Quarterly Letter

The year 2024 had something for everyone – a beautiful Paris Olympics, Taylor Swift-mania, an unprecedented U.S. Presidential election, and, most importantly to our clients, strong stock market returns. The S&P 500 Index wrapped up its second year in a row with over a twenty percent return, led again by technology-oriented businesses, particularly those investing in artificial intelligence (A.I.).

Does a three-peat for investment returns seem possible? One never knows, but stock market investors are well-advised to curb short-term enthusiasm. There is a lot trending right, but valuations are on the high-end and at some point, markets will need a breather to allow time for earnings growth to catch up.

How to best bring the investment landscape into better focus? Perhaps Benjamin Franklin can be of help. Franklin is credited with the invention of bifocals to fix both near- and far-sightedness. With our bifocals, when we peer through our long-term lens we continue to see a lot of good news. Consumer spending remains strong, labor market conditions are easing, short-term interest rates seem likely to decline, and corporate earnings are projected to be strong and relatively evenly spread among different sectors of the U.S. economy. In addition, a Trump administration is widely expected to be more pro-business – less regulation and lower taxes.

All that said, shifting our gaze to our shorter-term lens, there are potential stumbling blocks in the path. What will Trump really do, and what will simply serve as rhetoric for negotiation tactics? In addition, while Trump does have a pro-market bias, he was elected, in part, on populist themes, particularly those of higher tariffs and immigration control. Both are issues which could impact inflation, and consumers could pay more for items they purchase as new government policies are implemented.

Finally, there are budgetary issues and the soaring U.S. Federal deficit. In consideration of this, Elon Musk and Vivek Ramaswamy are leading a new Department of Government Efficiency (DOGE), with a stated goal of reducing Federal spending by $500 billion. The big cuts, however, that would make a true difference are with entitlements, such as Social Security and Medicare, and entitlements are currently the political third rail, too controversial for most politicians of either party to even discuss. Thus, while we admire the lofty goal, we will take a “Show Me” attitude until proven otherwise on this long-standing problem. As students of history know, arguments regarding the national debt and deficits have occurred ever since Alexander Hamilton, Thomas Jefferson and James Madison compromised in 1790 to allow the Treasury to assume state debts in exchange for the national capital to move to what is now Washington D.C. At that time, the debt was estimated to be $77 million. Oh, for the good ‘ole days!

We cannot close without also commenting on A.I. and how it continues to super-charge the stock market. Its impact can hardly be overstated. The Magnificent Seven – Apple, Microsoft, Meta, Alphabet, Tesla, NVIDIA and Amazon – represent, in aggregate, only 1.4 percent of the companies included in the S&P 500 Index. However, those seven companies represent fourteen percent of all S&P 500 companies’ sales, thirty-one percent of all S&P companies’ sales growth, and thirty-three percent of all S&P 500 companies’ total dollar earnings. In addition, collectively they are spending hundreds of billions of dollars annually on Research and Development, more annual spending than the entire market capitalization of most other S&P giants such as Coca Cola, Home Depot and Exxon.

Bottom line, we remain positive on the stock market, but more cautious in the short-term than we have been the past few years. While the economy and corporate earnings should do well in 2025, we expect bumps along the way. As mentioned at the opening, it is normal to experience a cooling off period after two exceptional years, and to recognize that while there is reason for optimism in 2025, we need to appreciate that returns with stocks are always uneven.

Nonetheless, we will stay on the same path, and keep our bifocals trained at a distance where it is easier to have confidence in outcomes. All great investors agree that the secret to success in stocks is not letting short-term uncertainty scare you out of them.

Market Commentary

– Randal Stauder, CFA – Portfolio Strategist

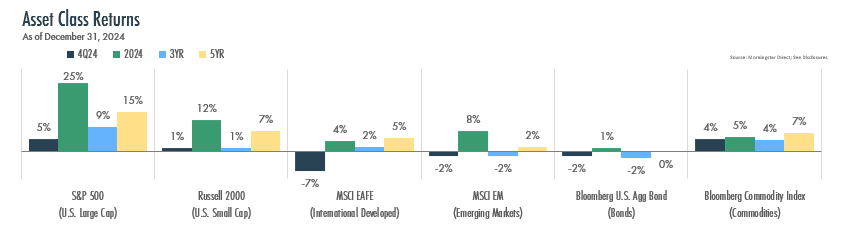

§2024 marked the second consecutive year of impressive stock market strength, despite an unprecedented presidential election, economic uncertainty, and stubbornly high interest rates.

