Contributors

Quarterly Letter

“When you got skin in the game, you stay in the game,

but you don’t get a win unless you play in the game.”

-Lin-Manuel Miranda, Hamilton

Despite recent market volatility and a negative quarter, the S&P 500 stock Index has still generated an impressive 70.9 percent three-year cumulative return. Thus, the recent pullback is the type of healthy breather that one should expect from time to time. While not fun, such breathers are generally positive for long-term market participants, as they help keep speculative investors at bay.

To be sure, the first quarter was rocky, as investors digested higher inflation, a war in Europe, spiking interest rates and oil prices jumping from $75 to $110 per barrel. Nonetheless, stock indices were down only slightly, with the S&P 500 off 4.5 percent in the first quarter, and most other stock and bond indices down 5 – 10 percent.

One of our many investment mantras is that stock market corrections are to be expected. Since 1980, the average annual drawdown from peak to trough during any year is 14 percent. Despite that, the markets were up by the end of the year in 32 of those 42 years. In fact, despite four of the largest declines in the S&P 500 Index since the Great Depression, the S&P has averaged close to 12 percent annually since 1980.

Perhaps more intriguing is a study of the results of bad-timing scenarios. For someone who purchased the S&P 500 on October 9th, 2007 – the worst possible day prior to the Great Financial Crisis – their average annual return is now 10 percent. Similarly, if that person had invested on February 19th, 2020 – the worst possible day prior to the Covid epidemic – the annual return is 19 percent. As Charlie Munger once said, “The first rule of compounding is never to interrupt it unnecessarily.”

As anyone who has read these commentaries knows, we tend to be optimistic, but we are not Pollyannas. We understand there is a lot of legitimate worry in today’s markets.

Let’s take a look:

Negatives

- Inflation is back. Last measured at 7.9 percent over the preceding 12 months, the concern is that inflationary environments are frequently followed by recessions. In fact, the Fed has never been able to get inflation under control without causing a recession.

- Retailer surveys show that the economy is slowing. We still are experiencing growth, but the growth rate is fading. It is worse in Europe, where a recession seems probable.

- War in Ukraine. The visuals are disturbing, and the number of lives lost and displaced is heartbreaking. From an economic perspective, the war is disrupting energy supplies in Europe and moving prices higher for many commodities, including corn, wheat and precious metals.

Positives

- U.S. household net worth has surged to all-time records; over $30 trillion greater than pre-Covid figures. Meanwhile, consumer debt is at an all-time low. There is a lot of money to be spent.

- U.S. Jobless Claims figures recently were the lowest since 1969. Even more remarkable, that statistic does not adjust for population change, and in that 50+ year span the workforce has more than doubled.

- Inventories are low. There has been a surge in orders across all industries to meet demand. Vehicle production, for example, has hovered around nine million vehicles in each of the past four quarters. Next quarter, consensus estimates predict over eleven million cars will be produced. Profits will follow.

The bottom line is there is a lot of ammunition with which investors could take either a positive or negative stance. As for us, we still see positives outweighing negatives. As Lin-Manuel Miranda so eloquently wrote, we will therefore stay in the game. Worries about a European war and higher inflation, as scary as they seem, are not sufficient reason to flee the stock market. Instead, they are the very reason to own stocks.

Stocks represent companies which have the ability to sustain profitability by increasing productivity, and by raising prices to maintain their margins. It is a strategy that has worked in the past and we firmly believe it will work again. Paraphrasing Robert Frost, “In three words I can sum up everything I have learned about life (or, in our case, the stock market). It goes on.”

Market Commentary

- Stocks finished March on a positive note, despite briefly entering correction territory in February as Russia’s invasion of Ukraine prompted a flight to safety amid geopolitical uncertainty. Large Cap U.S. stocks, as measured by the S&P 500 Index, were down 5% in the first quarter. Meanwhile, International equities fared slightly worse, down 6%.

- Headline CPI (Consumer Price Index) soared to an annualized rate of 7.9% in February, the highest inflation reading since 1982. Unemployment, which surged to 14.8% in April, 2020, continued to improve, falling to just 3.6% in March. The combination of an ultra-tight labor market and inflation prompted the Federal Reserve to raise interest rates by 0.25% in March. The Fed will likely continue to increase rates throughout 2022 as they attempt to cool inflationary pressures.

- Bonds produced losses in the first quarter as the 10-year Treasury yield climbed from 1.52% to 2.38%. Two-year Treasuries jumped from 0.73% to 2.44%. Average mortgage rates are now well over 4.0%, their highest levels since 2018.

- Among the few asset classes in positive territory, Commodities finished the first quarter with double-digit gains, driven by supply shortages which boosted oil, gas and grain prices.

