by Tim Side, CFA – Director of Investment Strategy

A cruel taste of life in Greenland swept across much of the U.S. over the weekend as snowstorms and frigid temperatures caused several deaths, grounded flights, and left hundreds of thousands without power.[1] The so-called pathetic fallacy[2] seems apt in today’s environment, which despite three straight years of double-digit S&P 500 gains, an unemployment rate at 4.4%, and inflation under 3%, an air of doom and gloom persists. There are multiple reasons behind this: an increasingly tumultuous political environment (both at home and abroad), the nature of a “k-shaped” economic environment and an important distinction between inflation and affordability; combined with a natural human negativity bias, a general gloom seems to be in place (sub-zero temperatures certainly don’t help either).

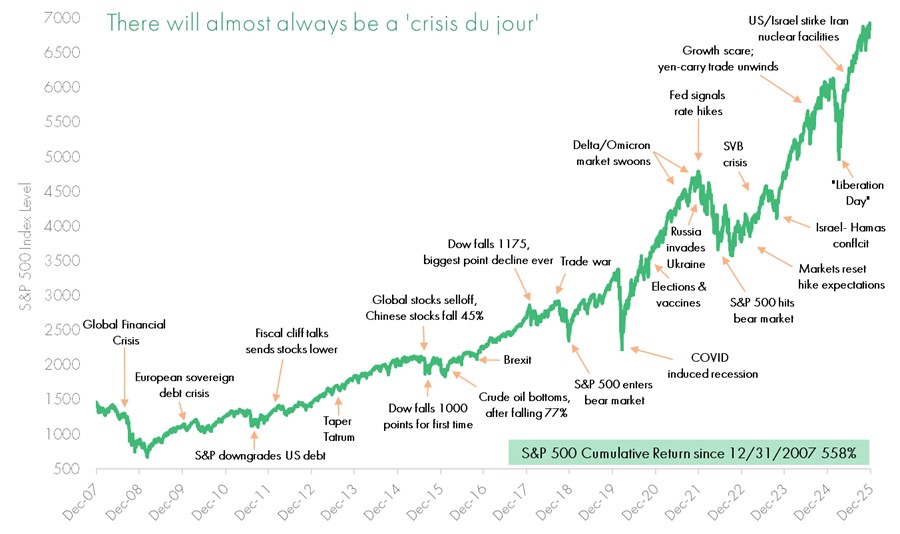

Persistent negative outlooks are “easy” to document and technically rebuff, though it is certainly an art and science to managing behavioral biases. One of our favorite ways of illustrating this is through our “Wall of Worry” chart, which highlights just a small sample of fears and concerns that the S&P 500 has endured over the last 17 years as it returned more than 500% cumulatively.

