Tim Side, CFA – Investment Strategist

“THERE ARE DECADES WHERE NOTHING HAPPENS; AND THERE ARE WEEKS WHERE DECADES HAPPEN.”

V.I. Lenin

Executive Summary

- Tariff Announcement: President Trump announced a universal 10% tariff on all US imports and additional tariffs on certain countries, effective April 5th and April 9th, respectively.

- Objectives: The tariffs aim to gain leverage in negotiations, generate revenue to offset tax cuts, and rebalance trade in the US’s favor.

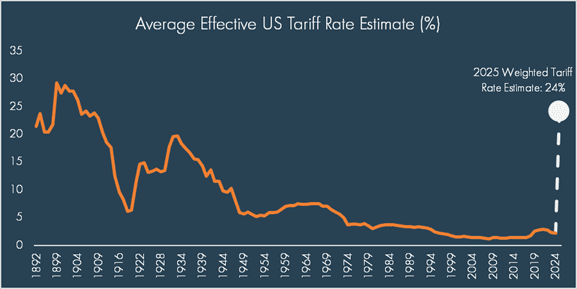

- Economic Impact: With an initial estimated average effective tariff rate just below 25%, markets generally saw the announcement as a worst-case scenario. Broadly speaking, a 25% tariff increase could potentially lead to an $800 billion increase in tariff revenue and a significant drag on GDP.

- Market Reaction: Markets responded poorly, with significant declines in US equities, especially companies with manufacturing bases in China and Vietnam.

- Uncertainty and Strategy: The situation is evolving, and it’s crucial to remain disciplined and avoid panic, as the long-term effects of the tariffs are still uncertain.

“Are you not entertained?”

Love him or hate him, it seems Trump understands theatrics. While Trump was announcing tariffs, a tornado siren went off here in St. Louis – perhaps an ominous sign that seemed fitting given initial market reactions to the news. Nevertheless, what unfolded on Wednesday afternoon in the Rose Garden was nothing short of classic Donald Trump. And whether you think this trade war is the “dumbest in history”[1] or will “drive economic growth for the American people”[2], Liberation Day is behind us, and we can start moving forward with a bit more clarity on what tariffs will look like.

What do we know?

On Wednesday, April 2nd, President Donald Trump announced a universal 10% tariff on all US imports and additional tariffs on certain countries who impose various tariffs and value added taxes (VAT) on US exports. Trump called these “discounted reciprocal tariffs” because the ultimate levy is lower than that charged by foreign countries on US exports. The universal 10% tariff will go into effect on April 5th, while the reciprocal tariffs will go into effect on April 9th. The reciprocal rates are targeted at “worst offenders”, including most of the US’s key trading partners such as China (34% tariff), the European Union (20% tariff), and Vietnam (46% tariff), to name a few. Notably, Canada and Mexico will not be subject to additional tariffs, though they will still be subject to a 25% tariff rate for non-USMCA compliant imports. All told, our rough estimates using 2024 import data points towards an effective tariff rate (the weighted average rate) around 24% – just shy of the 25% that many had considered a worst-case scenario.

Of course, we are in the very early days of these announcements with many details and deals to be worked out. The situation is evolving and while we have done our best to ensure up-to-date numbers at the time of publishing, this blog post should not be seen as the most up-to-date source of information. For that, we’d recommend the Wall Street Journal’s Tariff Tracker or Trade War Timeline (a subscription may be required). Instead, we aim to achieve five objectives: (1) Provide perspective on what the Trump administration is trying to accomplish, (2) provide comments on the potential impacts to the economy, (3) provide insights on what segments might be most at risk, (4) review how the market is initially responding, and (5) provide some considerations on how to respond.

What is the Trump Administration trying to accomplish?

According to Bloomberg[3], “Treasury Secretary Scott Bessent has described Trump’s use of tariffs as falling into three buckets – a tool to gain leverage in negotiations, a revenue-generating measure to offset the cost of extending the 2017 tax cuts, and as a way to rebalance trade in the US’s favor.”

Of those three noted objectives, one carries massively different implications than the other.