A Lot Can Change In Two Years

- COVID-19 brought world economies to a stand-still in March, 2020. Few predicted the high double-digit returns over the past two years, as shown at the left.

- As illustrated below, Growth stocks soared in the COVID recovery during 2020 and 2021, as many of these companies benefited from the secular trends of an evolving economy, particularly “work-from-home.” Zoom and Peloton, for example, at one point had gained more than 400% and 500%, respectively.

- Meanwhile, many traditional Value stocks felt the brunt of the pandemic, with travel and hospitality perhaps hardest hit as the world stayed home. By 2022, however, Expedia, Occidental Petroleum, and Marriot have surpassed many of the so-called high-flyers on a price and total return basis.

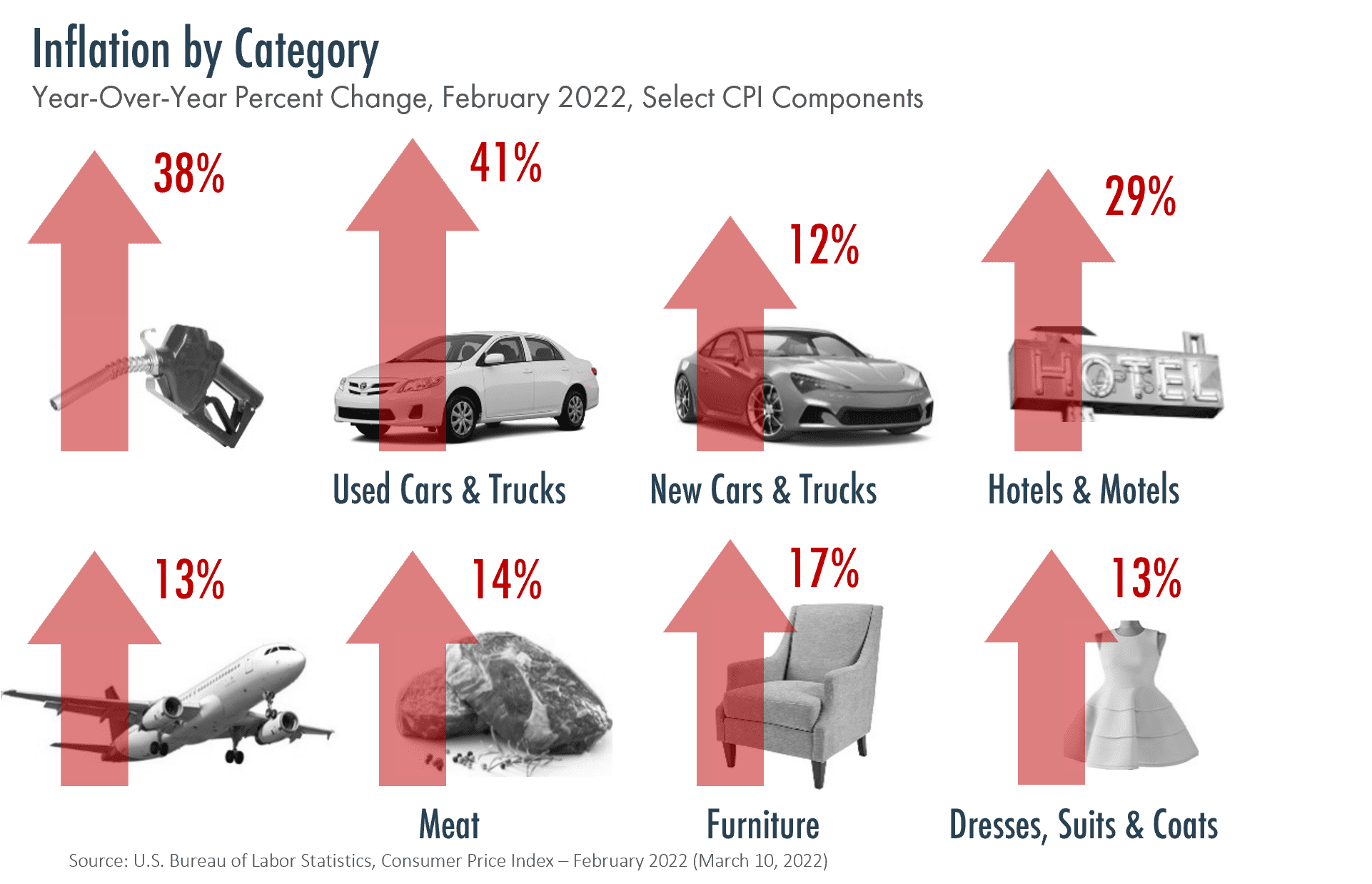

It Is Going to Cost You

- Stocks finished March on a positive note, despite briefly entering correction territory in February as Russia’s invasion of Ukraine prompted a flight to safety amid geopolitical uncertainty. Large Cap U.S. stocks, as measured by the S&P 500 Index, were down 5% in the first quarter. Meanwhile, International equities fared slightly worse, down 6%.

