Quarterly Letter

“Anyone who lives within their means suffers from a lack of imagination.”

– Oscar Wilde

As we prepare this investment update, Congress is putting the finishing touches on the Big, Beautiful Bill. While we applaud some aspects of it, and fret over others, clearly Oscar Wilde would cheer. Congress has certainly not lost its imagination!

The passage of the new Bill seems apropos, coming just days after the close of one of the wildest first halves for the stock market in memory. What a turbulent ride, with the April Tariff Tantrum knocking many stocks down by 30 percent or more. With approaching headlines such as, “Iranian Nuclear Sites Bombed by U.S.”, who would have predicted a stock market recovery in May and June? Much more relaxing for those with a Rip Van Winkle temperament, as one napping through the first half would have guessed little had changed.

Perhaps with more trade policy clarity and with certainty around tax policy for the next few years, coming months will be less exhausting. If so, returns for the balance of the year could be surprising. Inflation is falling and should further benefit from pending trade deals which lower the overall effective tariff rate. A low bar has been set for corporate earnings expectations, possibly setting the stage for positive surprises. In addition, the dollar is down 10 percent or more against most major currencies, which for multi-national firms can be a positive, turning foreign profits into higher earnings when converted back to dollar denomination.

Needless to say, there are obstacles on the path to better news. Trade wars could easily re-escalate. Inflation could also prove stubborn, particularly if reasonable trade deals fail to materialize. That could prevent the Fed from lowering interest rates. While we try to be generally optimistic, it is a fact that stronger than expected earnings are hardly a given. Housing, for one, has shown weakness in recent months. Finally, while recent jobs reports from the Labor Department are still satisfactory, momentum is weakening. The Labor Force Participation Rate has dipped, and when fewer people are contributing to the workforce, it has negative implications. Fair warning: this is something that is likely to be a growing concern in an Artificial Intelligence (AI) driven future.

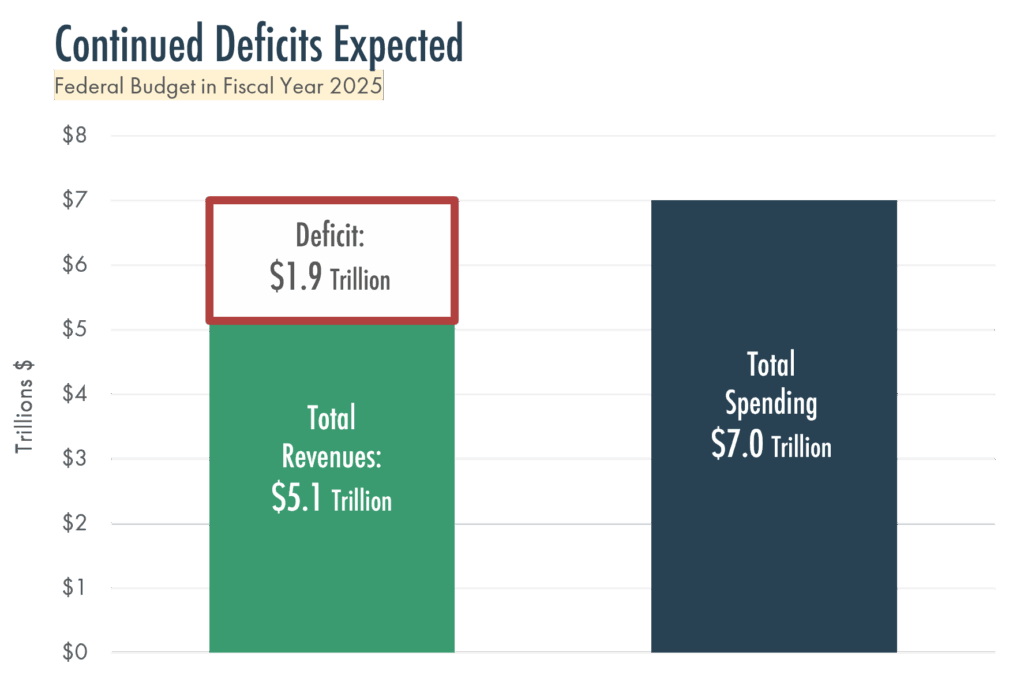

Regarding the U.S. federal deficit, we are pleased that deficit dialogue was heated in June as negotiations of the budget ensued. The national debt is undeniably on an unsustainable path, but leaders of both political parties show little interest in addressing it. The truth is that the deficit will not be a problem until it is, and by waiting until that it is moment – whether in 10, 20 or 30 years – the challenge to rectify it gets harder by the day. As put so well by Ronald Reagan, “Government is like a baby; an alimentary canal with a big appetite at one end and no sense of responsibility at the other.”

