Introduction

When “decades happen in weeks”, even the past quarter’s events can seem like old news already. While this is a first quarter update, the seismic shock from President Trump’s tariff announcements on “Liberation Day” in early April requires we provide a more recent assessment and overview of market moves. It is important to note amidst the chaos that the startling shift in sentiment, economic outlook and fear is not unusual when markets tank over a short time frame. Unlike past shocks, however, the catalyst today for the turmoil in markets is not overvaluations in non-profitable companies like 2000, massive deleveraging on the back of a housing market collapse in 2008, or a global pandemic like 2020. No, we are looking at political shock to the system via Presidential trade policy which deserves some space alongside thoughts on the first quarter.

Economic Update

The first quarter saw a shift from the US exceptionalism narrative to one now witnessing meaningfully higher expectations for a potential recession, as companies have been forced to write and rewrite the playbook for managing the Trump administration’s tariff policy. Coming into the year, economic forecasts for 2025 were of the goldilocks / soft-landing variety. Consensus estimates for recession risk probability hovered around 15-20% (a standard level in any given year), but that has now risen sharply to anywhere from 45% to 60% for many market strategists. US growth forecasts are now impacted by a potential rise in unemployment, as businesses respond to potentially higher input prices, supply chain shocks, and most importantly, to cautious consumers scaling back on spending – the core driver of the US’s economic strength in recent years.

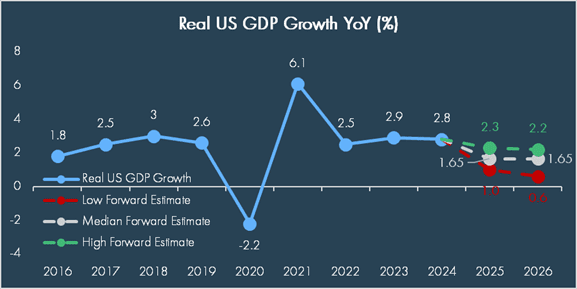

Alleviating this concern is tough for the Fed, as they try to balance their dual mandate of full employment and price stability while being constrained by elevated inflation levels. Supportive, counter-cyclical fiscal policy is also being constrained as sizable deficits have made fiscal hawks wary of any spending increases, though as we write, Congress appears to have completed a reconciliation process, a procedural step that takes them closer to passing new budget measures. All that said, as the chart below illustrates, economic forecasts for 2025 (updated since April 2nd) still show a median expectation for 1.65% real growth in US GDP, with the low-end estimate holding steady at 1.0%.

Despite the upheaval in outlooks, a soft landing is a base case for 2025. This does not mean a recession is avoided, a contraction is seen as highly possible, but the overall degree to which a recession is expected to impact real GDP growth remains on the fairly mild side.

As we noted in our blog post in late March, sentiment and hard data move at different paces which means they may stoke conflicting conclusions on the state of the economy. On the soft side of the equation, consumer sentiment understandably fell off a cliff over the first quarter while near-term inflation expectations rose and business optimism reversed course; this was likely driven by trade uncertainty, which also skyrocketed following President Trump’s initial tariff announcements in early February. In short, forward-looking survey results (soft data) did not appear to bode well for growth expectations, and as we write, preliminary numbers for April show further deterioration.

On the other hand, hard data, whose readings lag behind sentiment-oriented readings, still showed signs of resiliency, which may not yet be factoring into expectations for an economic contraction: payrolls have shown strength with 228K jobs added in March, above expectations; consumer spending growth is shaky, but has not fallen off; and earnings growth was robust in the first quarter, though estimates are obviously coming down as we enter earnings season. A key issue with hard data is its backward-looking nature which means events or decisions today are not showing up yet in the data. Nonetheless, while we could see meaningful short-term changes ahead, the economy’s starting point appears to be strong enough to weather an economic contraction, though weathering a prolonged economic slowdown is another thing altogether.

So where are we now?

