Andrew Kelsen – Chief Investment Officer

Tim Side, CFA – Investment Strategist

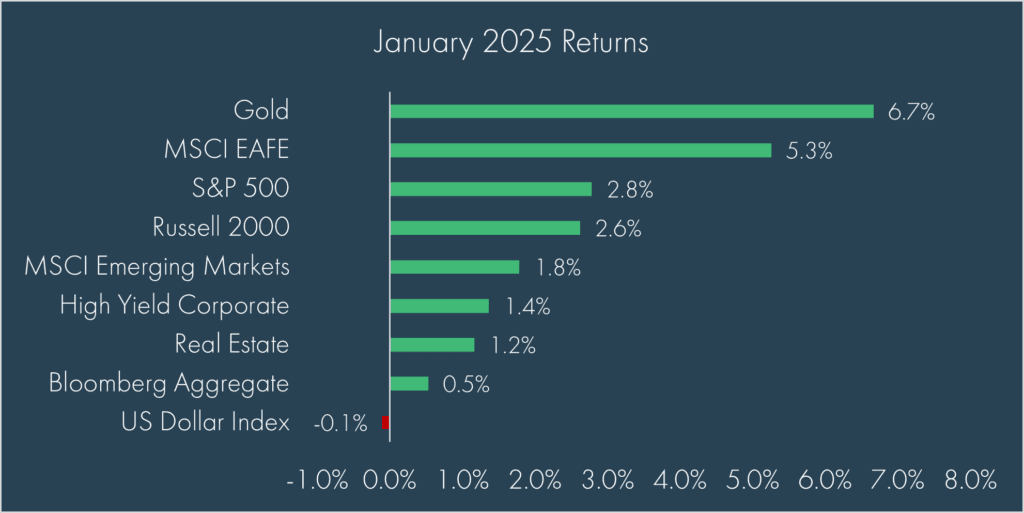

January represented a solid month for public markets in what might be the last stand of the previous global trade system, bouncing back strongly from a tough December. Gains across all areas last month suggest a positive start to the year for markets; the first time in almost three years that everything gained. However, this good news quickly became less important when over the weekend, President Trump announced large tariffs on imports from our three largest trading partners, Canada, Mexico, and China. As we write, both Canada and Mexico have reached an agreement with the US to postpone the threatened 25% tariffs for 30 days, while China responded with minor, retaliatory tariffs and other measures as US tariffs of 10% on all Chinese imports went into effect last night at midnight.

This theme of good news taking a back seat to attention-grabbing headlines (whether it’s another executive order or game-changing AI developments), has defined the last couple of weeks, leaving investors a bit shell-shocked on what to do with the influx of information. In this blog post, we’ll provide some quick thoughts on how to think about this “new normal.”

It’s been two weeks since President Trump was sworn into office, though you wouldn’t know it by the number of executive orders and actions (according to the Federal Register, Trump has already signed 45 executive orders in 2025, compared to 162 from Joe Biden from 2021-2025[1]). The speed and execution (or lack thereof) of these orders reflects two important dynamics of a Trump presidency:

- A self-proclaimed “Tariff Man”, Trump is not afraid to use the United States’ economic importance to the global economy to gain concessions from other countries – he is, after all, the co-author of a book called “The Art of the Deal”. This last weekend illustrated this quite clearly: 25% Tariffs on Mexico and Canada would likely hurt the US consumer (they are our two biggest trading partners), but it would also likely severely damage the Mexican and Canadian economy, who respectively saw 75% and 71% of their exports go to the US last year. This is unlikely to be the last game of “chicken” we see over the next four years.

- To borrow language from the Silicon Valley ethos, Trump is not afraid to “move fast and break things”. Whether through major policy announcements via executive orders, posts on social media, or unleashing the Department of Government Efficiency (DOGE) on various government entities, Trump is not holding back on implementing the policies that he believes he has a mandate to effect.

This brash style of governing and negotiating can be unnerving for markets, which dislike uncertainty, and find it tough to price in what is said versus what will be done. It can also be disruptive for businesses, many of whom are scrambling to assess the flurry of orders and what that means for their respective industries; if importing from Mexico and Canada, do you incorporate a 25% price increase on your consumers or simply wait a couple days to see if the tariffs go away?

