to believe they have superior investment skills. During the COVID-19 pandemic, many investors panicked and sold their stock investments, fearing substantial losses. Unfortunately, those who didn’t reinvest quickly missed out on the historic market rebound that followed. This loss-aversion bias, driven by fear, can prevent investors from capitalizing on potential gains. By understanding this bias, investors can avoid making impulsive decisions, which may improve their overall returns.

Endowment bias, on the other hand, makes investors overly attached to what they already own, even if better opportunities exist. Endowment bias often functions in tandem with other cognitive biases, such as loss aversion and the status quo bias. It can lead investors to miss out on diversification benefits and potentially higher returns as they fixate on safeguarding their existing holdings rather than objectively assessing new opportunities. Recognizing and managing emotional biases is an important step toward making rational investment decisions.

Link to source of image above.

THE ROLE OF A FINANCIAL ADVISOR:

Investing is multifaceted and involves a blend of cognitive and emotional factors. To assist in making wise and informed investment choices, it is crucial for individuals to recognize and address these biases. One effective approach is enlisting a financial advisor who can provide guidance tailored to one’s investment needs. During challenging market conditions, advisors can help investors view such periods as opportunities for growth and adjust their portfolios accordingly.

Financial advisors play a crucial role in helping clients understand their cash flow needs and incorporating them into their investment strategy. A comprehensive plan can help investors not need to sell stocks or assets during market downturns, avoiding potential losses. Developing a long-term financial plan is an effective strategy for mitigating biases. By setting clear goals and creating a customized plan, investors can align their investment decisions with their objectives.

A long-term financial plan is an ongoing process that adapts to changing circumstances. Financial advisors regularly review clients’ portfolios and make necessary adjustments to accommodate their needs. Additionally, tax planning strategies can help lower taxes and maximize investment returns. Investors can navigate difficult and prosperous market conditions by staying committed to the long-term plan and seeking professional advice.

Rough patches in investment portfolios are inevitable, but they also present opportunities for growth. Financial advisors can help investors rebalance their portfolios and implement tax-loss harvesting strategies. These practices ensure that portfolios remain aligned with investment goals.

It is important to recognize that investing is a journey that demands patience, resilience, and a commitment to ongoing learning. By equipping ourselves with knowledge about cognitive and emotional biases and implementing strategies to overcome them, we can enhance our investment decision-making and increase the likelihood of long-term success in the ever-evolving world of investing.

The bottom line is that biases can come from a multitude of sources, including where we grew up, how our parents viewed money and investing, and how we see our peers going about their own investments. Just as I spend my days trying to figure out my client’s mindset a little deeper, learning about yourself more deeply and discovering what biases you may hold can help you make better financial decisions and seek better opportunities.

Learn more about CWCJ here.

SIGN-UP TO RECEIVE THESE EDUCATIONAL PIECES STRAIGHT TO YOUR INBOX HERE.

© 2023 Advisory services offered by Moneta Group Investment Advisors, LLC, (“MGIA”) an investment adviser registered with the Securities and Exchange Commission (“SEC”). MGIA is a wholly owned subsidiary of Moneta Group, LLC. Registration as an investment advisor does not imply a certain level of skill or training. The information contained herein is for informational purposes only, is not intended to be comprehensive or exclusive, and is based on materials deemed reliable, but the accuracy of which has not been verified. Trademarks and copyrights of materials referenced herein are the property of their respective owners. Index returns reflect total return, assuming reinvestment of dividends and interest. The returns do not reflect the effect of taxes and/or fees that an investor would incur. Examples contained herein are for illustrative purposes only based on generic assumptions. Given the dynamic nature of the subject matter and the environment in which this communication was written, the information contained herein is subject to change. This is not an offer to sell or buy securities, nor does it represent any specific recommendation. You should consult with an appropriately credentialed professional before making any financial, investment, tax or legal decision. An index is an unmanaged portfolio of specified securities and does not reflect any initial or ongoing expenses nor can it be invested in directly. Past performance is not indicative of future returns. All investments are subject to a risk of loss. Diversification and strategic asset allocation do not assure profit or protect against loss in declining markets. These materials do not take into consideration your personal circumstances, financial or otherwise.