The bottom line is that in a world where our politicians seem to be auditioning for a TV reality show – except no one would believe it – we think a grind higher for stocks, and modest decline in interest rates, seems a likely outcome over the balance of the year. Charlie Munger put it best: “The first law of compounding is to never interrupt it unnecessarily. The best time to buy the great companies in America is when you have the money. The best time to sell them is when you need the money. Everything else is the madness of market timing.”

“Government is like a baby; an alimentary canal with a big appetite at one end and no sense of responsibility at the other.”

– Ronald Reagan

Market Commentary

– Randall Stauder, CFA – Portfolio Strategist

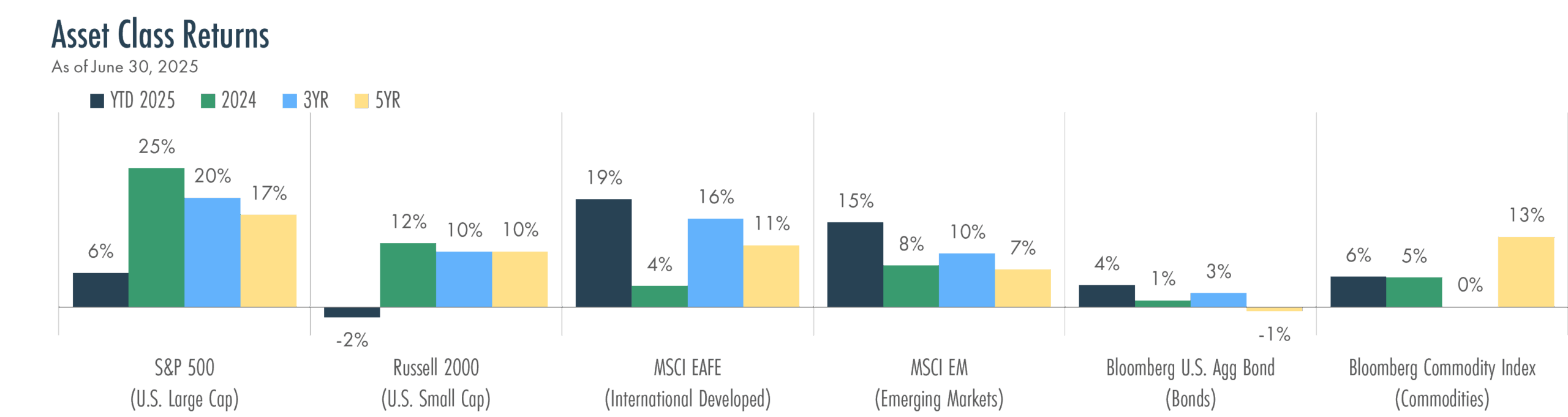

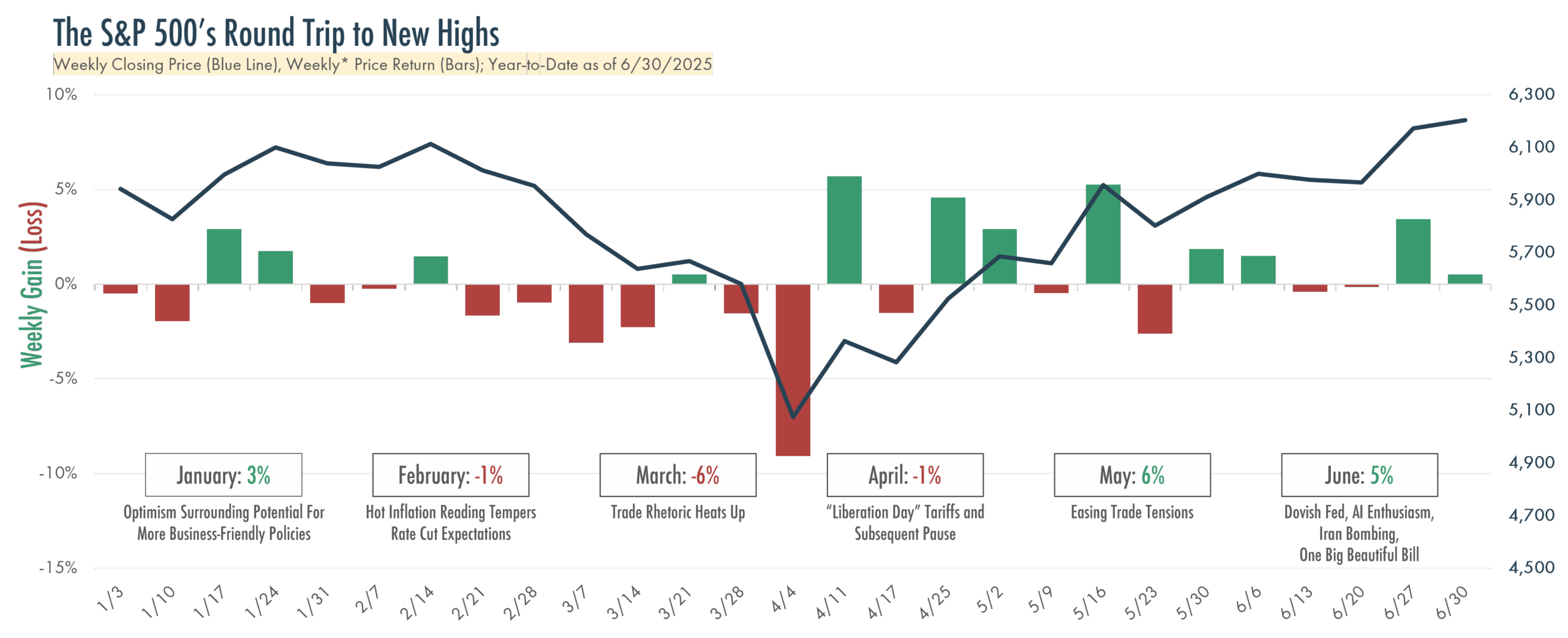

- Markets ended the first half of 2025 on a high note, with the S&P 500 Index setting a fresh all-time high, up 6% year-to-date. After a brief, but sharp, pullback in April driven by tariff fears, the S&P 500 staged a remarkable recovery – the fastest in history starting from a decline of 15% or more.