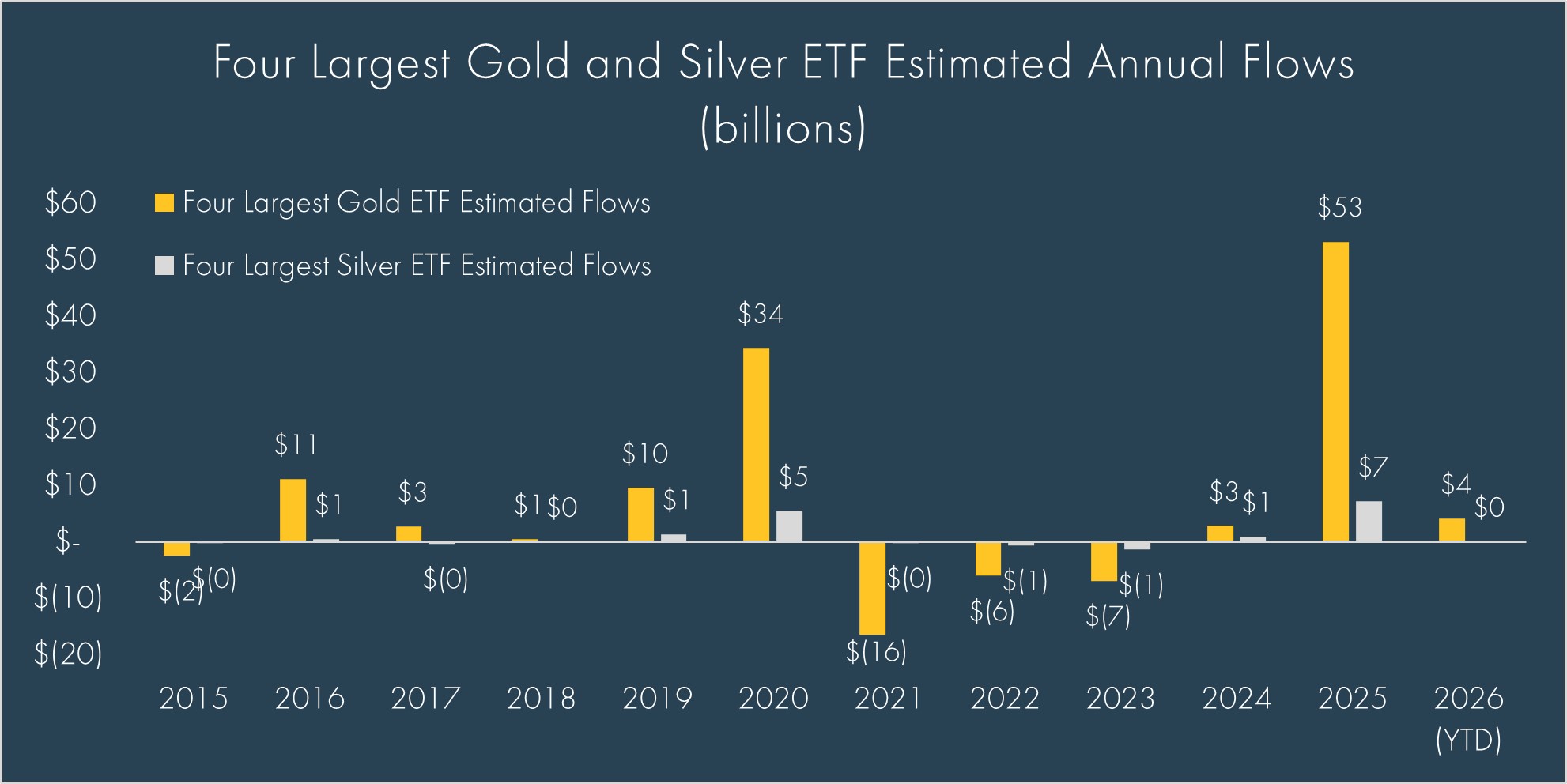

More recent events go beyond a simple chart, especially given the number of developments that have already captured public attention and amplified concerns this month. In early January, the U.S. undertook an unprecedented military operation to capture Venezuela’s leader, Nicolás Maduro, prompting both praise for the overwhelmingly successful and deft mission and debate about geopolitical risk and global stability. Just weeks later, Greenland’s Prime Minister warned residents to prepare for the possibility of a U.S. military invasion as President Trump increased pressure on Denmark to sell Greenland to the U.S., given its geographic importance and vast, largely untapped, resources. At home, Minneapolis has become a focal point of national attention as federal immigration enforcement operations and resulting protests have drawn widespread media coverage and sparked broader debates about governance, law enforcement, and civil unrest. Elsewhere, federal authorities served the Federal Reserve with grand jury subpoenas related to testimony by the Fed Chair and shifting fiscal policy concerns in Japan pushed Japanese bond yields higher. While markets have generally held steady, these unsettling events have been primarily reflected in precious metals, with gold prices surpassing $5,000 per ounce.

We are neither politicians nor journalists. However, we are human, and we empathize with the feeling that the world can feel untethered, and perhaps more so now than ever. We are also investors with a responsibility to help clients achieve their financial goals across multiple market cycles. This responsibility gives us a clear mandate to make objective, dispassionate decisions for what’s best for our client’s portfolios.

So, what do we objectively need to keep in mind?

