Chris Kamykowski, CFA, CFP®

The imagery could not have been more surreal…… U.S. President Donald Trump walking through ongoing renovations of the Federal Reserve headquarters in Washington D.C. with the current Fed Chairman, Jerome Powell. Both walked side by side in hard hats and suits as dust swirled and the two “discussed” cost overruns with the current project. This came in the midst of an ongoing public “clash” over the Fed’s current monetary policy, one in which the President has publicly lambasted the Chairman with many colorful complaints over the Fed’s reluctance to ease. The threat of “firing” the current Chairman – who’s term officially ends in May 2026 – has also made headlines and jarred markets in the last couple months. Fears were stoked over the independence of the Fed. Regardless, for all the drama between these two high ranking leaders of the free world, what should investors know or care about the current standoff?

The Current Stances

Both Trump and Powell have their specific reasons for their current stances which is worthwhile to understand. One may characterize Trump’s as more politically and fiscally expedient while Powell reflects a conservative approach to monetary policy decisions and data-dependency.

| Policy Dimension | Donald Trump | Jerome Powell |

| Interest Rate Stance | Advocates for immediate and aggressive rate cuts to 1% or lower. | Prefers holding rates steady at 4.25-4.50% until inflation is clearly under control. |

| Rationale for Position | Believes lower rates will reduce debt servicing costs and stimulate growth. | Emphasizes inflation risks and the need for data-driven decisions. |

| View on Inflation | Downplays inflation risks, arguing tariffs and fiscal policy won’t reignite it. | Sees inflation as still above target and potentially sticky. |

| Economic Outlook | Optimistic; sees tariffs and tax cuts as growth drivers. | Cautious; notes signs of labor market softening and slowing growth. |

Trump clearly sees value and cause for easing as lower rates would help the U.S. Treasury borrow more cheaply on the short end of the curve, helping stem the required spending on deficit spending. Higher rates across the curve on the back of the inflation surge in 2022 has put interest payments neck-in-neck with U.S. defense spending. The prospect of 2026 mid-term elections also looms for those who have supported Trump through thick and thin during the tariff turmoil and passing of the One Big Beautiful Bill Act (OBBB). The fear of a self-induced “recession” also likely looms large given the consequences of uncertainty imparted by the ever-changing tariff regime. A rate cut may be seen as a way to stem a more dire economic slowdown.

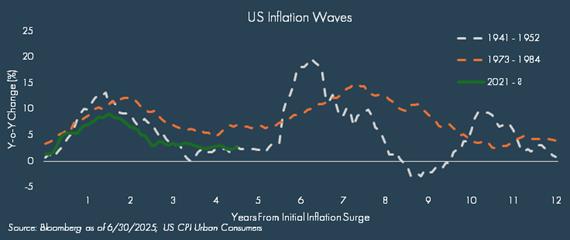

On the Fed side, technically, it is currently in an easing cycle given its last action was to lower rates 25 bps in December 2024, though it has been a pause for five consecutive meetings. The FOMC’s most recent policy update on July 30th kept rates steady in a range between 4.25%-4.5%, with two dissenters (a rarity) arguing for a 25 bps cut. In his commentary following the announcement, Chairman Powell admitted policy was “modestly restrictive” and that the labor market will be a focus as they seek to identify any consistent weakening trends which could lead to further easing.[1] Additionally, Powell noted the impact of tariffs have begun to show but have not yet made a major impact on overall economic activity or inflation. The Fed is all too aware of inflationary regimes and how second waves are possible. A combination of fiscal stimulus, loosening of regulations, and easier monetary policy could result in higher inflation somewhere in the near future.

Perspective on Fed Independence

As noted, this sharp contrast in opinions regarding monetary policy has led to explicit statements by Powell and many market pundits on maintaining the integrity of the Fed’s independence even as outright threats have circulated through social media. Trump’s threats to fire Powell, or to preemptively name his successor, pose significant risks to the Fed’s credibility. Markets rely on the central bank’s independence to anchor inflation expectations and stabilize long-term interest rates. Undermining that independence could lead to higher borrowing costs, a weaker dollar, and increased market volatility

That said, pressure on the Fed from the political wing of our country is nothing new, for better or worse. Indeed, even after the Treasury-Fed Accord in 1951, which solidified the Federal Reserve’s independence, political leaders have often sought to influence monetary policy. The following examples highlight pressures during the Vietnam War and the previous round of high inflation in the late 70s/early 80s:

1965: President Lyndon B. Johnson vs Fed Chair William Martin, Jr.

“[Martin] even survived the most brutal attack on a Fed chairman by a president, after his decision to hike rates just as the Vietnam War was ramping up in 1965 incurred Lyndon Johnson’s ire. Martin was invited to LBJ’s ranch in Texas, where the president — as much a bully as Trump, in his own way — physically pushed him around the room, yelling, ‘Martin, my boys are dying in Vietnam, and you won’t print the money I need.’”[2]

1979: U.S. Congress and Treasury Secretary vs Fed Chair Paul Volcker

“With interest rates high in the Volcker-led fight on inflation, the attacks came from both political parties. ‘We are destroying the small businessman. We are destroying Middle America. We are destroying the American dream,’ conservative Congressman George Hansen said during a 1981 hearing. A couple of weeks later, Treasury Secretary Donald Regan directly criticized the Fed’s position during an interview with a New York Times reporter. ‘What I am suggesting is that if (money supply growth) stays here, you’re going to have a severe recession,’ said Regan, who then went on to suggest how the money supply needed to be adjusted going forward.” [3]

Key for Powell and the Fed is to maintain independence in their decision-making without looking like any decision is induced by abundant political pressure. Their consistent statements regarding “data dependency” point to the awareness of remaining steady as political headwinds blow their way.