- International stocks have led all major asset classes in 2025. Developed Markets are up 19% year-to-date, while Emerging Markets are up 15%. Both benefitted from compelling valuations, a weakening U.S. dollar and accommodative central bank policy abroad.

- Bond markets have shown some signs of life this year, posting a 4% gain year-to-date, as measured by the Bloomberg U.S. Aggregate Bond Index. Momentum in bond pricing, however, has been constrained by upward pressure on longer-term yields. While the front-end of the yield curve remains anchored by Fed policy, longer-term rates have stayed elevated given market anxiety surrounding tariff and inflation uncertainty and questions about U.S. creditworthiness.

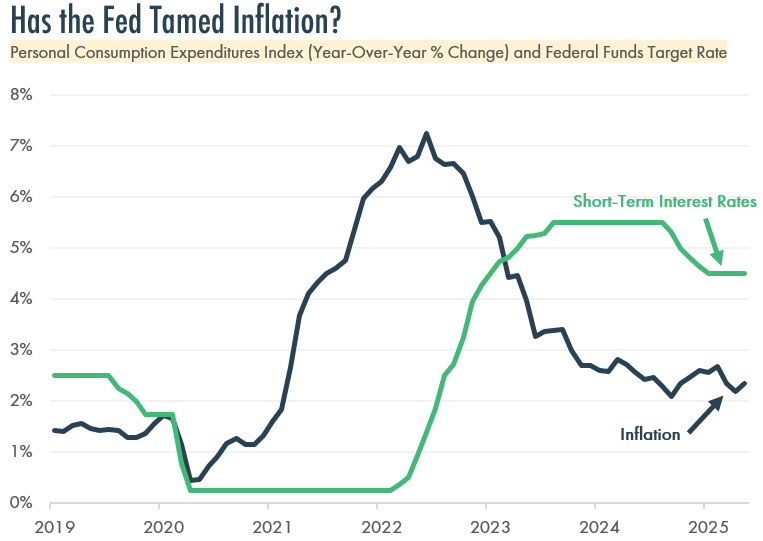

- The Federal Reserve has left interest rates unchanged thus far in 2025, citing caution around the potential inflationary effects of new tariffs. While two rate cuts are priced into markets for the second half of this year, the Fed appears reluctant to move prematurely.

