The year 2024 is now quickly in the rearview mirror as 2025 has already brought its fair share of events, including snowstorms in in the South and Midwest, wildfires in LA, Bird Flu on the rise, an incoming US president threatening a takeover of Greenland, and a rapidly rising 10-Year Treasury yield quickly reshaping the investment landscape. Nevertheless, there were some significant events that happened last quarter, including the election of Donald Trump for US president – the first non-consecutive president since Grover Cleveland in the late 1800s. Fourth quarter reviews often necessitate a look back at the entire year, so in this Quarterly Report, we’ll review some of the key themes from Q4 and 2024 while providing some insights for the year ahead.

Economic Update

We’ll begin with the major component driving everything: the global economy. In short, it’s hanging in there, although trajectories for major economic powers are certainly mixed.

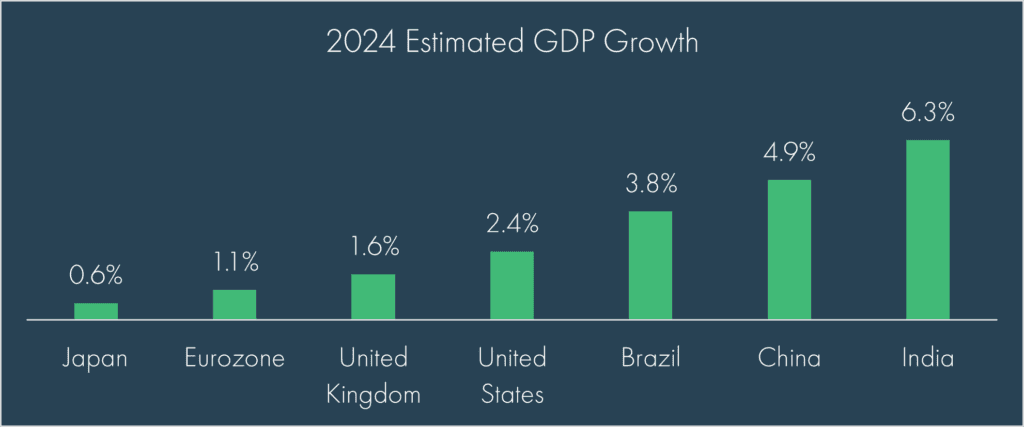

Looking at the largest economy in the world, the US has “miraculously” found itself looking at a “soft-landing” at worst and further expansion at the best. US voter’s call for Trump 2.0 has created confidence in economic momentum continuing, and alongside the artificial intelligence (AI) “revolution” it seems destined to remain strong enough to avoid a recession in the near-term. That said, unexpected impacts of potential policy changes and a worrisome fiscal situation remain key wild cards to the positive narrative.

Meanwhile, the second largest economy (China) is projected to post a near 5% estimated growth rate for 2024, just shy of their targeted policy rate. However, it remains seemingly trapped between, on one side, a lingering overextension in housing, local debt levels and demographic pressures, while on the other side, a government seeking to deliberately contain monetary policy measures to right the economic trajectory for the long-term. It still remains to be seen if parallel fiscal and additional monetary injections will be pushed forward to stimulate domestic demand. And of course, reliance on exports and the threat of US tariffs creates natural trepidation – more on that below.

In Europe, a war in its eastern theater, upheaval in the political establishment, reliance on China’s growth by its main economy (Germany), and a relatively less dynamic economy, has the Eurozone hanging on to growth by a thread. The area remains firmly in an easing-cycle to help support the broader economy with major economic engines such as France and Germany facing headwinds and fiscal constraints.

In Japan, positive growth of any sort alongside stronger positive inflation readings are welcome as the country is exiting a decades long period of stagnant growth and deflationary pressures. Policy makers have enacted market reforms to help drive corporate margin expansion and profits which are expected to help stimulate the economy. Still, demographics remain a notable issue for them with population a key component in driving any country’s growth.

Source: Bloomberg as of January 10th, 2025; please see important disclosures at the end of this material.

