Aoifinn Devitt | Chief Investment Officer

Chris Kamykowski CFA®, CFP® | Head of Investment Strategy & Research

The second quarter was dominated by the Fed finally moving to interest rate “lift-off” and beyond, growing inflation fears, and a lackluster market backdrop.

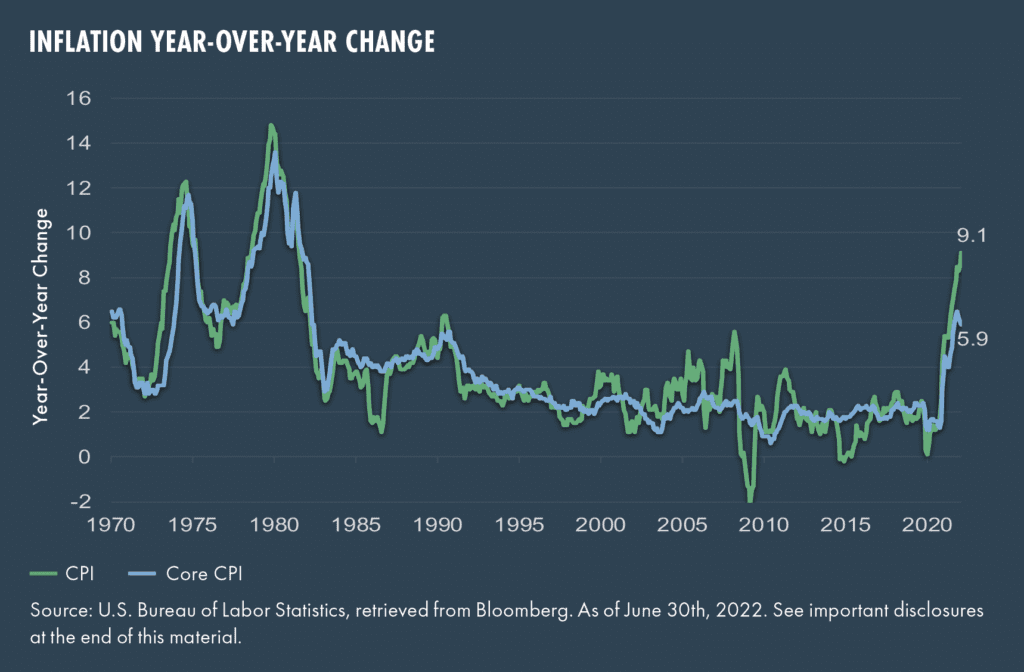

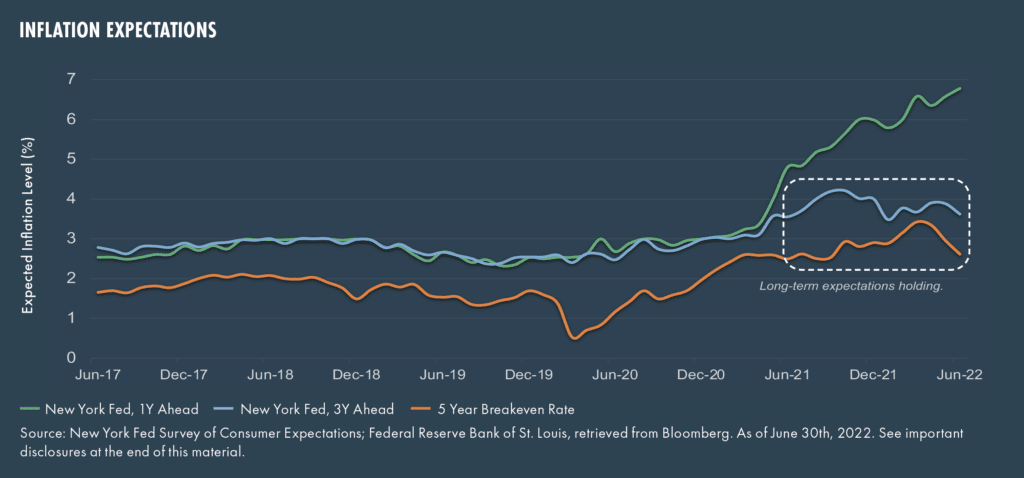

Inflation remained stubbornly high over the quarter, reaching another 40-year high of 9.1% annualized in June. Core inflation (the inflation level with the typically more volatile prices of energy and food stripped out) was higher too, at 5.9%, having essentially remained flat for the best part of the last 30 years. This stark shift in both inflation expectations and realized pricing shook markets and forced the Fed to take a more assertive stance than previously. When it comes to inflation expectations though, while they remain elevated in the short run, in the long and medium term they are somewhat more muted, suggesting that many market participants believe some of the drivers of inflation remain transitory, or that the economy will contract in the medium term to bring it into check.

The inflationary waves were felt globally, particularly in Europe, which is experiencing not only the imported inflation effect of a weaker currency (which briefly fell through parity with the US dollar in July) but also acute uncertainty regarding its energy supply, given its reliance on Russia for natural gas supplies. As summer turns to fall and winter, the question of energy supply and the potential for rationing and steeper prices is casting a pall over European area growth outlooks.