The first, “A tool to gain leverage in negotiations”, is mostly what markets anticipated for Trump 2.0 coming into the year. That said, investors were caught off-guard when Trump came out forcefully in early February taking shots at two of our biggest trading partners, Canada and Mexico, forcing a reset in expectations for how far Trump would be willing to go in the negotiations.

The second, “A revenue-generating measure to offset the cost of extending the 2017 tax cuts”, has been largely overlooked, following the logic that meaningfully generating tariff revenue would require a level of tariffs (and therefore economic pain) beyond what a businessman like Trump would be willing to stomach. We noted in a past blog post that tariff revenue peaked in 2022 at $100 billion; with a federal deficit of $1.8 trillion in 2024, tariff revenue seemed almost inconsequential. We’ll examine the numbers in greater detail, but even just a universal tariff of 10% alone might make this goal more realistic, though it ignores the political and economic consequences of an effective tax increase.

The third, “A way to rebalance trade in the US’s favor”, is where things get uncomfortable. Last year, we put out a 3-part series on geopolitics and noted the shift towards deglobalization. Well, Trump and his administration are putting this shift into hyperdrive, calling out “unfair” trade practices by our trading partners (“friend and foes”) and attacking the US’s $900 billion trade deficit head-on with the stated goal of bringing manufacturing (jobs) back to the US and helping the working class. With the S&P 500 up more than 3,000% (10.4% annualized) since 1989, on the back of cheap labor, higher margins, and better earnings, US stocks have clearly been a beneficiary of globalization. In that context, the idea that our system needs fixing can seem baffling to investors, yet it’s important to remember that Trump’s core voting base saw him as a “change candidate”[4]. Despite the S&P 500’s 66% (13.6% annualized) return over Joe Biden’s presidency, voters chose the change candidate, giving Trump both the electoral and popular vote – in other words, Trump and his voter base might not really care about the stock market (at least for now) as he executes his “mandate”.

Using one tool to fulfill three different goals can create confusion for investors on how to interpret the deluge of tariff announcements. When Trump announces a 25% tariff on automotives, is he negotiating on immigration policy, trying to raise some revenue, or trying to bring auto manufacturing back to the US? In some cases, it might be all three! This could be a reason why Trump seems to love tariffs, but ultimately, there are no easy answers. US government deficit spending at $1.8 trillion, especially with higher rates, is unsustainable, but if there was a painless solution, it certainly would have been taken by now. For better or worse, a majority of Americans voted for Trump to change the country; and it is hard to argue that change is not occurring.

How does this impact the economy?

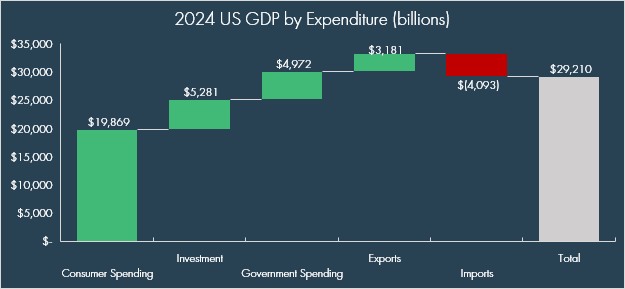

In 2024, the US’s total Gross Domestic Product (GDP) was $29.2 trillion. The chart below illustrates the various components of this calculation, which as a quick refresher, follows the formula:

GDP = Consumer Spending + Investment + Government Spending + (Exports – Imports)

“All else equal”, with an estimated $3.3 trillion in imported goods in 2024, a 25% tariff increase (a “worst case”) across the board would result in an $800 billion increase to imports; a potentially significant drag on GDP (imports have an inverse impact on GDP). This is a very conservative estimate; final numbers are likely to be lower given the case-by-case approach to each country. Additionally, accounting for a multitude of factors such as currency movements, substitution effects, reciprocal tariffs, government spending impacts, changes in investments, and consumer behavior, to name a few, makes any true estimate of the impact of tariffs a bit of a fool’s errand. But, following Trump’s stated goal of bringing manufacturing back to the US, the most likely outcome means, absent significant technology gains, higher prices as US workers cost more to employ. To what extent remains to be seen.

So, who’s at risk?