Monetary Policy

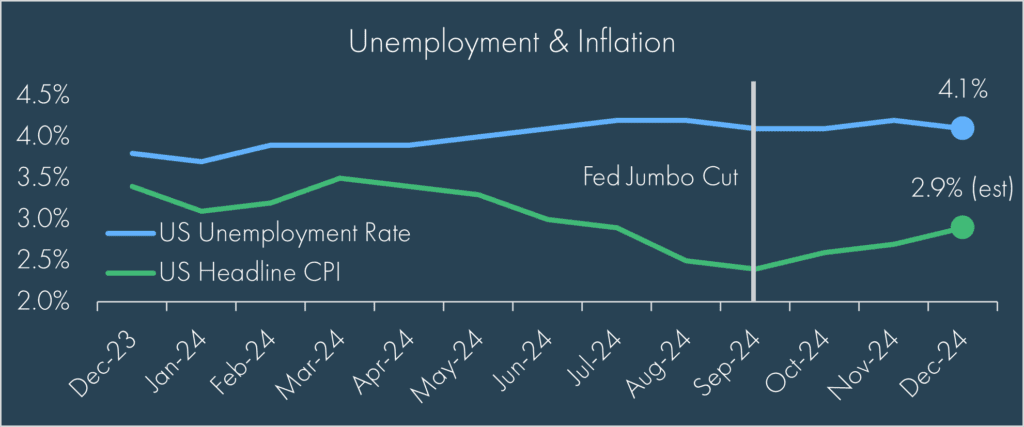

At their September FOMC meeting, the Federal Reserve began the rate cutting cycle, surprising markets with a 50-basis point (bps) rate cut, compared to an expected cut of 25 bps. At the time of their meeting, the Fed was seeing warning signals of a deteriorating employment picture and inflation continuing its slow grind lower, with a 2.4% YoY headline inflation reading coming in just days prior to their meeting. The so-called “jumbo” rate cut quickly seemed overdone, as employment stabilized, and inflation moved higher – resulting in multiple “resets” over the quarter of investor expectations for additional rate cuts in the subsequent months and 2025.

Source: Bloomberg as of January 10th, 2025; please see important disclosures at the end of this material.

Looking ahead, the Fed has signaled expectations for two rate cuts in 2025 and two rate cuts in 2026; this is already seen as overly optimistic by markets, which, as we write, are currently pricing in just two total rate cuts in 2025 and 2026.

Elections and Fiscal Policy

Many labeled 2024 as the “year of elections”, with more than 4 billion people around the world voting in key elections in their respective regions – none more important to US investors than US elections in November, where the Republican party achieved a clean (albeit narrow) sweep of the House, Senate, and Presidency. We’ll have more on the market’s reaction momentarily, but as Trump prepares to take office in a matter of days, two key policy items have risen to the forefront of investors’ minds: Tariffs and Fiscal Policy. There are more to be sure, including immigration, which could have implications for the labor market and wages.

We wrote more on tariffs here, but in short: investors are grappling with how much of Trump’s proposed tariffs are real and how much are negotiating tactics. Tariffs can raise revenue, can serve as a catalyst to bring jobs home, and can shift supply chains to more accommodative trading partners, however, they can also lead to higher prices, which could have secondary effects of a more hawkish Fed introducing tighter monetary policy, and retaliatory tariffs further reshaping global trade, which could ultimately drag on growth. Few expect all proposed tariffs to be implemented, though consensus seems to lie with China once again receiving the brunt of tariff increases.

US government finances are also a topic that will be top of mind this year. Many are aware of the challenging situation, including rising deficits, an increasing interest burden, and limited political appetite to adjust spending or raise taxes. There are no painless solutions, which we discuss in more detail here, but doing nothing could also bring its own kind of pain, as seen in recent weeks as the long-end of the Treasury curve jumped to its highest point since last May.

All told, with the optimism of Trump 2.0 in markets comes the uncertainty of a leader who likes big and bold deals. Markets are quick to price in news generated from social media posts, but there is also a limit to how much power the president actually has. For many reasons, 2025 is poised to be another interesting year.