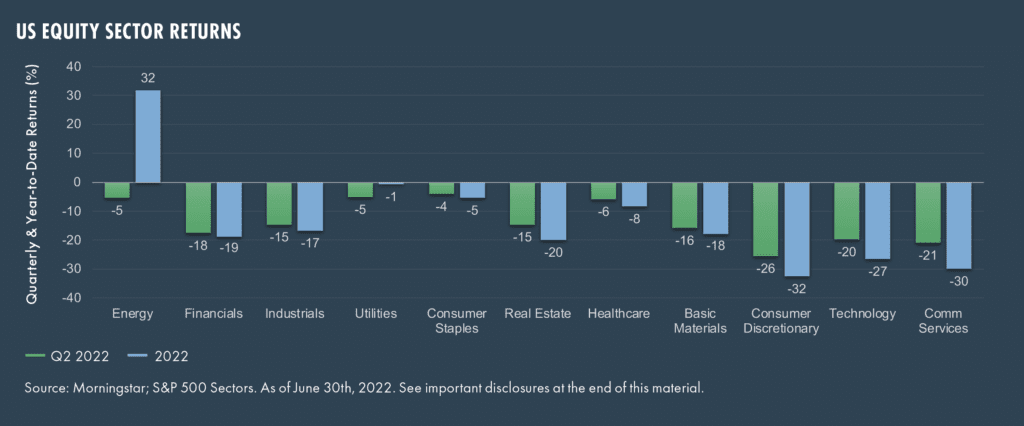

Inflation creates tremendous uncertainty for corporate outlooks too, and earnings releases have been laden with caution and inklings of demand weakening for many months now. This uncertainty was felt universally in the second quarter, across all sectors, although certain sectors such as financials, consumer discretionary, technology, and communication services led in terms of negative returns, which is particularly interesting given the rising rate environment. The energy sector was slightly weaker due to the decline in oil prices, but it remained robust relative to the bulk of the market.

As noted previously, the Federal Reserve hiked rates twice over the quarter, with hikes of 50 and 75 bps in May and June, respectively, in a stark reversal to its previous near-complacency about rising inflation. A new “highly attentive” positioning is the norm, although at mid-year it is unclear how long the current trajectory will last.

Given the interest rate backdrop, the first start to the year was an exceptionally poor one for traditional balanced portfolios, due to the decline in bonds as well as equities. In fact, the second quarter was the worst quarterly return for a 60/40 blend over the past 50 years with a return of -11.8%, and negative returns for a quarter have only occurred 22% of the time.