Although some might say it’s under stress, the rule of law still persists. The Supreme Court is reviewing the legality of Trump’s tariffs. The U.S. did not execute a formal regime change in Venezuela, ala Iraq. Despite the animated bluster, Trump has reiterated that he will not fire Powell nor will the U.S. invade Greenland. Higher Japanese yields indicate a limit to fiscal largess which has been a long-time coming. As painful as government shutdowns may be there is an increased likelihood of a government shutdown this week, as lawmakers on both sides of the aisle need to come together to make a deal.

Another important principle is that risk and return go hand in hand. Gold’s +80% gain and silver’s +250% gain over the last year or so are reflective of central bank purchases and investor concerns and should not be taken lightly. That gold can potentially be a hedge against inflation and a weaker dollar is true, but as long-term investors, we have to consider the historical nature of gold and silver and their boom/bust properties.

As the dollar weakens, some appreciation of these assets makes sense, but the extent of the warning is likely obfuscated by sentiment, making it difficult to know (1) how much additional protection gold could provide in the event of a true risk-off event and (2) where the floor lies once retail demand cools.

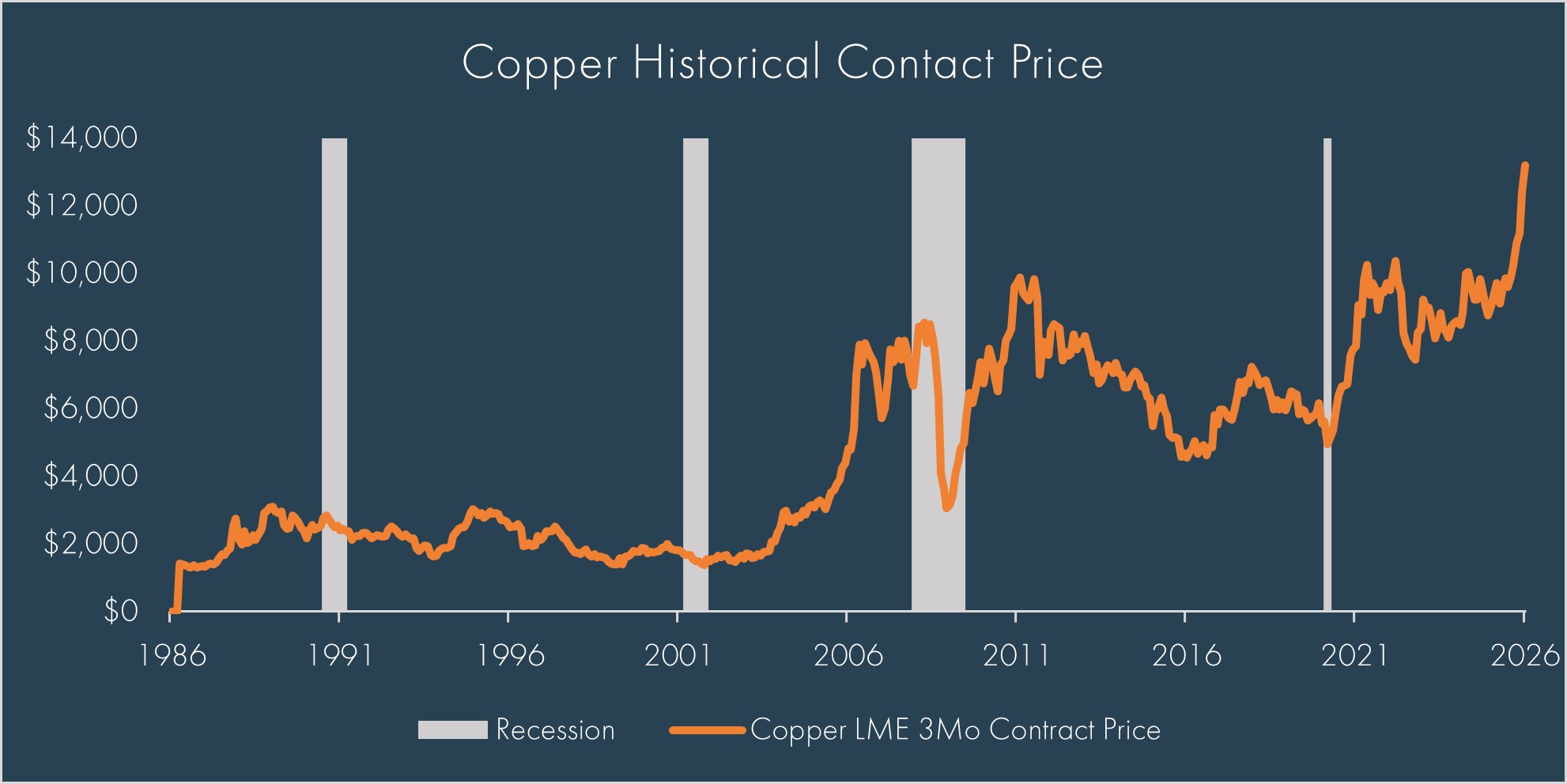

Additionally, the rapid rise of precious metals also has to be reconciled with global equities up +20% over the last year, copper up +40% over the last year, and a U.S. 10-Year Treasury sitting well below the 5% levels touched in late 2023. These coinciding movements could also be a signal that historical correlations between gold/equities and copper/inflation may finally be breaking down for good. We addressed equities and fixed income in our recent quarterly update, but copper is also noteworthy as it’s rise is more an indication of expansion rather than a risk-off environment. Though as with gold and silver, there is a notable boom/bust nature of copper making investment difficult to time.

Lastly, the world is changing. We’ve written about shifting global dynamics, the potential decline of the U.S. dollar, the unsustainable fiscal situation in the U.S., Trump vs. Powell, and the resilience of the U.S. amid policy “missteps”. These are real concerns, and we’re living through many a moment that could shape the global economy for decades. Change can be uncomfortable, but that’s the risk/reward nature of investing. As we noted in our Geopolitics Series (linked above), in the sweep of history, the last 30–40 years of relative peace have been the exception, not the rule.