- U.S. Large Cap stocks, as measured by the S&P 500 Index, were up 25% in 2024. Although “lagging”, U.S. Small Cap stocks staged an impressive rally in the second half of 2024 to finish the year up 12%.

- International Developed and Emerging Markets stocks were up 4% and 8%, respectively. Easing inflation and stabilizing economic conditions across major regions resulted in gains despite geopolitical challenges.

- Fixed-income markets were generally up in 2024, with low single digit returns. While short-term interest rates declined, longer-term interest rates stayed stubbornly high.

The U.S. economy has demonstrated remarkable resilience, with GDP expanding at an annualized rate of 2.7% in the third quarter, even as some signs of labor market softening emerge. Strong consumer spending and a tight labor market continue to underpin economic strength, though potential government policy shifts loom in 2025.

The Fed reduced short-term interest rates three times for an aggregate total of 1.0% in 2024. With the U.S. economy seemingly in good shape and inflation still hovering above the Fed’s long-term 2% target, Fed Chairman Jerome Powell expressed uncertainty about the timing of future rate cuts as officials continue to judge the path of the economy and inflation.

Quarter Century Observations

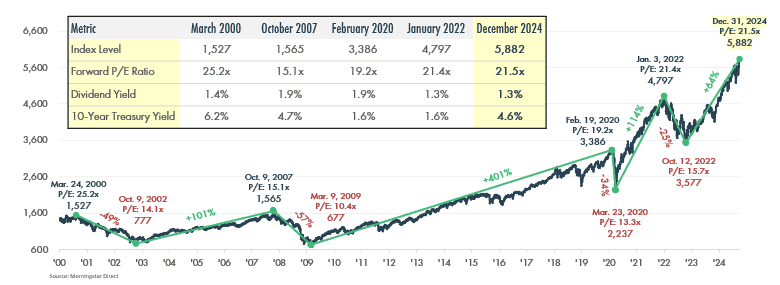

Over the past 25 years, the S&P 500 has grown from 1,469 at the end of 1999 to nearly 6,000 at the close of 2024. Despite four large bear markets, long-term investors saw $1,000,000 invested in 1999 (at a market peak no less) grow to more than $6,000,000 today. As shown below, it is not a smooth path, but stock markets consistently take two steps forward for every one step back, rewarding disciplined investors and demonstrating the power of compounding even amid market volatility.

Since 1999, S&P 500 cash dividends have grown more than 4.5 times, far outpacing inflation, which has only doubled over the same period. This dividend growth reflects the strength of corporate earnings and highlights the role of reinvested income in driving long-term returns.