First Half Turbulence

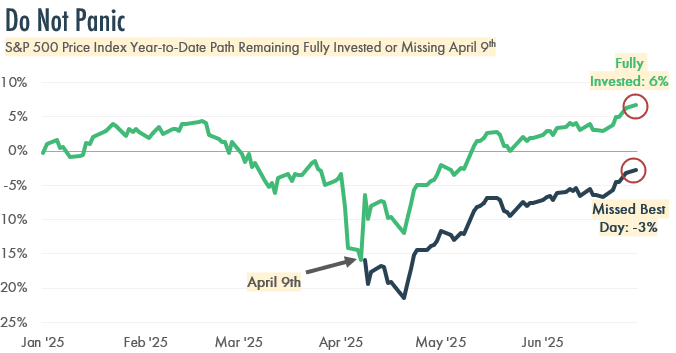

- 2025’s first half was defined by volatility. The S&P 500 approached bear market territory (down 20%) in April before surging nearly 25% by the end of June. Market sentiment shifted week-to-week driven by a barrage of headlines, from tariffs to corporate earnings to the bombing of Iran.

- Timing the market is difficult and costly. Investors who missed just one day of the first half of 2025 – April 9th – have underperformed the index by about 9%. The best days often cluster around the worst, making “sitting it out” a dangerous game.

Debt Dilemma

- As shown in the lower right, the U.S. federal deficit continues to swell, with borrowing required for over 25% of government spending. Major budget categories such as Defense, Social Security, and Medicare now account for half of federal spending. This leaves little room to address the problem without major policy changes.