In periods like this, there’s often a strong urge to act and “not just stand there”, especially when it feels like a freight train may be headed straight for your portfolio. Yet time and time again, we’ve encouraged clients and readers to look past the headlines and stay focused on their long-term goals. Markets have been remarkably resilient, supported by real earnings growth and the potential for meaningful productivity gains from artificial intelligence. We’ll take those wins when they come, knowing that at some point, another painful drawdown will arrive.

The headlines may feel relentless, but successful investing has never required a calm world – it requires a clear plan and the discipline to stick with it. While risks remain, the silver lining is that uncertainty has always been part of the journey, not a reason to abandon it. By focusing on quality, diversification, and patient rebalancing, we can tune out the noise, stay positioned for opportunity, and keep portfolios aligned with long-term financial goals.

[1] https://www.wsj.com/us-news/climate-environment/deadly-winter-storm-disrupts-air-travel-leaves-thousands-without-power-8786db2d?mod=hp_lead_pos3

[2] “Pathetic fallacy” is when a writer gives human emotions to nature or objects (like stormy weather reflecting a character’s sadness).

© 2026 Advisory services offered by Moneta Group Investment Advisors, LLC, (“MGIA”) an investment adviser registered with the Securities and Exchange Commission (“SEC”). MGIA is a wholly owned subsidiary of Moneta Group, LLC. Registration as an investment adviser does not imply a certain level of skill or training. The information contained herein is for informational purposes only, is not intended to be comprehensive or exclusive, and is based on materials deemed reliable, but the accuracy of which has not been verified.

Trademarks and copyrights of materials referenced herein are the property of their respective owners. Index returns reflect total return, assuming reinvestment of dividends and interest. The returns do not reflect the effect of taxes and/or fees that an investor would incur. Examples contained herein are for illustrative purposes only based on generic assumptions. Given the dynamic nature of the subject matter and the environment in which this communication was written, the information contained herein is subject to change. This is not an offer to sell or buy securities, nor does it represent any specific recommendation. You should consult with an appropriately credentialed professional before making any financial, investment, tax or legal decision. An index is an unmanaged portfolio of specified securities and does not reflect any initial or ongoing expenses nor can it be invested in directly. Past performance is not indicative of future returns. All investments are subject to a risk of loss. Diversification and strategic asset allocation do not assure profit or protect against loss in declining markets. These materials do not take into consideration your personal circumstances, financial or otherwise.