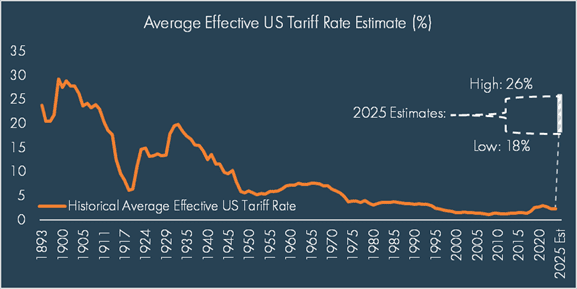

On April 2nd, President Trump announced a 10% universal tariff on all imports in addition to reciprocal tariffs on certain countries to gain leverage in negotiations, generate revenue, and rebalance trade in the US’s favor. Estimates varied, but as stated, these tariffs were expected to bring the US’s effective tariff rate on imports to somewhere between 18-26% – a level generally viewed as a worst-case scenario by markets leading up to the announcements. (A more detailed analysis of the announcement can be found in our Liberation Day blog post ).

As we write, President Trump has announced a 90-day pause on the reciprocal tariffs, though the universal 10% rate remains in place. The exception to this pause is China, where trade war tensions have escalated such that the US now has a 145% tariff on Chinese imports while China has an 125% tariff on US imports. Notably, given the magnitude of US imports from China, these current tariff levels are estimated to raise more revenue than all of the original reciprocal tariffs combined.

The fluidity of the situation cannot be overstated. While there are many unknowns, we can ultimately take some comfort that the US came into the quarter in a position of general strength. That strength can only last so long in the face of extreme uncertainty, but even so, it may provide some support should the economy tip into a contraction or even recession. Stay tuned.

Markets

We’ll begin with a brief recap of the quarter:

January: After a rough start to the year, US equities entered a risk-on rally alongside robust bank earnings and falling rates. However, as the month wrapped up, the rally in large cap was interrupted as DeepSeek made its presence known, upending expectations on recent winners from the boom in artificial intelligence.

February: A reversal in the momentum trade sent US stocks mostly lower in February as the combination of a Fed on pause, weaker macro data, trade policy uncertainty, and elevated valuations drove a rotation out of US equities and into non-US equities and other asset classes. Concerns around the capex spend on artificial intelligence, particularly by the famed Magnificent 7, drove a pullback in tech stocks with the Nasdaq Composite down nearly 4% on the month.

March: Policy uncertainty and recession risks were the key themes in March as investors looked ahead to “Liberation Day” on April 2nd. US stocks continued to underperform global equities, particularly within US Large Cap Growth. With the Fed continuing to remain on hold, US Small Cap stocks also underperformed given their susceptibility to higher rates and less pricing power in a trade war environment. Non-US equities held strong through most of the month, though they pulled back near the end of the month as President Trump’s tariff narrative gained steam.

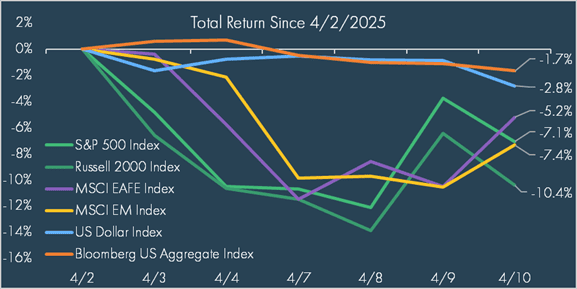

That all said, investors seem to have moved past the first quarter with Liberation Day’s collateral impact very much on investors’ minds. As we write, markets are still on edge, fixated on every comment, online post, reaction, etc. from the various stakeholders in this tariff battle. We have seen dramatic falls and equally dramatic swings skyward in both equity prices and fixed income rates while volatility levels have been sent to levels not seen since March of 2020 – happy five-year anniversary!

Reactions have been quite binary, almost entirely related to President Trump’s comments (or lack thereof). Everchanging assessments of the impact of tariffs on the economy; negotiation and/or retaliations by trading partners, and technical flows have all had an impact as well. As an example, April 9th saw equities rebound strongly on news of a 90-day pause on reciprocal tariff implementation (absent China) with the NASDAQ up 12%, S&P 500 up nearly 10% and Russell 2000 (small caps) up nearly 9% on the news. To be sure, a 10% reciprocal tariff floor remains in place during this period though as well as sectoral tariffs for pharmaceuticals and semiconductors, which up to this point, have been spared.

Bond markets have also been on a roller coaster with the 10-year Treasury whipsawed between lower yields on slower growth concerns and expectations for Fed easing, to higher yields as trade unwinding, federal deficits, and the dollar’s safe haven status came under scrutiny.