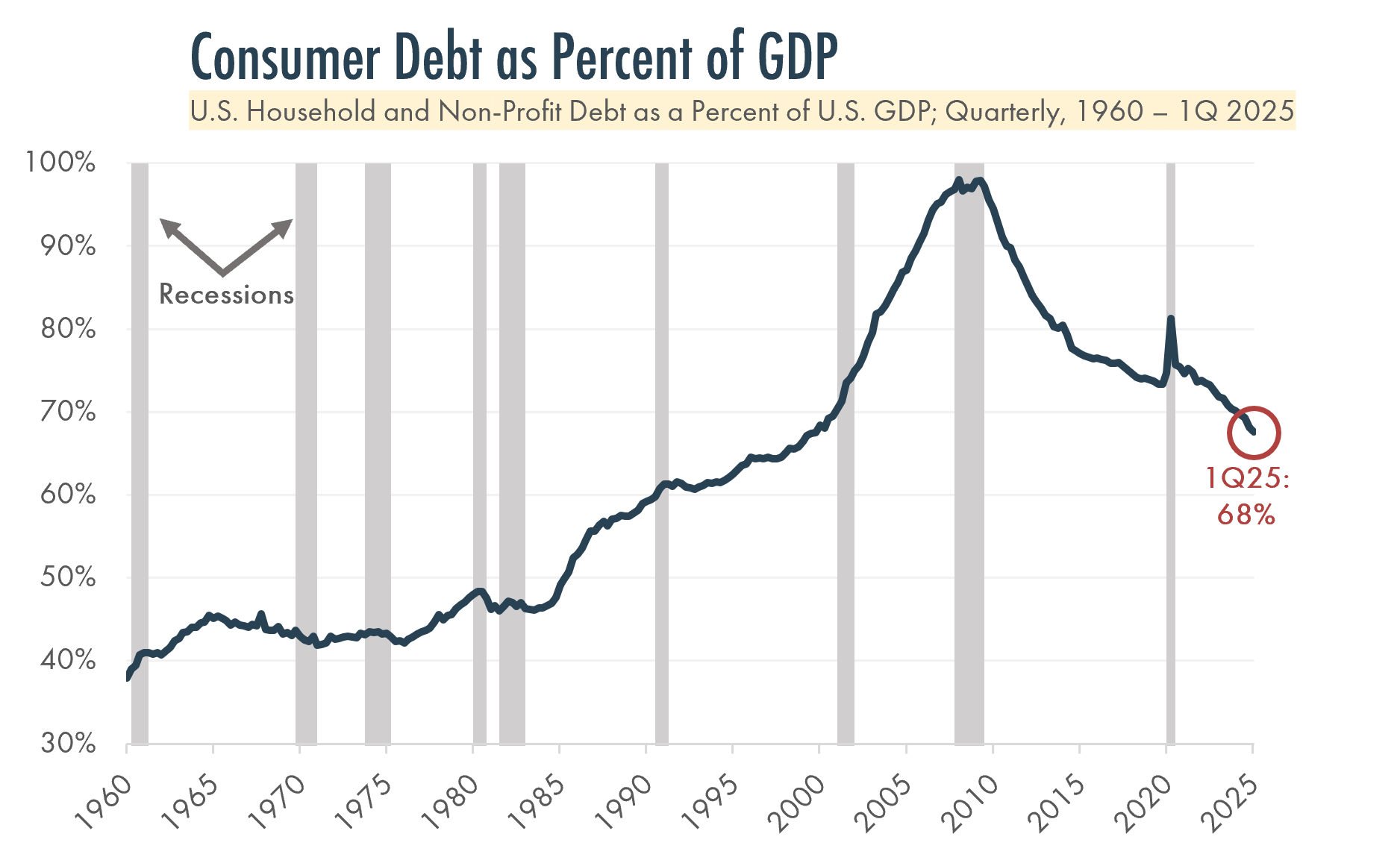

- On a positive note, U.S. households and corporations have deleveraged considerably since the Great Financial Crisis, as shown to the right. Household debt as a percent of Gross Domestic Product (GDP) has fallen back to early-2000s levels.

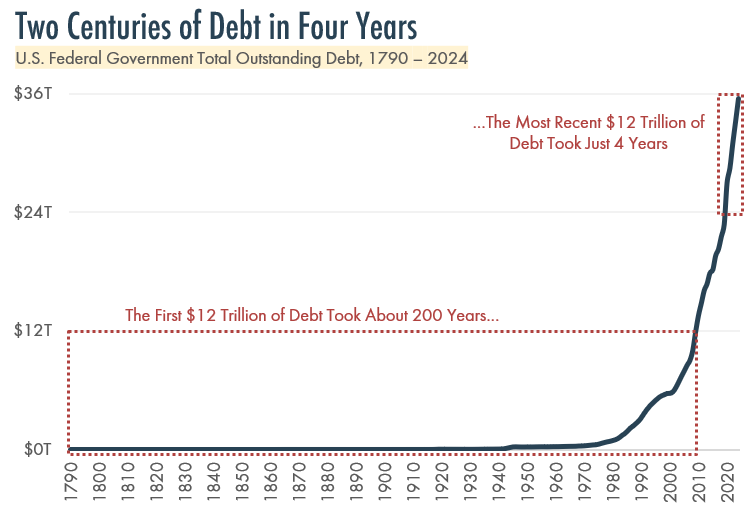

- It took nearly 200 years – from George Washington to Barack Obama – for the U.S. government to rack up its first $12 trillion in debt. As shown below, it took ten years for the next $12 trillion and just four years to add the latest $12 trillion. Without meaningful reform to rein in persistent deficits, it is likely a long-term recipe for higher inflation and a slower growth economy.