Markets

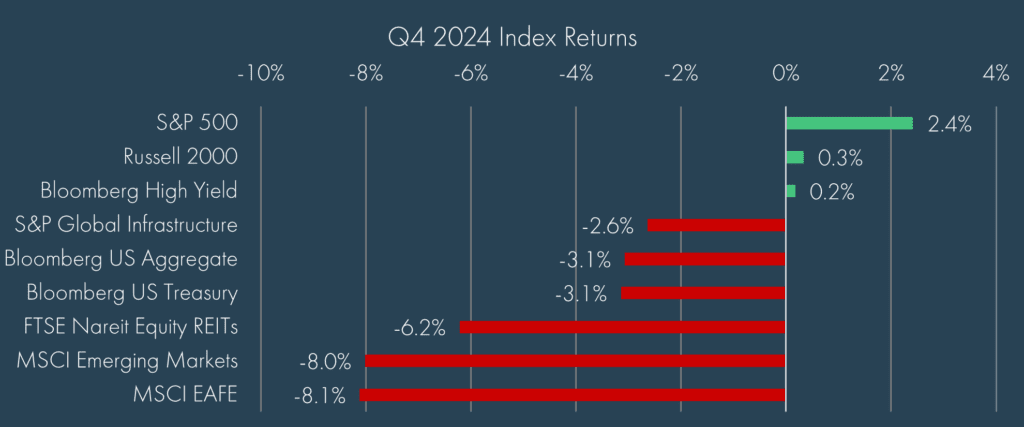

It was a tough quarter to close out what had been an otherwise great year for markets, with rate expectations weighing on most asset classes outside of US Large Cap, which benefitted once again from AI optimism.

Source: Morningstar as of December 31st, 2024; please see important disclosures at the end of this material.

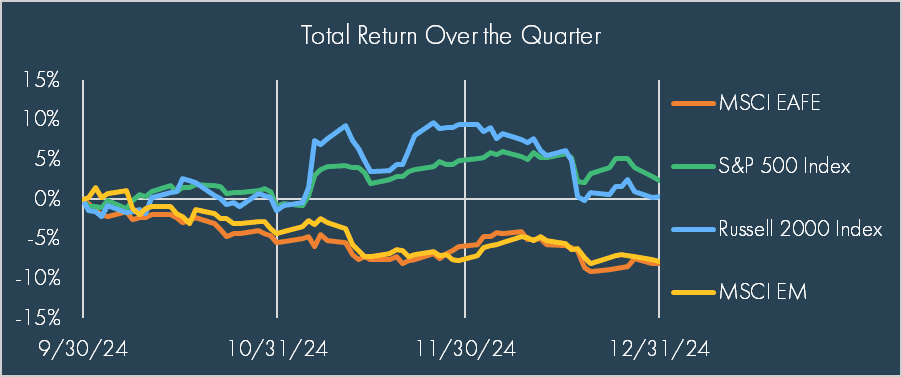

The “fading dominance” in US Large Cap we wrote about for the 3rd quarter reversed in the 4th quarter, ensuring that 2024 was decidedly all about large cap stocks and the dominance of the “Magnificent 7” stocks[1]. The 7-stock cohort was responsible for more than 50% of the S&P 500’s gains in 2024, and it’s a familiar story as the tech sector continued to be buoyed by advancements in artificial intelligence with significant capital flowing into AI-focused startups and publicly traded companies.

There was a noticeable divergence between US and non-US equities over the quarter, as non-US equities faced headwinds from rising rates strengthening the US dollar. The trend continued into November, as Donald Trump’s victory boosted investors’ optimism for US equities and crypto, while sending non-US equities lower on tariff concerns. December was mostly negative across the board, as higher rates all but erased small cap’s gains in November, though non-US equities held steady in December as some initial tariff concerns eased.

Source: Bloomberg as of December 31st, 2024; please see important disclosures at the end of this material.

Fixed Income assets did not fare much better, since prices fall as yields rise. The Bloomberg Aggregate, up nearly 5% on the year heading into the fourth quarter, dropped more than 3% over the quarter, bringing its total return for the year to a paltry 1.25%. This was primarily driven by an increase in yields on longer-maturity bonds while shorter-dated yields fell lower as the Fed cut rates.