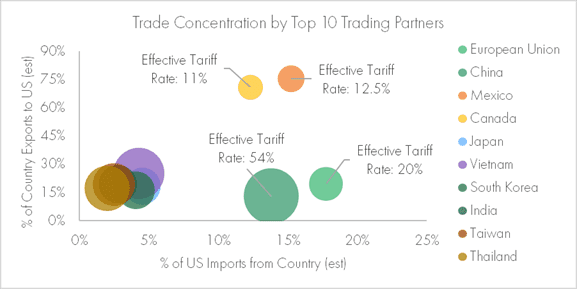

With a 10% universal tariff rate and higher reciprocal tariff rates, there are really no safe places to hide. Canada and Mexico appear to have gotten off “easy”, as their 25% tariff rate does not apply to imports that are compliant with USMCA (about 38% of Canadian imports and 50% of Mexican imports are USMCA compliant according to White House estimates). But otherwise, most countries and imports are at risk; the following chart illustrates the trade exposure for our top 10 trading partners with bubble size indicating a rough estimate of an average effective tariff rate:

These 10 trading partners represented nearly 80% of US imports in 2024, with the four trading partners on the right side of the chart (Canada, China, European Union, and Mexico) representing nearly 60% of US imports. The varying sizes of the bubbles (representing the estimated effective tariff rate) indicate the nuanced approach to each situation. Additionally, as the y-axis illustrates, each country will be forced to consider how they want to respond – only 14% of China’s exports are to the US compared to Mexico’s 75%; China might be more incentivized to play hardball while Mexico might be more incentivized to acquiesce.

What sectors are most exposed?

We examined these top 10 partners to see which sectors might be most exposed. Within this group of countries, there are varying degrees of sector “exposure”. For example, the US imported $32 billion of toys and sports equipment from China in 2024, representing 74% of all toys and sports equipment imported. For that sector, there is a massive exposure to Chinese tariffs (54% as we write), but relative to overall US imports ($3.3 trillion), toys and sports equipment make up a small segment. To assess the biggest exposures, we grouped the top 5 product types that the US imports from these countries, and totaled the dollar amount of imports and the overall percentage of product imports from this group of countries:

| Top Five US Imports from European Union, China, Mexico, Canada, Japan, Vietnam, South Korea, India, Taiwan*, and Thailand in 2024 | ||

| Product | $ of Imports (billions) | % of US Product Import |

| Industrial machinery and appliances | $ 462 | 87% |

| Electrical equipment and parts | $ 410 | 84% |

| Cars, trucks, cycles and parts | $ 373 | 95% |

| Coal, oil and gas | $ 170 | 68% |

| Pharmaceuticals | $ 166 | 78% |

Source: Bloomberg, UN Comtrade as of 3/26/2025; trade data for the calendar year 2024; *Taiwan data for the calendar year 2023.

What does this mean for markets?

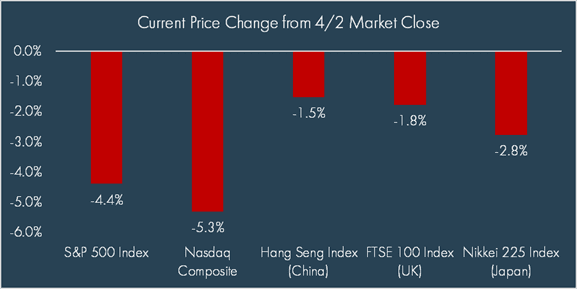

Markets have responded poorly:

Notably, there is divergence between US equities and non-US equities, with non-US equities aided by a decline in the US dollar, which as we write, is down more than 2% relative to a basket of currencies. Within US equities, notable losers include companies with significant manufacturing bases in areas such as China and Vietnam, such as Apple (-9%), Nike (-13%), and Lululemon (-13%). US Small Cap Stocks, as measured by the Russell 2000 Index, have declined more than 6% as we write, given a reduced ability for price negotiations and greater exposure to recession concerns.

To be sure, we are seeing diversification benefits playing out in real time, as Treasury yields have fallen (the 10-year yield is down about 10 basis points) while defensive asset classes such as infrastructure are actually up about half a percent. Interestingly, gold is down more than half a percent – perhaps a sign that more pain was priced in relative to equities?

