Quarterly Letter

“The stock market is a great device for transferring money from the impatient to the patient.”

– Warren Buffett

As we write this commentary in early April 2025, President Trump has just announced the most significant tariffs on imports in U. S. history. The U.S. stock market is responding with a pronounced thumbs down. It seems concerns are not just with tariffs, but with the aggressive new approaches to reining in the federal bureaucracy, management of the IRS, and FBI, oversight of healthcare policy, and so on. All this in just a few months.

In the investment world, the opposite of uncertainty is not certainty, it is confidence, and what is happening with global markets is a reaction to uncertainty. How will other countries react to new tariffs from the United States? Are current tariff rates negotiating plays, or long-term economic sanctions on our trading partners? Will tax relief in upcoming legislation offset some of the negative impact of tariffs? Will the Fed lower interest rates to help stimulate the worried U.S. consumer, or will tariffs drive inflation higher and cause the Fed to postpone interest rate reduction plans?

Answers to these and other questions are unknown – it is complete speculation at this point. However, there are two obvious results: rapidly shrinking U.S. economic growth for this year and a cratering U.S. stock market this spring.

To be clear, we are not advocates for the tariff policies being imposed and wish a different approach had been taken to address what are some legitimate concerns over trade. We see no historical precedent that suggests this current tariff initiative will be a winning strategy. The blended tariff rate of 25-30% is higher than almost anyone thought it would be, and arguably the highest overall in U.S. history. Without modifications, such tariffs will likely result in slower corporate earnings growth, higher inflation and declining stock prices. However, we also recognize that none of us knows the real endgame with tariffs for the Trump administration. Our guess is that much of what they are doing is posturing – a shot across the bow, so to speak, to get everyone’s attention prior to formal negotiations. If so, any negotiated compromise would be a positive for markets. We also know the average stock is well-off its fifty-two-week high, meaning current prices relative to long-term earnings potential are perhaps much more attractive than they were just weeks ago. There are many great companies that will get through this just fine, and it is our job to find those opportunities and take advantage of the temporary adjustment.

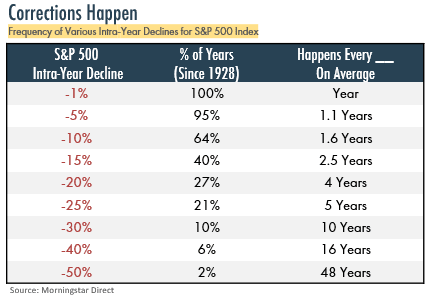

The U.S. has had twenty-one declines of ten percent or more in the S&P 500 Index since 1980, and the average intra-year decline is approximately fourteen percent. Thus, the current drop, while frustrating, is not far off what happens in most years for one reason or another. It is also worth noting that there are some things the administration is doing that should be positives for the economy and stock prices. For one, despite soaring tax revenues, the Federal deficit continues to balloon. It is on an unsustainable path and could have dire long-term consequences. The DOGE methodology being deployed to address deficit issues seems to us somewhat fractious and disorderly but hopefully will become more disciplined with time. Second, there is a great likelihood this year for extended tax relief, something to which any stock market generally responds favorably.

In January, we wrote that after two great years it would be prudent for investors to curb their short-term enthusiasm given relatively high stock market valuations. We said the market needed a breather at some point to allow time for earnings to catch up with high valuations. Holy smokes! We should be more careful with our comments. Little did we know how wild the next few months would prove to be, but we will stand by that outlook as it still reflects our viewpoint for the balance of 2025.

Rudyard Kipling wrote, “If you can keep your head while all others are losing theirs… Yours is the Earth and everything that is in it.” Each rough period for stock markets feels different from the last, but it is remarkable how quickly past markets have stabilized. Uncertainty clears after a short time, and the never-ending innovation and productivity growth embedded in the DNA of our economic system marches on. History has always rewarded the patient investor for their discipline, and we expect this time will be no exception.

“If you can keep your head while all others are losing their… Yours is the Earth and everything is in it.”

– Rudyard Kipling

Market Commentary

– Randall Stauder, CFA – Portfolio Strategist

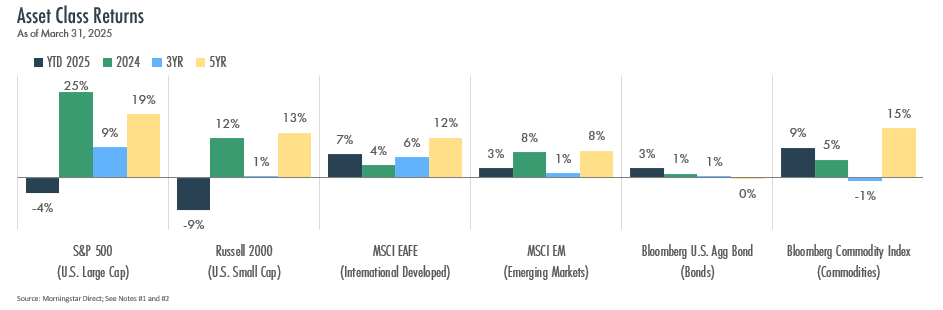

- U.S. stocks pulled back sharply in March as tariff uncertainty, recession worries, and weak consumer sentiment weighed on investor confidence. Despite recent volatility, international equities posted gains and fixed income helped buoy diversified portfolios.