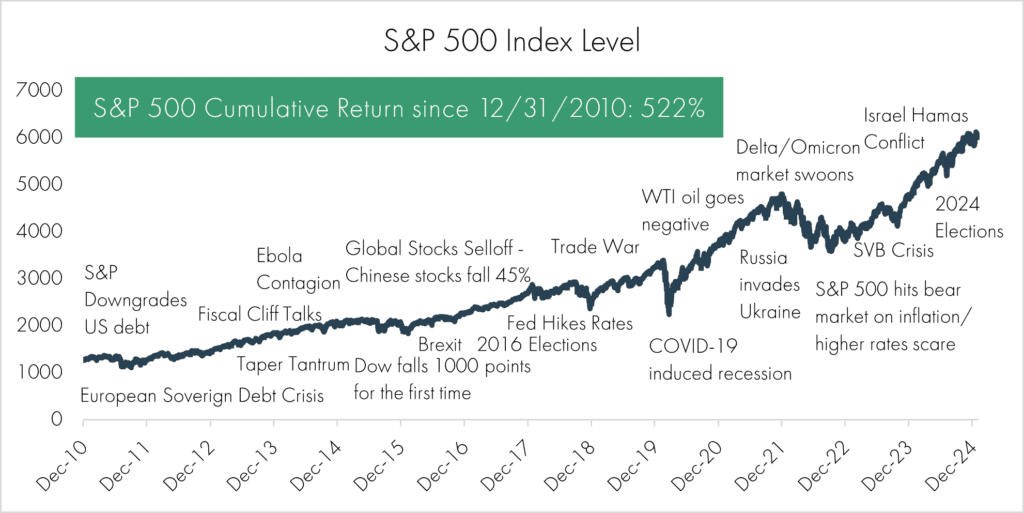

Fortunately, for long-term investors, near-term noise does not hold a candle to the big picture. Despite a never-ending list of concerns, the S&P 500 has climbed a “Wall of Worry” over the last decade (up more than 150% since the last “trade war”):

Additionally, while cracks may be present, the US economy continues its steady march of strong economic growth, as last week’s GDP numbers showed year-over-year quarterly growth of 2.3% with the consumer continuing to hum along. Through Friday, Q4 S&P 500 earnings continue to beat analyst estimates with a blended earnings growth rate of 13.2%.

It’s hard to predict February’s numbers. For now, the beginning of what seems to be a global trade war has increased uncertainty. Given potential for a new global trade system, investors will now need to consider how tariffs will impact the global economy and we will need to watch how these tariffs continue to be used. Trump is a deal guy and a negotiator. Tariffs could just be pieces on a playing board. These four years will be very different from the last. He won’t be running for office again and can do the unpopular things, but markets are resilient, and investment opportunities are present. Stay the course.

[1] https://www.federalregister.gov/presidential-documents/executive-orders

DISCLOSURES

© 2025 Advisory services offered by Moneta Group Investment Advisors, LLC, (“MGIA”) an investment adviser registered with the Securities and Exchange Commission (“SEC”). MGIA is a wholly owned subsidiary of Moneta Group, LLC. Registration as an investment adviser does not imply a certain level of skill or training. The information contained herein is for informational purposes only, is not intended to be comprehensive or exclusive, and is based on materials deemed reliable, but the accuracy of which has not been verified.

Trademarks and copyrights of materials referenced herein are the property of their respective owners. Index returns reflect total return, assuming reinvestment of dividends and interest. The returns do not reflect the effect of taxes and/or fees that an investor would incur. Examples contained herein are for illustrative purposes only based on generic assumptions. Given the dynamic nature of the subject matter and the environment in which this communication was written, the information contained herein is subject to change. This is not an offer to sell or buy securities, nor does it represent any specific recommendation. You should consult with an appropriately credentialed professional before making any financial, investment, tax or legal decision. An index is an unmanaged portfolio of specified securities and does not reflect any initial or ongoing expenses nor can it be invested in directly. Past performance is not indicative of future returns. All investments are subject to a risk of loss. Diversification and strategic asset allocation do not assure profit or protect against loss in declining markets. These materials do not take into consideration your personal circumstances, financial or otherwise.

DEFINITIONS

The S&P 500 Index is a free-float capitalization-weighted index of the prices of approximately 500 large-cap common stocks actively traded in the United States.

The Russell 2000® Index is an index of 2000 issues representative of the U.S. small capitalization securities market.

The MSCI EAFE Index is a free float-adjusted market capitalization index designed to measure the equity market performance of developed markets, excluding the U.S. and Canada.

The MSCI Emerging Markets Index is a float-adjusted market capitalization index that consists of indices in 21 emerging economies.

The Bloomberg U.S. Aggregate Bond Index is an index, with income reinvested, generally representative of intermediate-term government bonds, investment grade corporate debt securities and mortgage-backed securities.

The Bloomberg US Corporate High Yield Bond Index measures the USD-denominated, high yield, fixed-rate corporate bond market. Securities are classified as high yield if the middle rating of Moody’s, Fitch and S&P is Ba1/BB+/BB+ or below. Bonds from issuers with an emerging markets country of risk, based on the indices’ EM country definition, are excluded.

The US Dollar Index measures the US dollar against six global currencies: the euro, Swiss franc, Japanese yen, Canadian dollar, British pound, and Swedish krona.

The FTSE Nareit All Equity REITs Index is a free-float adjusted, market capitalization-weighted index of U.S. equity REITs. Constituents of the index include all tax-qualified REITs with more than 50 percent of total assets in qualifying real estate assets other than mortgages secured by real property.

The Dow Jones Commodity Index Gold is designed to track the gold market through futures contracts.