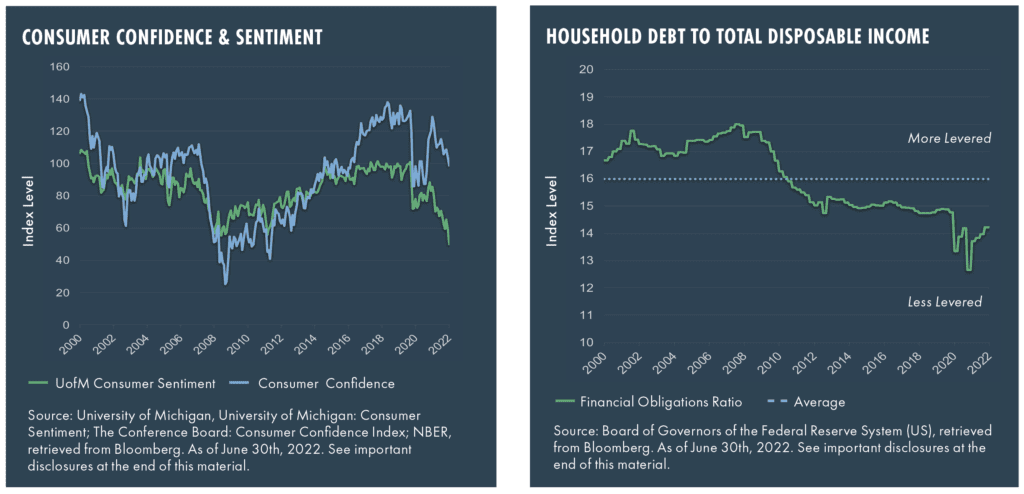

Economic indicators continue to be mixed, with the labor picture continuing to buck the trend of softening economic signals. Just in the past few weeks, there have been some anecdotes from companies that hiring is slowing and some layoff waves have been announced. The strength of labor is a key indicator to watch as it relates to economic health and the levels of consumer confidence. As the charts below show, consumer sentiment has recently dipped, although household debt to total disposable income remains below average, suggesting some resilience and staying power despite rising rates and prices.

Markets had an exceptionally poor start to the year, with the S&P 500 (-16.10% for the quarter, -19.96% YTD) showing its worst first half to the year in 100 years, with only emerging markets slightly bucking the trend by delivering a slightly less negative -17.63% for the year, and -11.45% for the quarter. Bonds shed -4.69% (Bloomberg US Aggregate) bringing their year-to-date return to -10.35%, while high yield and investment grade were even more negative. Bonds displayed one of their worst starts to the year since 1990.

Alternatives such as MLPs and infrastructure equities remained true to their defensive orientation to protect capital somewhat, although their performance was still negative (-7.38% and -7.66%, respectively), while REITs sold off more dramatically (-18.1% for the quarter) given the worsening outlook for real estate as mortgage rates rose and economic indicators faltered.

Final Thoughts

As we look to the second half of the year, the Biden administration looks poised to have achieved legislative success with the passing of the CHIPs+ bill as well as the likely passing of an iteration of the former Build Back Better initiative, which will be encouraging to a market jaded by the appearance of political gridlock. The mid-term elections and their uncertainty continue to loom, and it is reasonable to expect more market volatility in their wake.

As the summer draws to a close, the frenzy of a surge in travel, staffing shortages, and delays should ebb, and as “back to school” beckons the real state of the economy may gather more scrutiny. The stark correction in equities as well as attractive bond (and even cash) yields have forced investors to take another look at the return expectations for various asset classes.

We are settling in to our post-Covid normal and while much uncertainty remains, we are starting to see the shape of how our work lives might look. Perhaps Covid has given us some immunity – to shocks, uncertainty, and the unexpected. As markets cope with a new set of records in terms of inflation and interest rate rises, perhaps that resilience will come to the fore. It will be a crucial, testing time, but, as always, we don’t believe in timing markets nor that calling a “bottom” or inflection point is possible. Our advice remains to retain a broad-based diversified exposure with a solid asset class mix, including inflation-hedging assets such as real estate, real assets, and infrastructure. We believe in preparation and not prediction.

Have Questions?

If you have questions or need to discuss your investment strategy, feel free to contact us.

Definitions

Alerian MLP Index: The Alerian MLP Index is a capped, float-adjusted, capitalization-weighted index, whose constituents earn the majority of their cash flow from midstream activities involving energy commodities.

The S&P 500 Index is a free-float capitalization-weighted index of the prices of 500 large-cap common stocks actively traded in the United States.

Emerging Markets are represented by the MSCI Emerging Markets Index, a float-adjusted market capitalization index that consists of indices in 21 emerging economies.

The Bloomberg U.S. Aggregate Bond Index is an index, with income reinvested, generally representative of intermediate-term government bonds, investment grade corporate debt securities and mortgage-backed securities.