- Bond markets rallied in March, with the Bloomberg U.S. Aggregate Bond Index rising 1.5%, bringing its year-to-date gain to 4.5%, as cooling inflation data and recession concerns pulled long-term yields lower.

- The U.S. economy remains on solid footing—so far. GDP grew 2.3% last quarter, and the labor market remained strong, but a range of soft data indicators suggest the economy may be losing steam. Consumer spending is showing signs of moderating, and sentiment has dropped to a 12-year low.

- The Federal Reserve held rates steady in March and signaled caution, citing elevated inflation and uncertainty around the impact of tariffs and trade policy. Futures markets now reflect rising odds of two cuts later this year, contingent on economic indicators being posted in the months ahead.

Recession Looming?

- The imposition of significant tariffs globally has reignited inflation fears and darkened the outlook for consumer spending and business confidence. The conversation has quickly shifted from if a recession happens to when.

- History shows markets tend to fall before a recession begins and recover well before it ends. Many believe markets began to predict a recession in the first quarter.

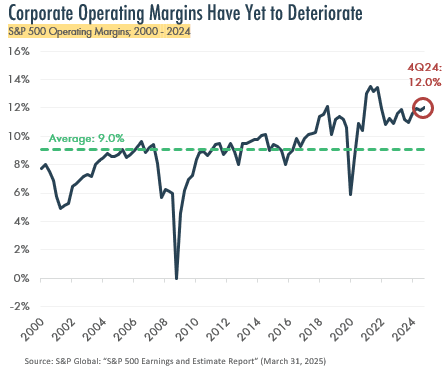

- While recessions are generally associated with consecutive quarters of negative growth and rising unemployment, the latest economic data reflects a mixed picture. S&P 500 operating margins remained elevated at 12.0% through year-end 2024 – well above the long-term average – indicating that corporate profitability has not yet cracked.

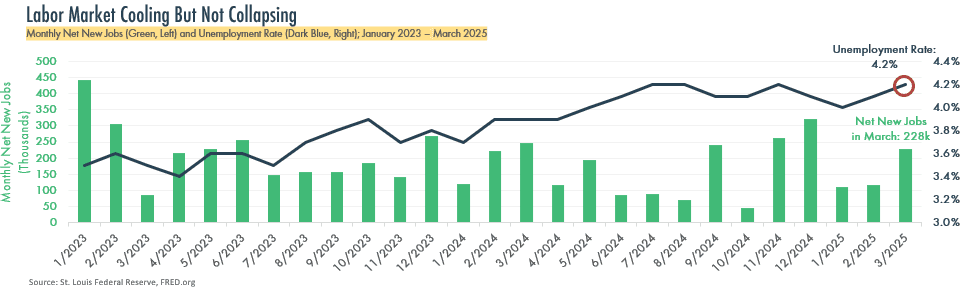

- Meanwhile, the labor market, as highlighted below, is showing signs of cooling, with the unemployment rate edging up to 4.2%.

- Time will tell how the economy and markets will react to the rapidly evolving macro environment, but for now uncertainty rules the narrative, and a further economic slowdown seems the likely outcome.

Yet Another Wall of Worry

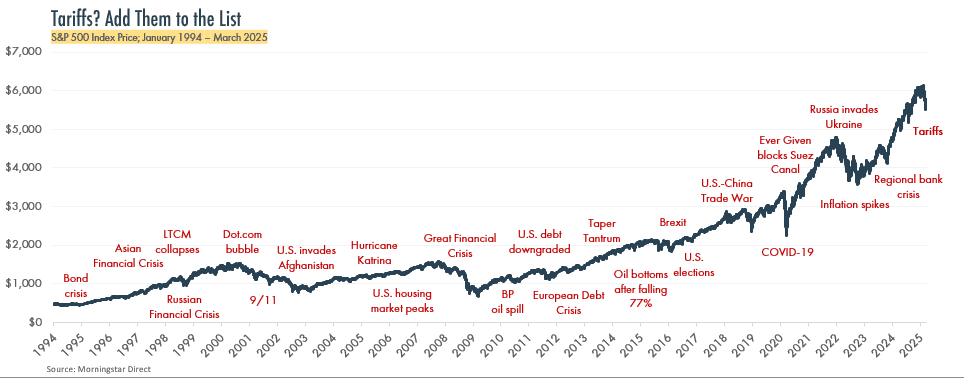

- Each rough period for stock markets feels different, and each creates its own wall of worry. This time it is tariffs. But if history is any guide, markets are remarkably resilient. As shown in the chart of historical crises below, markets have climbed through wars, hurricanes, terror attacks, defaults, pandemics, and more.

