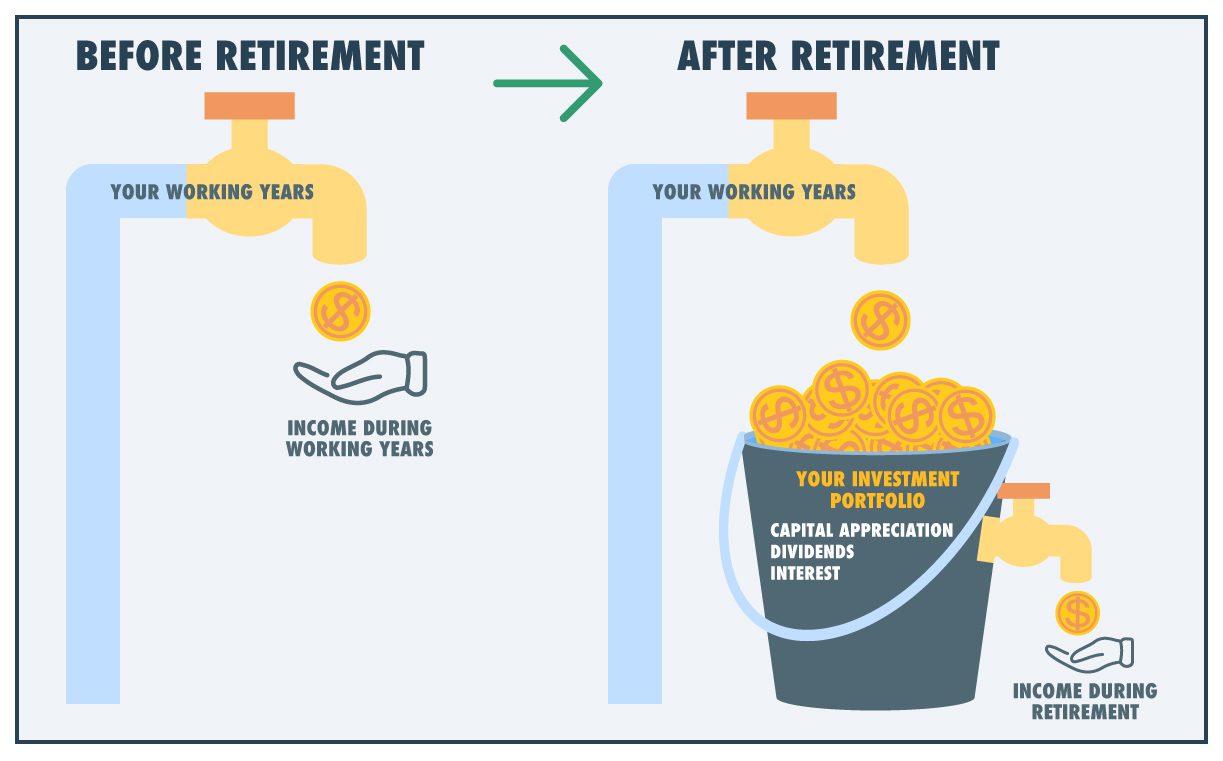

When you retire, the typical paycheck from your employer stops coming, but your income needs do not necessarily stop coming.

Instead, you may start to rely on your investment portfolio to replace your salary with standard withdrawals called remittances. This remittance is a combination of interest income from bonds, dividend income from stocks, and capital appreciation from the portfolio.

Your Moneta advisor can help you optimize your remittance strategy based on your assets, age, income sources, tax considerations, risk tolerance, and other factors.

Tax Strategy

The rules for withdrawing from retirement accounts can be complex.

At a high level, we recommend drawing down taxable accounts first, followed by tax-deferred accounts while saving tax-free accounts last.

At a more tactical level, there may be nuances to your specific situation that affect the optimal timing and execution of withdrawing from certain accounts.

We can work with the goal of making sure you don’t miss any details or opportunities while helping you navigate this process, as well as trying to help you avoid moving into a higher tax bracket or disrupting your asset allocation as a result.

Income Strategy

Remittance isn’t necessarily the only source of retirement income replacing your salary. There are other sources that can come with their own nuances and decision points, so consider an advisor who can help discern which option is best for your circumstances. Here are a couple of examples:

- Pensions and retirement packages: You may have a choice between a lump sum payout or monthly payments, which can be taken immediately or delayed.

- Social Security: From age 62 to 70, your social security benefits increase each year you wait to collect, but there are also situations where it may make sense to claim at the earlier end.

Investment Strategy

The sobering reality of retirement is we don’t know how long it will last. Even with a remittance strategy in place to cover your short-term needs, it’s important to maintain a portfolio with enough growth potential to sustain through a time horizon that may end up longer than expected – especially given the context of current inflation, interest rates, and market volatility.

As you draw down your retirement accounts, we may be able to help with the effort to diversify and optimize your asset allocation in light of your circumstances, market conditions, and other factors.

Contact Us for Assistance

Reach out to us for assistance planning your retirement.

© 2023 Advisory services offered by Moneta Group Investment Advisors, LLC, (“MGIA”) an investment adviser registered with the Securities and Exchange Commission (“SEC”). MGIA is a wholly owned subsidiary of Moneta Group, LLC. Registration as an investment advisor does not imply a certain level of skill or training. The information contained herein is for informational purposes only, is not intended to be comprehensive or exclusive, and is based on materials deemed reliable, but the accuracy of which has not been verified.

Trademarks and copyrights of materials referenced herein are the property of their respective owners. Examples contained herein are for illustrative purposes only based on generic assumptions. Given the dynamic nature of the subject matter and the environment in which this communication was written, the information contained herein is subject to change. This is not an offer to sell or buy securities, nor does it represent any specific recommendation. You should consult with an appropriately credentialed professional before making any financial, investment, tax or legal decision. All investments are subject to a risk of loss. Diversification and strategic asset allocation do not assure profit or protect against loss in declining markets. These materials do not take into consideration your personal circumstances, financial or otherwise.