Summary

2024 was a dynamic year for investments, with both opportunities and challenges across global markets, but a key theme underlying markets was strength amidst volatility. Despite significant fluctuations due to geopolitical tensions and shifts in monetary policy around the world, major equity indices like the S&P 500 and MSCI World Index ended the year with strong gains, private equity saw a meaningful pick up in deal flow, and higher yields offered attractive opportunities for income-focused investors. There are risks ahead to be sure, but as we saw in 2024, a balanced portfolio across asset classes and regions remained key to managing risks. 2025 will bring its fresh set of challenges and we’ll continue to navigate them with the highest level of care and attentiveness – focusing on the right mix of quality companies, real assets, and income generating assets for every client.

CONTRIBUTORS

Andrew Kelsen, Chief Investment Officer

Chris Kamykowski, CFA, CFP® – Head of Investment Strategy and Research

Rich McDonald, MBA – Head of Portfolio Management and Fixed Income

Tim Side, CFA – Investment Strategist

DISCLOSURES

© 2025 Advisory services offered by Moneta Group Investment Advisors, LLC, (“MGIA”) an investment adviser registered with the Securities and Exchange Commission (“SEC”). MGIA is a wholly owned subsidiary of Moneta Group, LLC. Registration as an investment adviser does not imply a certain level of skill or training. The information contained herein is for informational purposes only, is not intended to be comprehensive or exclusive, and is based on materials deemed reliable, but the accuracy of which has not been verified.

Trademarks and copyrights of materials referenced herein are the property of their respective owners. Index returns reflect total return, assuming reinvestment of dividends and interest. The returns do not reflect the effect of taxes and/or fees that an investor would incur. Examples contained herein are for illustrative purposes only based on generic assumptions. Given the dynamic nature of the subject matter and the environment in which this communication was written, the information contained herein is subject to change. This is not an offer to sell or buy securities, nor does it represent any specific recommendation. You should consult with an appropriately credentialed professional before making any financial, investment, tax or legal decision. An index is an unmanaged portfolio of specified securities and does not reflect any initial or ongoing expenses nor can it be invested in directly. Past performance is not indicative of future returns. All investments are subject to a risk of loss. Diversification and strategic asset allocation do not assure profit or protect against loss in declining markets. These materials do not take into consideration your personal circumstances, financial or otherwise.

DEFINITIONS

The S&P 500 Index is a free-float capitalization-weighted index of the prices of approximately 500 large-cap common stocks actively traded in the United States.

The Russell 2000® Index is an index of 2000 issues representative of the U.S. small capitalization securities market.

The MSCI EAFE Index is a free float-adjusted market capitalization index designed to measure the equity market performance of developed markets, excluding the U.S. and Canada.

The MSCI Emerging Markets Index is a float-adjusted market capitalization index that consists of indices in 21 emerging economies.

Bloomberg U.S. Treasury Bond Index includes public obligations of the US Treasury, i.e. US government bonds. Certain Treasury bills are excluded by a maturity constraint. In addition, certain special issues, such as state and local government series bonds (SLGs), as well as U.S. Treasury TIPS, are excluded.

The Bloomberg U.S. Aggregate Bond Index is an index, with income reinvested, generally representative of intermediate-term government bonds, investment grade corporate debt securities and mortgage-backed securities.

The Bloomberg US Corporate High Yield Bond Index measures the USD-denominated, high yield, fixed-rate corporate bond market. Securities are classified as high yield if the middle rating of Moody’s, Fitch and S&P is Ba1/BB+/BB+ or below. Bonds from issuers with an emerging markets country of risk, based on the indices’ EM country definition, are excluded.

The FTSE Nareit All Equity REITs Index is a free-float adjusted, market capitalization-weighted index of U.S. equity REITs. Constituents of the index include all tax-qualified REITs with more than 50 percent of total assets in qualifying real estate assets other than mortgages secured by real property.

The S&P Global Listed Infrastructure index measures the performance of global companies that are engaged in infrastructure and related operations. It provides liquid and tradable exposure to 75 companies from around the world that represent the listed infrastructure universe. To create diversified exposure, the index includes three distinct infrastructure clusters: utilities, transportation and energy.

[1] The Magnificent 7 refers to the following seven stocks: Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia, and Tesla