All told, markets are signaling expectations for some combination of supply chain disruptions, higher input costs, and a potential slowdown in consumer demand.

How should we respond?

The pain is real, and uncertainty abounds. As Trump spoke, we saw literal storm clouds in the sky and numbers turning red all across the screen. To some, Liberation Day may be the best thing that has happened in their lifetime as well-paying jobs come back to the US on the back of investment into the US industrial base. To others, it could be the end of their business that simply cannot withstand the shock of higher input prices and supply chain chaos. To all, it could mean real pain from a recession, something that aside from the 2–3-month COVID-19 shock, we haven’t experienced since the Global Financial Crisis.

However, it is times like these when it is most critical to take a step back, maybe take a breath, and trust the process. There are so many unknowns right now, and based on initial comments from Treasury Secretary Scott Bessent, there are many things that Trump’s own administration doesn’t even know. As they “pull all the trade levers” at once, it will be hard enough to pinpoint the effects of each action 12 months from now, much less in real time. Long-term growth of wealth is made from a disciplined process. Permanent impairment of capital can occur when we panic, and make sub-optimal decisions based on fear.

Today is the noise and theatre. Days like this are for the fast money. That is not us. This could be the final purge in the recent selloff. We will hit a “seller exhaustion” moment soon. 6-12 months from now we will know if these tariffs were a bold stroke of genius or a really bad idea. Consider muting CNBC and Fast Money. Watch this play out and think about rebalancing.

[1] https://www.wsj.com/opinion/donald-trump-tariffs-25-percent-mexico-canada-trade-economy-84476fb2

[2] https://www.whitehouse.gov/fact-sheets/2025/04/fact-sheet-president-donald-j-trump-declares-national-emergency-to-increase-our-competitive-edge-protect-our-sovereignty-and-strengthen-our-national-and-economic-security/

[3] https://www.bloomberg.com/news/articles/2025-03-25/trump-s-threat-of-secondary-tariffs-invents-new-trade-weapon?embedded-checkout=true

[4] https://www.pewresearch.org/short-reads/2024/11/13/what-trump-supporters-believe-and-expect/

DISCLOSURES

© 2025 Advisory services offered by Moneta Group Investment Advisors, LLC, (“MGIA”) an investment adviser registered with the Securities and Exchange Commission (“SEC”). MGIA is a wholly owned subsidiary of Moneta Group, LLC. Registration as an investment adviser does not imply a certain level of skill or training. The information contained herein is for informational purposes only, is not intended to be comprehensive or exclusive, and is based on materials deemed reliable, but the accuracy of which has not been verified.

Trademarks and copyrights of materials referenced herein are the property of their respective owners. Index returns reflect total return, assuming reinvestment of dividends and interest. The returns do not reflect the effect of taxes and/or fees that an investor would incur. Examples contained herein are for illustrative purposes only based on generic assumptions. Given the dynamic nature of the subject matter and the environment in which this communication was written, the information contained herein is subject to change. This is not an offer to sell or buy securities, nor does it represent any specific recommendation. You should consult with an appropriately credentialed professional before making any financial, investment, tax or legal decision. An index is an unmanaged portfolio of specified securities and does not reflect any initial or ongoing expenses nor can it be invested in directly. Past performance is not indicative of future returns. All investments are subject to a risk of loss. Diversification and strategic asset allocation do not assure profit or protect against loss in declining markets. These materials do not take into consideration your personal circumstances, financial or otherwise.

DEFINITIONS

The S&P 500 Index is a free-float capitalization-weighted index of the prices of approximately 500 large-cap common stocks actively traded in the United States.

The NASDAQ Composite Index is a broad-based capitalization-weighted index of stocks in all three NASDAQ tiers: Global Select, Global Market, and Capital Market.

The Hang Seng Index is a free-float capitalization weighted index of a selection of companies from the Stock Exchange of Hong Kong.

The Nikkei-225 Stock Average is a price-weighted average of 225 top-rated Japanese companies listed in the First Section of the Tokyo stock Exchange.

The FTSE 100 Index is a capitalization-weighted index of the 100 most highly capitalized companies on the London Stock Exchange.