Quarterly Letter

“The key to making money in stocks is not to get scared out of them.”

-Peter Lynch

Investors are justified in feeling a little pain given that they have just experienced the worst first half for global stock markets since the 1970’s, with the average U.S. stock down 20 percent or more. Even more sobering, this particular correction has coincided with rising interest rates and the worst bond market since the late 1970’s.

The severity of the stock market weakness greatly accelerated in the second quarter, with readings of 8 percent inflation, sky-high oil and gas prices and the Ukrainian War settling into a heavyweight slugfest. In addition, surging mortgage rates are sure to slow the robust housing market, and the Fed is clearly positioning itself for several more interest rate increases. This concurrence of negative news suggests to many that economic readings due out in late July will show that the U.S. economy is already in a recession. They might be right.

A recession is defined as two consecutive quarters of negative gross domestic product (GDP) growth. Regardless of whether or not we are officially in a recession, a slow-down has clearly occurred. Unfortunately, this is the medicine we probably need as continued inflation is highly destructive. The Fed seems committed to tolerating lower economic growth for some time in order to put out the fire.

The concern, of course, is that the Fed, embarrassed that they initially coined it “transitory” inflation, will over-react and raise interest rates too fast and too high. Indeed, the mere expectation of the Fed’s new monetary restraint (with higher interest rates and shrinking balance sheet) already seems to be working. Oil prices in recent weeks have softened on the possibility of reduced demand, lumber prices have plummeted on the expectation of a housing slowdown, and some businesses are scaling back hiring given evidence of more cautious consumer spending. In addition, copper prices have declined, indicating businesses see a downturn coming – copper is a critical industrial metal used in everything from electric vehicles to household appliances.

As we are often reminded, stock markets move based on the outlook for business and economic conditions in the future. It seems reasonable, therefore, that stock market declines in recent months have been foretelling the softening conditions we will see in the balance of this year, and potentially into next. Thus, the new narrative is that the next shoe to drop will be widespread reductions in future corporate earnings estimates. Indeed, we fully expect that to begin happening in coming weeks – not drastic cuts to forecasts, but measured reductions reflecting current challenges.

The year-over-year change in fixed-income markets with higher interest rates is also quite a story. Two-year Treasury notes were paying 0.25 percent one year ago. They paid 2.84 percent at the end of June. The result has been the first big decline in bond prices in forty years. In the U.S., the Fed has indicated it will continue to raise interest rates and reduce its balance sheet (by declining to purchase bonds in the open market), which should push interest rates up even more. Short-term interest rates, in particular, seem destined to be higher. However, whether intermediate and longer-term rates follow suit is anyone’s guess. We are agnostic and see validity to arguments both ways – those for higher longer-term rates and for those who state there will not be a significant change for some time. As a result, we continue to keep bond maturities relatively short, feeling there is little downside to maintaining a cautious approach.

One of the world’s great investors, Fayez Sarofim, died several weeks ago. Among his many comments was,

“Nervous energy is a great destroyer of wealth. The temptation to sell has cost investors more money than they would have made by doing nothing.”

We concur, as any student of investing knows that large stock market gains often occur when least expected.

Surprisingly, when one looks to the S&P 500 Index returns over the past 100 years, there are six occurrences similar to the first half we just experienced. In every case returns in the second half of the year were positive, usually significantly so. Candidly, it does not seem obvious to us that such a result will happen this time, but great companies adapt quickly to a changing economic environment. Eventually, renewed profit growth ensues. While it may take a quarter or two more of unpleasant volatility to see this happen, we know the patient long-term investor will be rewarded, just as they have been in the past.

Market Commentary

- Markets grappled with heightened volatility in the first half due to rising inflation, higher interest rates, signs of a slowing economy, and geopolitical issues. Major stock indices had a very rough quarter, finishing in bear market territory – defined as a drawdown of 20%. U.S. Large Cap stocks were down 20% and Small Caps dropped 23%. International Developed Markets were also down 20%, while Emerging Market equities fared only slightly better, off 18% year-to-date.

- It was the worst first half for bonds in over 40 years, with most bond market indices declining by high single-digits. Two-year Treasuries, which yielded 0.25% one year ago, jumped to 2.84%, close to the10-year Treasury note rate of 2.88%.