- Market declines happen about as frequently as investors tend to forget the last one. Since 1928, the S&P 500 has experienced a 10%+ correction about once every 1.6 years, and a 20%+ “bear market” about once every four years. These pullbacks, while unsettling, are part of the market’s rhythm. The key is not to avoid volatility, but to stay invested through it – because the long-term reward is significant, and timing the market has proven impossible.

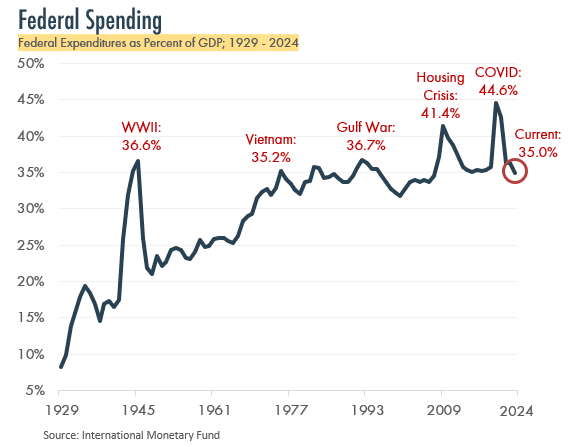

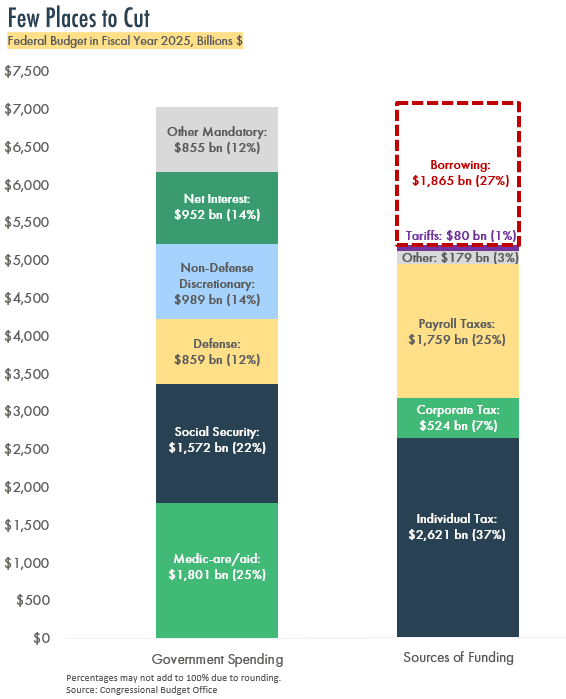

Federal Budgeting

- The DOGE cuts come at a fragile moment – with economic data showing some signs of weakening. While many federal workers may ultimately find more productive private sector roles, the abrupt timing risks a hit to the labor market and consumer spending, two pillars of economic stability.

- The federal deficit does need to be addressed. The interest on the deficit has exploded with higher interest rates in recent years, leading to even more borrowing, as shown at the right. However, whether DOGE tactics prove to be effective over time remains to be seen.

Contributors

© 2025 The Finerty Team

The S&P 500 Index is a free-float capitalization-weighted index of the prices of approximately 500 large-cap common stocks actively traded in the United States. The Bloomberg US Aggregate Bond Index is a broad base, market capitalization-weighted bond market index representing intermediate term investment grade bonds traded in the United States. The Consumer Price Index (CPI) is a measure of the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services.

Advisory services offered by Moneta Group Investment Advisors, LLC, (“MGIA”) an investment adviser registered with the Securities and Exchange Commission (“SEC”). MGIA is a wholly owned subsidiary of Moneta Group, LLC. Registration as an investment advisor does not imply a certain level of skill or training. The information contained herein is for informational purposes only, is not intended to be comprehensive or exclusive, and is based on materials deemed reliable, but the accuracy of which has not been verified.

Trademarks and copyrights of materials referenced herein are the property of their respective owners. Index returns reflect total return, assuming reinvestment of dividends and interest. The returns do not reflect the effect of taxes and/or fees that an investor would incur. Examples contained herein are for illustrative purposes only based on generic assumptions. Given the dynamic nature of the subject matter and the environment in which this communication was written, the information contained herein is subject to change. This is not an offer to sell or buy securities, nor does it represent any specific recommendation. You should consult with an appropriately credentialed professional before making any financial, investment, tax or legal decision. An index is an unmanaged portfolio of specified securities and does not reflect any initial or ongoing expenses nor can it be invested in directly. Past performance is not indicative of future returns. All investments are subject to a risk of loss. Diversification and strategic asset allocation do not assure profit or protect against loss in declining markets. These materials do not take into consideration your personal circumstances, financial or otherwise.