The Waiting Game for the Fed

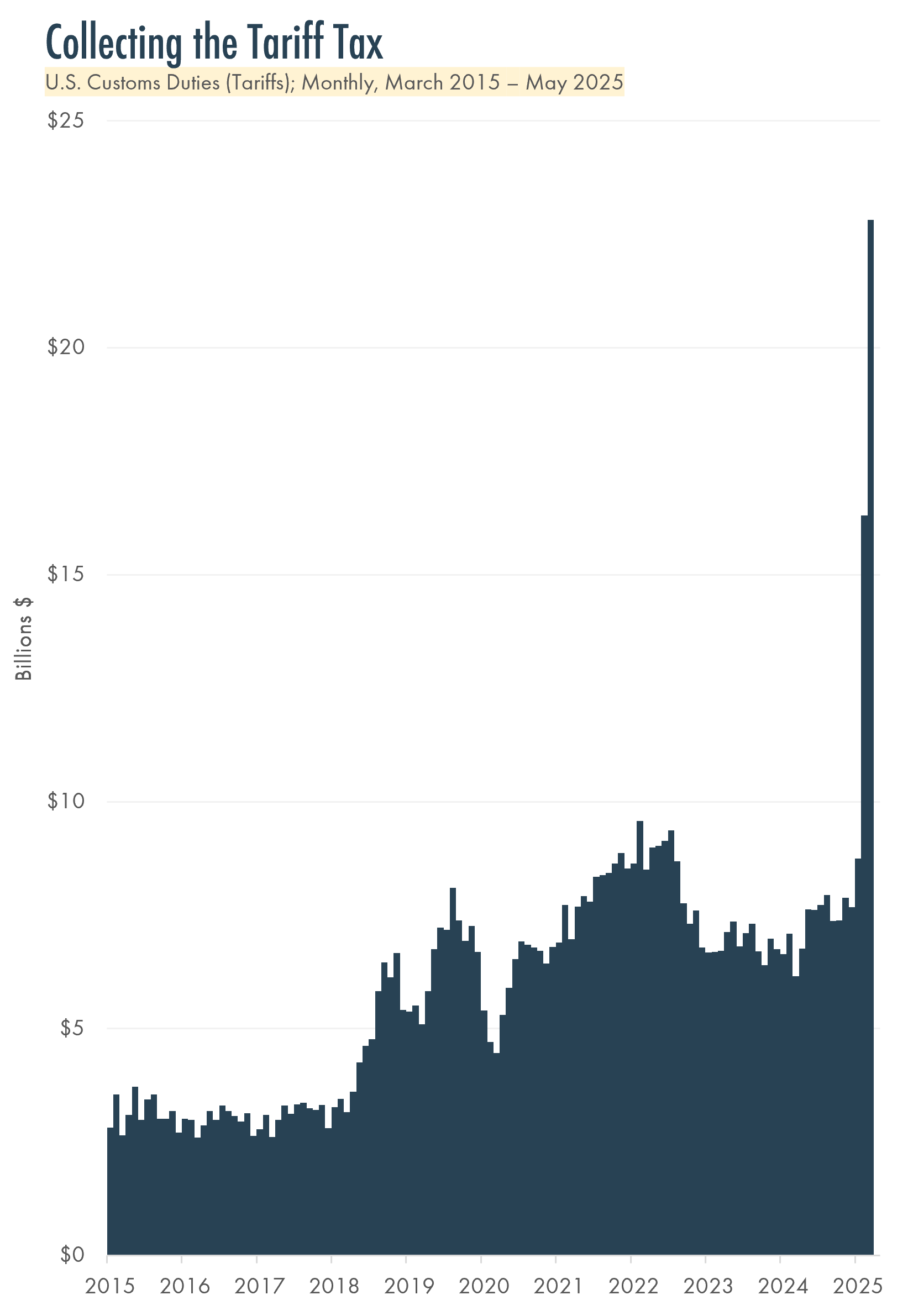

- Tariffs dominate headlines. New and proposed tariffs since April have pushed average U.S. tariff rates to levels not seen since pre-WWII.

- The revenue impact of tariffs are real ($22.8 billion in May alone), but that is a rounding error against a nearly $2 trillion deficit. Tariffs may be more about negotiation and leverage than about balancing the budget.

- Although tariffs have not meaningfully impacted inflation data, the Fed is on high alert. Jerome Powell has emphasized Fed analysts are closely watching potential tariffs’ effects on inflation.

- Powell’s cautious stance reflects a hard-learned lesson from 2020 to 2022, when the Fed kept interest rates near zero even as inflation accelerated. That delay contributed to the inflation surge which peaked in 2022, and ultimately forced the Fed into a sharp tightening cycle.

Contributors

© 2025 The Finerty Team

The S&P 500 Index is a free-float capitalization-weighted index of the prices of approximately 500 large-cap common stocks actively traded in the United States. The Bloomberg US Aggregate Bond Index is a broad base, market capitalization-weighted bond market index representing intermediate term investment grade bonds traded in the United States. The Consumer Price Index (CPI) is a measure of the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services.

Advisory services offered by Moneta Group Investment Advisors, LLC, (“MGIA”) an investment adviser registered with the Securities and Exchange Commission (“SEC”). MGIA is a wholly owned subsidiary of Moneta Group, LLC. Registration as an investment advisor does not imply a certain level of skill or training. The information contained herein is for informational purposes only, is not intended to be comprehensive or exclusive, and is based on materials deemed reliable, but the accuracy of which has not been verified.

Trademarks and copyrights of materials referenced herein are the property of their respective owners. Index returns reflect total return, assuming reinvestment of dividends and interest. The returns do not reflect the effect of taxes and/or fees that an investor would incur. Examples contained herein are for illustrative purposes only based on generic assumptions. Given the dynamic nature of the subject matter and the environment in which this communication was written, the information contained herein is subject to change. This is not an offer to sell or buy securities, nor does it represent any specific recommendation. You should consult with an appropriately credentialed professional before making any financial, investment, tax or legal decision. An index is an unmanaged portfolio of specified securities and does not reflect any initial or ongoing expenses nor can it be invested in directly. Past performance is not indicative of future returns. All investments are subject to a risk of loss. Diversification and strategic asset allocation do not assure profit or protect against loss in declining markets. These materials do not take into consideration your personal circumstances, financial or otherwise.