Is One Side More “Right”?

Timing appropriate monetary policy for current or expected economic conditions is a tough task made more difficult by changing market conditions, expectations, and outlooks. With the myriad of economic data available, two sides of an argument can find data points to support their particular view.

The Fed’s most recent decision to keep the benchmark rate at 4.25%–4.50% reflects a nuanced economic picture. Inflation has cooled but remains sticky, especially with new tariffs and geopolitical risks on the horizon. Unemployment is low, and GDP growth has moderated but not stalled. The Fed’s own projections still pencil in two rate cuts for 2025, but officials are in no rush to act prematurely. Easing rates while the economy is not observably stalling, is not the typical routine of the Fed and certainly not a pressing option when tariffs cloud the inflation outlook. While Trump touts wanting to lower rates to help home buyers as they stare at high 6-7% mortgage rates, the fact is easing policy primarily affects the short end of the curve. 10- and 30-year tenors of the Treasury curve, where mortgages are priced, are more linked to inflation expectations and demand/supply dynamics. Additionally, financial conditions are not necessarily restrictive (higher is more accommodative), M2 money growth has steadily increased, and the Real Fed Funds rate is at 1.7%, slightly north of its 1.5% average since 1960.

To be sure, payroll growth of 73K in July and a 250K+ plus revision downward for May and June did not exactly paint a promising picture for employment trends recently. However, alongside the impact to hiring decisions for business due to the uncertainty around tariffs, the Peterson Institute for International Economics has also recently noted that the “breakeven” growth rate for payroll may be lower than our recent past, requiring an update to the market’s reference point for a suitable monthly print. The Institute estimates a breakeven rate of 86K given the slowing population growth which has not been helped by the fall in immigration this year. [4]

What Now?

In short: a delicate balance. As the U.S. economy navigates a complex post-pandemic recovery, a sharp divide has emerged between Federal Reserve Chair Jerome Powell and U.S. President Donald Trump over the future of interest rates. Trump has argued for a slashing of the federal funds rate, suggesting that such a move would ease the government’s debt burden and stimulate growth. Powell, however, has held firm, citing persistent inflation risks and the Fed’s dual mandate of price stability and full employment. Ultimately this standoff is more than a political spat – it’s a test of institutional resilience.

As Powell navigates the final stretch of his term, he appears committed to data-driven policy, even in the face of mounting political pressure that sees no abating. We are at an inflection point, where the timing of if, and when, to cut is subject to genuine debate. Currently, Powell sees more “pain” from acting too quickly (inflation), while Trump sees more “pain” by acting too late (recession). Ultimately, there are no winners from a biased Fed shifting its policy based on political whims. Luckily, Powell does not actually sit on any “throne” whereby he is able to dictate policy; the decision to lower or raise rates does not reside solely with him. There are 12 voting members on the Federal Open Market Committee (FOMC) which ultimately sets monetary policy. It is their collective resolve that will shape not only the Fed’s legacy but also the trajectory of the U.S. economy.

DEFINITIONS

Real Fed Funds Rate – Reflects the actual cost of borrowing after accounting for the impact of inflation as measured by PCE.

M2 – Consists of M1 plus (1) savings deposits (including money market deposit accounts); (2) small-denomination time deposits (time deposits in amounts of less than $100,000) less individual retirement account (IRA) and Keogh balances at depository institutions; and (3) balances in retail money market funds (MMFs) less IRA and Keogh balances at MMFs.

Bloomberg US Financial Conditions Index – Tracks the overall level of financial stress in the U.S. money, bond, and equity markets to help assess the availability and cost of credit. A positive value indicates accommodative financial conditions, while a negative value indicates tighter financial conditions relative to pre-crisis norms.

DISCLOSURES

© 2025 Advisory services offered by Moneta Group Investment Advisors, LLC, (“MGIA”) an investment adviser registered with the Securities and Exchange Commission (“SEC”). MGIA is a wholly owned subsidiary of Moneta Group, LLC. Registration as an investment adviser does not imply a certain level of skill or training. The information contained herein is for informational purposes only, is not intended to be comprehensive or exclusive, and is based on materials deemed reliable, but the accuracy of which has not been verified.

Trademarks and copyrights of materials referenced herein are the property of their respective owners. Index returns reflect total return, assuming reinvestment of dividends and interest. The returns do not reflect the effect of taxes and/or fees that an investor would incur. Examples contained herein are for illustrative purposes only based on generic assumptions. Given the dynamic nature of the subject matter and the environment in which this communication was written, the information contained herein is subject to change. This is not an offer to sell or buy securities, nor does it represent any specific recommendation. You should consult with an appropriately credentialed professional before making any financial, investment, tax or legal decision. An index is an unmanaged portfolio of specified securities and does not reflect any initial or ongoing expenses nor can it be invested in directly. Past performance is not indicative of future returns. All investments are subject to a risk of loss. Diversification and strategic asset allocation do not assure profit or protect against loss in declining markets. These materials do not take into consideration your personal circumstances, financial or otherwise.

[1] https://www.federalreserve.gov/mediacenter/files/FOMCpresconf20250730.pdf

[2] https://www.bloomberg.com/opinion/articles/2025-07-18/what-happened-the-last-time-a-fed-chief-was-bounced?srnd=phx-economics-v2&embedded-checkout=true

[3] https://www.federalreservehistory.org/essays/anti-inflation-measures

[4] https://www.piie.com/publications/policy-briefs/2025/us-population-growth-slows-we-need-reset-expectations-economic-data