Investment grade bonds are represented by the Bloomberg US Corporate Bond Index, which measures the investment grade, fixed-rate, taxable corporate bond market. It includes USD-denominated securities publicly issued by US and non-US industrial, utility, and financial issuers.

High-yield bonds are represented by the Bloomberg US Corporate High Yield Bond Index, which measures the USD-denominated, high yield, fixed-rate corporate bond market. Securities are classified as high yield if the middle rating of Moody’s, Fitch and S&P is Ba1/BB+/BB+ or below. Bonds from issuers with an emerging markets country of risk, based on the indices’ EM country definition, are excluded.

Master Limited Partnerships (MLPs) are represented by the Alerian MLP Index, which is the leading gauge of energy infrastructure Master Limited Partnerships (MLPs). The capped, float-adjusted, capitalization-weighted index, whose constituents earn the majority of their cash flow from midstream activities involving energy commodities, is disseminated in real-time on a price-return basis (AMZ) and on a total-return basis (AMZX).

Real Estate Investment Trusts (REITs) are represented by the FTSE Nareit All Equity REITs Index, which is a free-float adjusted, market capitalization-weighted index of U.S. equity REITs. Constituents of the index include all tax-qualified REITs with more than 50 percent of total assets in qualifying real estate assets other than mortgages secured by real property.

Infrastructure is represented by the S&P Global Infrastructure Index, which provides liquid and tradable exposure to 75 companies from around the world that represent the listed infrastructure universe. The index has balanced weights across three distinct infrastructure clusters: Utilities, Transportation, and Energy.

The Consumer Price Index (CPI) is a measure of the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services.

The Core Consumer Price Index (CPI) is an aggregate of prices paid by urban consumers for a typical market basket of consumer goods and services, excluding food and energy.

The New York Fed, one-year ahead expected inflation rate, is the median expectation from all respondents to the New York Fed Survey of Consumer Expectations when asked for their expectations for inflation/deflation over the next 12 months.

The New York Fed, three-year ahead expected inflation rate, is the median expectation from all respondents to the New York Fed Survey of Consumer Expectations when asked for their expectations for inflation/deflation over the next 36 months.

The five-year breakeven inflation rate represents a measure of expected inflation derived from 5-Year Treasury Constant Maturity Securities and 5-Year Treasury Inflation-Indexed Constant Maturity Securities. The latest value implies what market participants expect inflation to be in the next 5 years, on average.

The 60/40 blend is a hypothetical portfolio constructed as 60% S&P 500 TR USD and 40% Bloomberg Government/Credit.

The US Index of Consumer Sentiment (ICS), as provided by the University of Michigan, tracks consumer sentiment in the US, based on surveys on random samples of US households. The index aids in measuring consumer sentiments in personal finances, and business conditions, among other topics.

The Consumer Confidence Index (CCI) is a survey, administered by The Conference Board, that measures how optimistic or pessimistic consumers are regarding their expected financial situation.

© 2022 Moneta Group Investment Advisors, LLC. All rights reserved. Moneta Group Investment Advisors, LLC is an SEC registered investment advisor and wholly owned subsidiary of Moneta Group, LLC. Registration as an investment advisor does not imply a certain level of skill or training. These materials were prepared for informational purposes only based on materials deemed reliable, but the accuracy of which has not been verified. Trademarks and copyrights of materials referenced herein are the property of their respective owners. Index and/or Style returns reflect total return, assuming reinvestment of dividends and interest. The returns do not reflect the effect of taxes and/or fees that an investor would incur. Examples contained herein are for illustrative purposes only based on generic assumptions. Given the dynamic nature of the subject matter and the environment in which this communication was written, the information contained herein is subject to change. This is not an offer to sell or buy securities, nor does it represent any specific recommendation. You should consult with an appropriately credentialed professional before making any financial, investment, tax or legal decision. You cannot invest directly in an index. Past performance is not indicative of future returns. All investments are subject to a risk of loss. Diversification and strategic asset allocation do not assure profit or protect against loss in declining markets. These materials do not take into consideration your personal circumstances, financial or otherwise.