- The Fed is strongly committed to cooling inflation, which remains above 8%, and is willing to tolerate lower economic growth to do so. Historically, the Fed has never been able to tame elevated inflation without causing a recession. Recessions have occurred without inflation, but not the other way around.

- Among the few asset classes in positive territory, Commodities were up 18% in the first half, driven by supply shortages which boosted oil, gas, and grain prices.

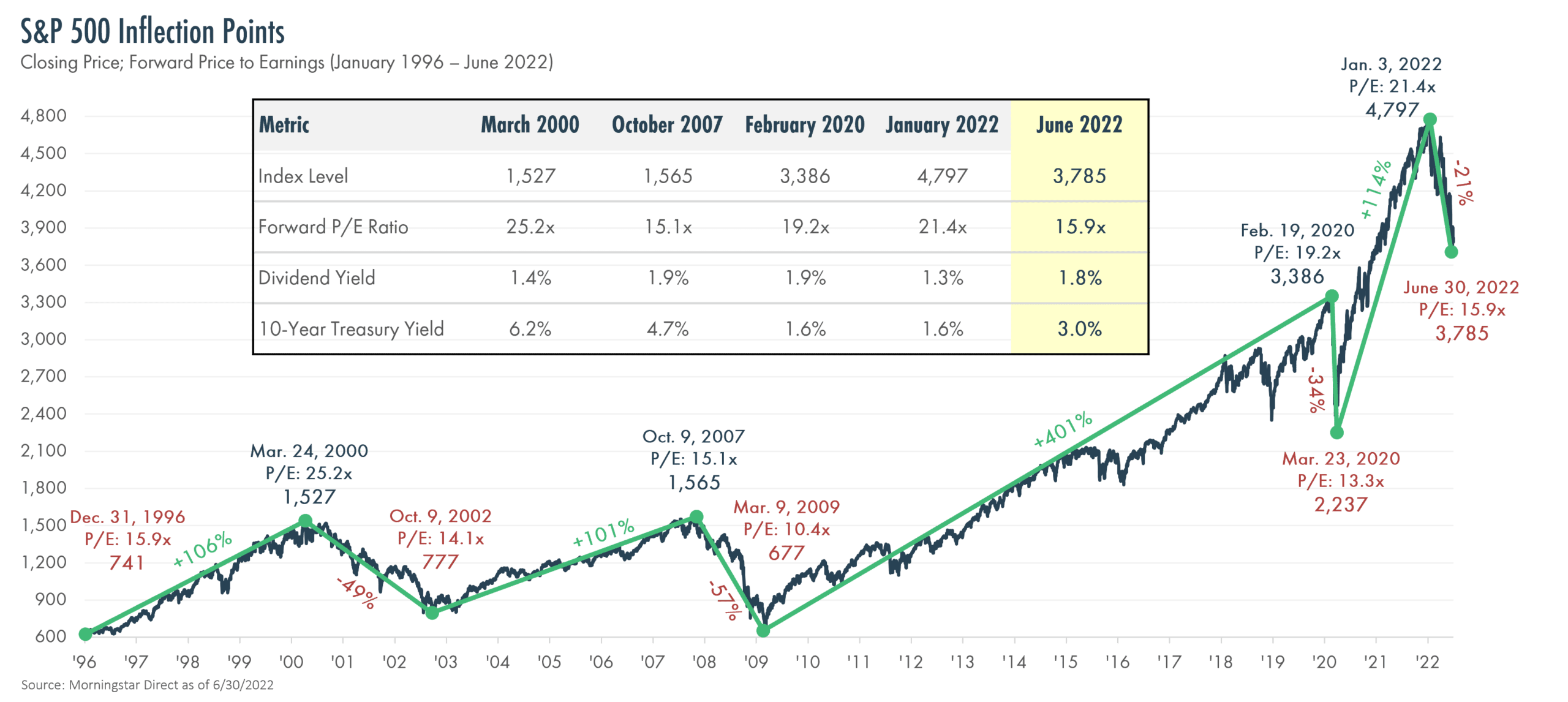

Inflection Points

- The first half of 2022 experienced increased volatility as markets contended with inflation and rising interest rates among other issues. The S&P 500 Index entered bear market territory for the first time since 2020 and just the fourth time since 1990. While significant declines of this nature are challenging for investors, the S&P 500 had more than doubled in value from the depths of COVID-19 through January and has gained nearly 600% since 2009.