- Headline CPI (Consumer Price Index) soared to an annualized rate of 7.9% in February, the highest inflation reading since 1982. Unemployment, which surged to 14.8% in April, 2020, continued to improve, falling to just 3.6% in March. The combination of an ultra-tight labor market and inflation prompted the Federal Reserve to raise interest rates by 0.25% in March. The Fed will likely continue to increase rates throughout 2022 as they attempt to cool inflationary pressures.

- Bonds produced losses in the first quarter as the 10-year Treasury yield climbed from 1.52% to 2.38%. Two-year Treasuries jumped from 0.73% to 2.44%. Average mortgage rates are now well over 4.0%, their highest levels since 2018.

- Among the few asset classes in positive territory, Commodities finished the first quarter with double-digit gains, driven by supply shortages which boosted oil, gas and grain prices.

The price of oil spiked during the first quarter and has been a significant contributor to inflation in recent months. However, there are a variety of factors in play:

- Monetary and Fiscal Stimulus lifted the economy out of the COVID recession, resulting in elevated stock market portfolios and healthy consumer balance sheets. Corporations have been able to pass on price increases to support their profit margins because consumers are flush with money to spend.

- Labor shortages, for a variety of reasons (including a wave of early retirements among Baby Boomers), has created an extraordinarily tight labor market, which has produced the largest wage gains in decades.

- Low inventories across large swaths of the economy are the result of broad supply-chain disruptions. Inventories take time to rebuild, and basic supply-demand economics indicate that prices increase when supplies are low and demand is strong.

Back to Square One

- The U.S. is roughly 1.5 million jobs away from reaching its pre-pandemic peak set in February, 2020, a remarkable feat considering almost 21 million jobs were lost in the span of two months at the beginning of the pandemic.

- Labor shortages stem from a number of factors, including accelerated retirement among Boomers, COVID-19, and fewer immigrants. The labor shortage problem is contributing to the red-hot inflation figures.

- The shortage of job seekers has forced employers to increase wages significantly to attract and retain talent. Bottom line: there may not be enough population growth in Western countries to slow wage growth in the near-term.

Tighter Monetary Policy

- The Federal Reserve raised interest rates for the first time in more than three years, with a 0.25% hike in March. The Fed will likely continue to aggressively tighten monetary policy in 2022, in a bid to temper surging inflation.

- The Fed plans to raise short-term interest rates, which will trickle through to higher lending rates for businesses and consumers. Higher financing costs cause businesses and households to reduce spending and increase savings, which should decrease demand and result in more attractive prices for goods and services. Accomplishing this without inducing the economy into recession is the challenge and a tight needle to thread.

- Nobody knows how this will play out, but based on prior cycles of policy tightening, the outlook for U.S. stock and bond returns may not be as bleak as one might expect. (See “Rising Interest Rate Environment” chart.)

The S&P 500 Index is a free-float capitalization-weighted index of the prices of 500 large-cap common stocks actively traded in the United States. The Bloomberg US Aggregate Bond Index is a broad base, market capitalization-weighted bond market index representing intermediate term investment grade bonds traded in the United States. The Consumer Price Index (CPI) is a measure of the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services.

Performance returns cited represent past performance, which is not indicative of future returns. Index and/or Style returns reflect total return, assuming reinvestment of dividends and interest. The returns do not reflect the effect of taxes and/or fees that an investor would incur. Investors cannot invest directly in an index. Opinions expressed herein are solely those of the Finerty Team as of the date of this commentary and subject to change without notice. These materials were prepared for informational purposes only based on materials deemed reliable, but the accuracy of which has not been verified. Trademarks and copyrights of materials referenced herein are the property of their respective owners. This is not an offer to sell or buy securities, nor does it represent any specific recommendation. You should consult with an appropriately credentialed professional before making any financial, investment, tax or legal decision. All investments are subject to a risk of loss. Diversification and strategic asset allocation do not assure profit or protect against loss in declining markets. These materials do not take into consideration your personal circumstances, financial or otherwise.

© 2022 Moneta Group Investment Advisors, LLC. All rights reserved. These materials were prepared for informational purposes only based on materials deemed reliable, but the accuracy of which has not been verified. This is not an offer to sell or buy securities, nor does it represent any specific recommendation. You cannot invest directly in an index. You should consult with an appropriately credentialed professional before making any financial, investment, tax or legal decision. Past performance is not indicative of future returns. These materials do not take into consideration your personal circumstances, financial or otherwise.