Compardo, Wienstroer & Janes – Garrett Reeg, MBA, CFP®

For many HNW families, preserving wealth across generations is about more than just numbers — it’s about control, protection, and shared values. Trusts are a vital part of that equation, offering a way to manage how and when wealth is distributed.

When it comes to IRAs, however, naming a trust as the beneficiary can be both an opportunity and a challenge. Trusts can have significant advantages, but they also introduce complex tax rules and must be drafted carefully. The key to the best possible outcome is selecting the right trust type and ensuring it is coordinated thoughtfully with current tax laws.

Why HNW Families Use Trusts as IRA Beneficiaries

- Asset Protection: Trusts can shield inherited assets from creditors, lawsuits, or divorce settlements.

- Control Over Distributions: A trust can allow you to determine how and when funds are accessed, which is especially valuable when heirs are young, inexperienced, or have differing financial values.

- Estate Tax Benefits: Properly structured trusts can help exclude IRA assets from a beneficiary’s estate, protecting them from future estate taxes.

Example: A family matriarch wants to ensure her $8M IRA isn’t exposed to her adult child’s risky business ventures or potential divorce. By naming a trust, she protects the ssets while providing structured distributions.

Drafting Considerations for HNW Estates

One common approach for HNW families is a “see-through trust”, which allows the IRS to look through the trust to the underlying individual beneficiaries for distribution purposes. If drafted correctly, these trusts can provide control and protection while still complying with required distribution rules.

For a trust to qualify as a “see-through trust” it would have the following:

- All beneficiaries must be identifiable individuals (no charities as remainder beneficiaries).

- A copy must be provided to the IRA custodian by October 31 of the year following death.

- Language must align with the Secure Act’s 10-year payout rule.

Failure to meet these requirements can result in accelerated taxation, potentially forcing the IRA to be distributed and taxed much sooner than intended.

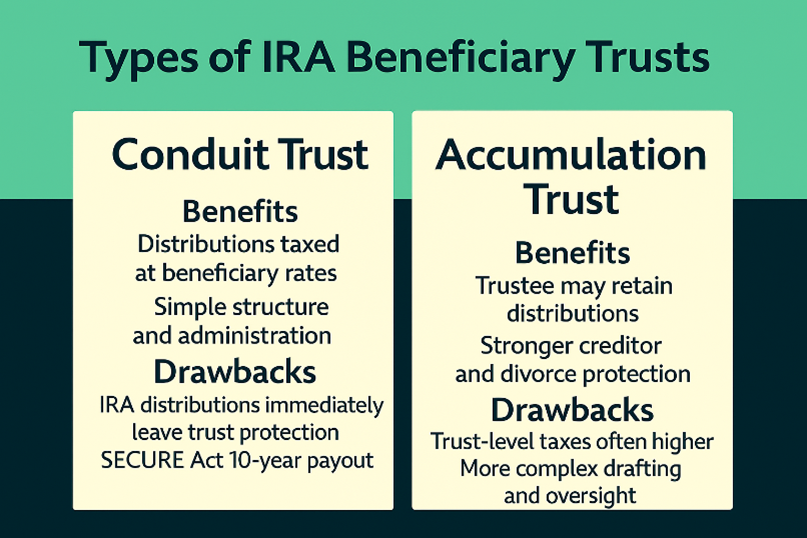

Outright Beneficiaries vs. Trust Beneficiaries

For individuals with significant IRA assets, a key decision is naming the beneficiary of your IRA.

- Outright beneficiaries are often simpler and can result in lower income taxes, since trusts reach the highest tax brackets quicker.

- Trust beneficiaries provide control, protection and flexibility. A properly drafted trust can:

- Pass IRA distributions to the beneficiary (along with the income tax liability)

- Retain distributions inside the trust when asset protection or estate considerations outweigh potential income tax benefits

Before naming a trust as your IRA beneficiary, work closely with your estate planning attorney and wealth advisor to ensure the structure aligns with both IRS rules and your family’s priorities.

The key decisions you make now can save your heirs time, money and frustration for years to come.

Contact me at greeg@monetagroup.com.

© 2026 Advisory services offered by Moneta Group Investment Advisors, LLC, (“MGIA”) an investment adviser registered with the Securities and Exchange Commission (“SEC”). MGIA is a wholly owned subsidiary of Moneta Group, LLC. Registration as an investment adviser does not imply a certain level of skill or training. The information contained herein is for informational purposes only, is not intended to be comprehensive or exclusive, and is based on materials deemed reliable, but the accuracy of which has not been verified.

Trademarks and copyrights of materials referenced herein are the property of their respective owners. Index returns reflect total return, assuming reinvestment of dividends and interest. The returns do not reflect the effect of taxes and/or fees that an investor would incur. Examples contained herein are for illustrative purposes only based on generic assumptions. Given the dynamic nature of the subject matter and the environment in which this communication was written, the information contained herein is subject to change. This is not an offer to sell or buy securities, nor does it represent any specific recommendation. You should consult with an appropriately credentialed professional before making any financial, investment, tax or legal decision. An index is an unmanaged portfolio of specified securities and does not reflect any initial or ongoing expenses nor can it be invested in directly. Past performance is not indicative of future returns. All investments are subject to a risk of loss. Diversification and strategic asset allocation do not assure profit or protect against loss in declining markets. These materials do not take into consideration your personal circumstances, financial or otherwise.