Importantly, we continued to see diversification working as defensive assets provided protection from the broader equity market selloff.

Summary

Pause or no pause in tariffs, the last week has upended certainty to a degree that business and consumer behavior will be altered. Even if the worst is behind us, there remains a long way to go to recover from the market drawdown. Questions remain on whether a sustained recovery is impaired given the degree and extent of concerns about shifting policy. There will be a lasting effect on consumers and businesses given the recent uncertainty which could drag on sentiment or at minimum, lead to ongoing skepticism.

Whenever we enter periods of extreme uncertainty, it is often best to take a step back and evaluate the big picture. At Moneta, while we cannot predict the timing or nature of a drawdown, we do know that they will happen, and therefore we aim to build resilient portfolios that enable clients to achieve their long-term goals even through market volatility. Staying with the long-term plan is critical in times like these – making decisions based on fear is often when permanent impairment of capital occurs, while long-term growth of wealth is made from a disciplined process. Consider muting CNBC and Fast Money. Watch this play out and think about rebalancing. Stay the course.

DISCLOSURES

© 2025 Advisory services offered by Moneta Group Investment Advisors, LLC, (“MGIA”) an investment adviser registered with the Securities and Exchange Commission (“SEC”). MGIA is a wholly owned subsidiary of Moneta Group, LLC. Registration as an investment adviser does not imply a certain level of skill or training. The information contained herein is for informational purposes only, is not intended to be comprehensive or exclusive, and is based on materials deemed reliable, but the accuracy of which has not been verified.

Trademarks and copyrights of materials referenced herein are the property of their respective owners. Index returns reflect total return, assuming reinvestment of dividends and interest. The returns do not reflect the effect of taxes and/or fees that an investor would incur. Examples contained herein are for illustrative purposes only based on generic assumptions. Given the dynamic nature of the subject matter and the environment in which this communication was written, the information contained herein is subject to change. This is not an offer to sell or buy securities, nor does it represent any specific recommendation. You should consult with an appropriately credentialed professional before making any financial, investment, tax or legal decision. An index is an unmanaged portfolio of specified securities and does not reflect any initial or ongoing expenses nor can it be invested in directly. Past performance is not indicative of future returns. All investments are subject to a risk of loss. Diversification and strategic asset allocation do not assure profit or protect against loss in declining markets. These materials do not take into consideration your personal circumstances, financial or otherwise.

DEFINITIONS

The S&P 500 Index is a free-float capitalization-weighted index of the prices of approximately 500 large-cap common stocks actively traded in the United States.

The Russell 2000® Index is an index of 2000 issues representative of the U.S. small capitalization securities market.

The MSCI EAFE Index is a free float-adjusted market capitalization index designed to measure the equity market performance of developed markets, excluding the U.S. and Canada.

The MSCI Emerging Markets Index is a float-adjusted market capitalization index that consists of indices in 21 emerging economies.

Bloomberg U.S. Treasury Bond Index includes public obligations of the US Treasury, i.e. US government bonds. Certain Treasury bills are excluded by a maturity constraint. In addition, certain special issues, such as state and local government series bonds (SLGs), as well as U.S. Treasury TIPS, are excluded.

The Bloomberg U.S. Aggregate Bond Index is an index, with income reinvested, generally representative of intermediate-term government bonds, investment grade corporate debt securities and mortgage-backed securities.

The Bloomberg US Corporate High Yield Bond Index measures the USD-denominated, high yield, fixed-rate corporate bond market. Securities are classified as high yield if the middle rating of Moody’s, Fitch and S&P is Ba1/BB+/BB+ or below. Bonds from issuers with an emerging markets country of risk, based on the indices’ EM country definition, are excluded.

The FTSE Nareit All Equity REITs Index is a free-float adjusted, market capitalization-weighted index of U.S. equity REITs. Constituents of the index include all tax-qualified REITs with more than 50 percent of total assets in qualifying real estate assets other than mortgages secured by real property.

The S&P Global Listed Infrastructure index measures the performance of global companies that are engaged in infrastructure and related operations. It provides liquid and tradable exposure to 75 companies from around the world that represent the listed infrastructure universe. To create diversified exposure, the index includes three distinct infrastructure clusters: utilities, transportation and energy.