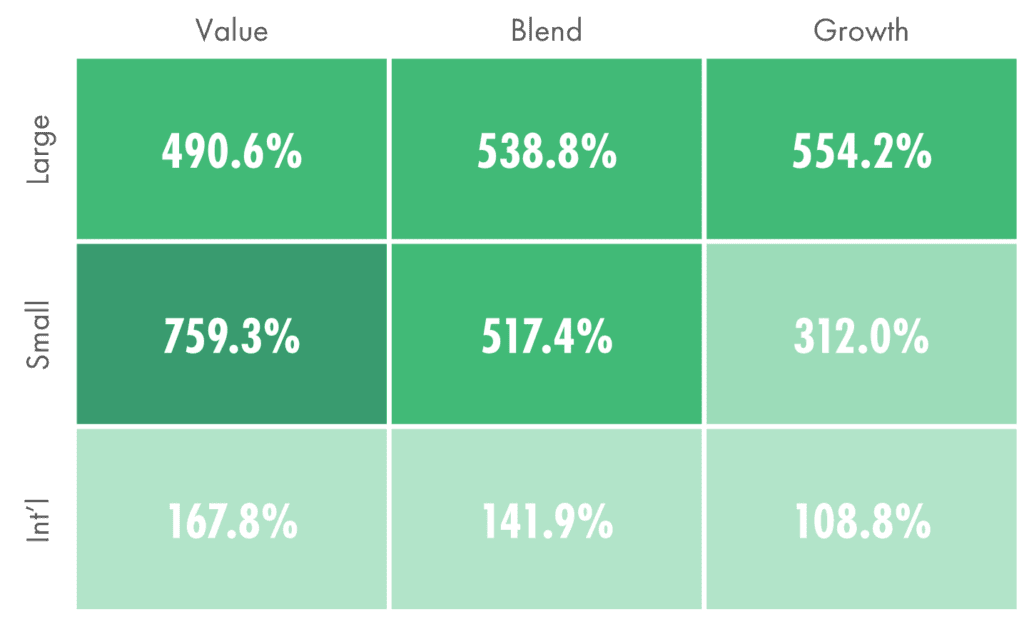

25 Year Gains

Cumulative Total Returns By Equity Style January 2000 – December 2024

S&P Inflection Points

Closing Price and Forward Price-to-Earnings Summary, January 2000 – December 2024

Federal Budget Adversity

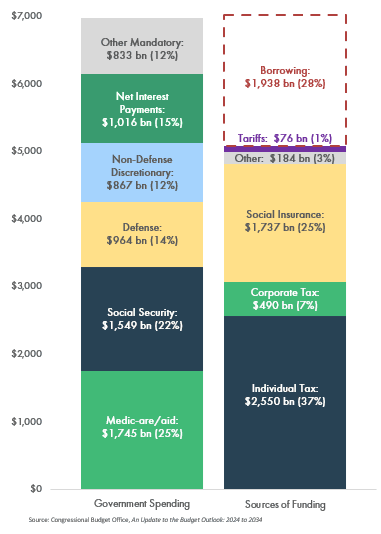

Longer-term, the U.S. economy faces a fiscal trainwreck. The U.S. budget deficit was an astounding $2.2 trillion in 2024, up from $2.0 trillion in 2023. This persistent growth, despite the end of COVID-related stimulus, underscores deeper structural imbalances in federal spending and revenue.

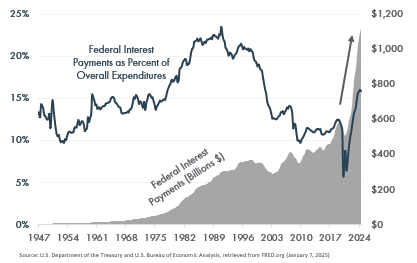

Funding the deficit has created a vicious cycle of government borrowing, further exacerbated by higher interest rates. Federal debt has ballooned to $36 trillion, or approximately 125% of GDP, a post-WWII record. Government spending on interest payments alone is more than the Pentagon’s defense budget.

Washington faces mounting pressure to address the widening gap between spending and revenue. Stabilizing the debt-to-GDP ratio will likely require difficult decisions. DOGE, the new Department of Government Efficiency, headed by Elon Musk and Vivek Ramaswamy, seeks to reduce government spending by $500 billion. Entitlements such as Social Security and Medicare, however, seem untouchable to either party. As a result, deep cuts will be a challenge.

Compound Interest

Federal Investment Payments, Dollars and Percent of Overall Expenditures;

January 1947 – July 2024

More Deficits Are Expected

2025 CBO Baseline Forecast, USD Billions

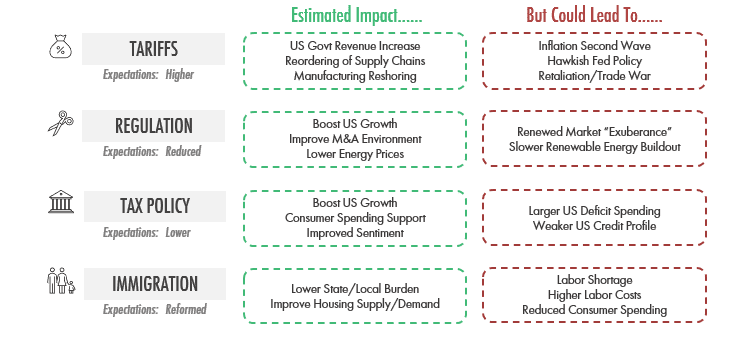

Policy Changes on the Horizon

The “soft landing” scenario endures, but challenges remain. Nevertheless, monetary policy is easing, consumer and capital spending is growing at a reasonable pace, housing supply should slowly improve, and debt delinquency rates are relatively low.