- With economic momentum stalling, valuations of stock markets worldwide have gotten much more attractive. The average Price-to-Earnings (P/E) Ratio is down to 15.9 times forward earnings. Excluding the 10 largest companies, the average P/E drops to below 14 times.

- Elevated inflation paired with a healthy consumer and a tight labor market make this bear market unique. Early in the year, many businesses were indicating a surprising ability to raise prices. Today, pricing power seems to be decreasing, putting future profit margins in question.

Recession on the Horizon?

- Since World War II, the U.S. economy has endured 12 recessions, each featuring two key factors: declining GDP and rising unemployment. If we are on the precipice of a recession, this one will be unique – GDP did contract slightly in the first quarter, but unemployment remains near 50-year lows and there are currently 1.9 job openings for each unemployed worker.

- Inflation remains a serious challenge today, exacerbated by a tight labor market and rising wages. In addition, as consumers get out and spend again, consumer savings rates have slowed, as shown below, and returned to historical averages.

- Given media coverage, this may be the most highly anticipated recession in history. Importantly for investors, stocks historically have mostly corrected ahead of recessions, with the market bottoming, on average, 116 days before GDP bottoms and recovering an average of 19% in that window (as shown at the right).

- Mortgage rates have surged and will unquestionably have a negative impact on the housing market in coming quarters. As shown in the lower right, the 30-year mortgage rate jumped from 3.20% in January to 5.84% by the end of June.

Fed Determined to Tighten

- The Federal Reserve began hiking interest rates in the first half and plans to continue with more restrictive monetary policy to fight inflation. While the hope is for a “soft landing,” the Fed has never successfully tamed inflation without inducing a recession, which may ultimately be the only anecdote to bring inflation down to acceptable levels.

- Every tightening cycle since 1974 has resulted in the Fed raising short-term interest rates above CPI inflation, which could be a sign of what is to come. Short-term interest rates have gone from virtually zero to over 2% in the past 12 months. Inflation currently exceeds 8% but seems destined to fall somewhat in the coming months.

- Higher short-term interest rates mean higher lending rates for businesses and consumers. In turn, higher financing costs cause businesses and households to reduce spending, which should decrease demand.

Contributors

The S&P 500 Index is a free-float capitalization-weighted index of the prices of 500 large-cap common stocks actively traded in the United States. The Bloomberg US Aggregate Bond Index is a broad base, market capitalization-weighted bond market index representing intermediate term investment grade bonds traded in the United States. The Consumer Price Index (CPI) is a measure of the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services.

Performance returns cited represent past performance, which is not indicative of future returns. Index and/or Style returns reflect total return, assuming reinvestment of dividends and interest. The returns do not reflect the effect of taxes and/or fees that an investor would incur. Investors cannot invest directly in an index. Opinions expressed herein are solely those of the Finerty Team as of the date of this commentary and subject to change without notice. These materials were prepared for informational purposes only based on materials deemed reliable, but the accuracy of which has not been verified. Trademarks and copyrights of materials referenced herein are the property of their respective owners. This is not an offer to sell or buy securities, nor does it represent any specific recommendation. You should consult with an appropriately credentialed professional before making any financial, investment, tax or legal decision. All investments are subject to a risk of loss. Diversification and strategic asset allocation do not assure profit or protect against loss in declining markets. These materials do not take into consideration your personal circumstances, financial or otherwise.

© 2022 Moneta Group Investment Advisors, LLC. All rights reserved. These materials were prepared for informational purposes only based on materials deemed reliable, but the accuracy of which has not been verified. This is not an offer to sell or buy securities, nor does it represent any specific recommendation. You cannot invest directly in an index. You should consult with an appropriately credentialed professional before making any financial, investment, tax or legal decision. Past performance is not indicative of future returns. These materials do not take into consideration your personal circumstances, financial or otherwise.