The incoming administration’s proposed policies, such as higher tariffs, will likely ripple through markets both negatively and positively. Tariffs may temporarily drive inflation higher, but their impact could be mitigated by global price adjustments. Meanwhile, lower tax policies and less regulation may help consumers, but further deficit-driven spending raises questions about long-term fiscal sustainability.

The combination of trade tensions, rising deficits, and geopolitical uncertainty is likely to test market resilience in 2025.

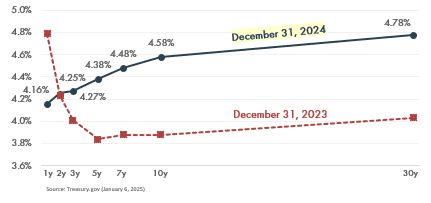

Yield Curve

U.S. Treasury Notes

U.S. Outpacing International

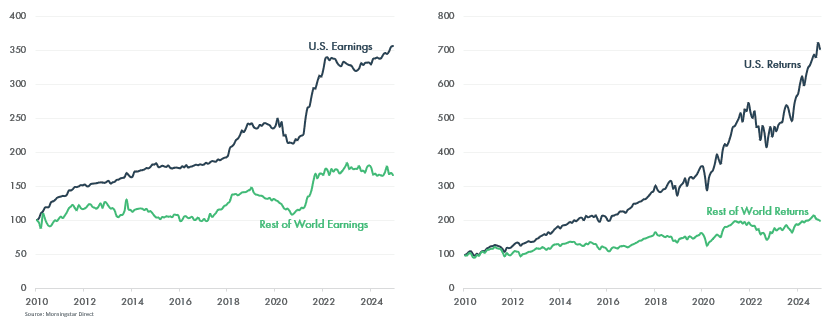

U.S. stock markets continue to outperform international markets, driven by significantly stronger earnings growth, fueled by economic resilience, productivity gains, and technological innovation. This trend may persist as U.S. companies benefit from robust consumer spending, sustained corporate profitability, and a regulatory environment ripe for innovation.

While international stocks have generated positive returns, they continue to face structural and cyclical challenges. Trade policy uncertainty, including potential tariffs from the new U.S. administration, and slower economic growth in key export-driven economies like China, Germany, and Japan have weighed on valuations. Additionally, a strong U.S. dollar – often supported by relatively higher domestic interest rates and economic growth – poses a continuing headwind for international returns.

Despite headwinds, international stocks have discounted valuations relative to U.S. stocks and offer more attractive dividend yields. While near-term momentum favors U.S. markets, international exposure remains important for long-term portfolio diversification.

Earnings Driving Returns

S&P 500 (U.S.) and MSCI ACWI Ex USA (Rest of World) Earnings (Left Side) and Total Returns (Right Side); Indexed to 100 at Start of 2010

© 2025 The Finerty Team

The S&P 500 Index is a free-float capitalization-weighted index of the prices of approximately 500 large-cap common stocks actively traded in the United States. The Bloomberg US Aggregate Bond Index is a broad base, market capitalization-weighted bond market index representing intermediate term investment grade bonds traded in the United States. The Consumer Price Index (CPI) is a measure of the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services.

Advisory services offered by Moneta Group Investment Advisors, LLC, (“MGIA”) an investment adviser registered with the Securities and Exchange Commission (“SEC”). MGIA is a wholly owned subsidiary of Moneta Group, LLC. Registration as an investment advisor does not imply a certain level of skill or training. The information contained herein is for informational purposes only, is not intended to be comprehensive or exclusive, and is based on materials deemed reliable, but the accuracy of which has not been verified.

Trademarks and copyrights of materials referenced herein are the property of their respective owners. Index returns reflect total return, assuming reinvestment of dividends and interest. The returns do not reflect the effect of taxes and/or fees that an investor would incur. Examples contained herein are for illustrative purposes only based on generic assumptions. Given the dynamic nature of the subject matter and the environment in which this communication was written, the information contained herein is subject to change. This is not an offer to sell or buy securities, nor does it represent any specific recommendation. You should consult with an appropriately credentialed professional before making any financial, investment, tax or legal decision. An index is an unmanaged portfolio of specified securities and does not reflect any initial or ongoing expenses nor can it be invested in directly. Past performance is not indicative of future returns. All investments are subject to a risk of loss. Diversification and strategic asset allocation do not assure profit or protect against loss in declining markets. These materials do not take into consideration your personal circumstances, financial or otherwise.