By Sarah Bishop, Senior Retirement Plan Advisor – Learn more about our Retirement Plan Consulting Services

The Internal Revenue Service (IRS) announced increases to retirement plan limits for tax year 2025. These cost-of-living adjustments were published on Friday, November 1, 2024. These new limits provide workers with an opportunity for greater savings next year.

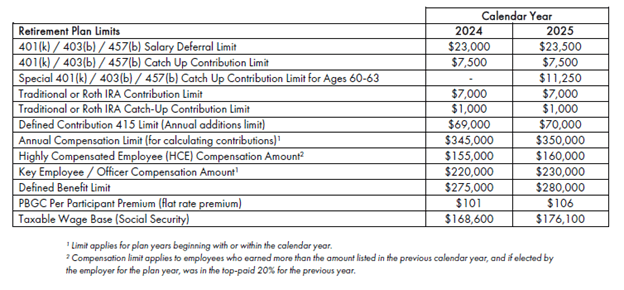

In 2025, workers can contribute $23,500 pre-tax to a 401(k) or similar retirement savings plan – a $500 increase from 2024. Workers aged 50 or older can also contribute $7,500 in catch-up contributions in 2025, which remains unchanged from 2024.

A new catch-up provision under the SECURE 2.0 Act also takes effect in 2025. If permitted under the employer’s 401(k), 403(b), or governmental 457(b) plan, the catch-up limit for participants aged 60-63 will be the greater of $10,000 or 150% of the regular catch-up limit ($11,250 for 2025).

What Does This Mean for You?

If you already maximize your annual contributions and have the ability to save more, you may be able to lower your taxable income by $500 in 2025. If you will attain age 50 in 2025, don’t forget that you’re eligible for the catch-up contribution, an additional $7,500 savings opportunity.

While only pre-tax contributions reduce your current tax burden, the increased limits also apply to Roth contributions.

(Limits for other types of retirement plans will vary. See IRS Notice 2024-80 for details.)

What Do the New Catch-up Rules Under SECURE 2.0 Mean for You?

If you will attain age 60, 61, 62, or 63 during 2025, and your employer offers the additional catch-up under SECURE 2.0, you will be eligible to save an additional $3,750 above the regular catch-up limit ($11,250 in total catch-up).

How Do the Changes in Limits Impact Individual Retirement Accounts (IRAs)?

For those eligible to make contributions to a pre-tax or Roth IRA, the limit remains at $7,000 for 2025 – unchanged from 2024. The age 50 catch-up contribution in these accounts also remains unchanged at $1,000.

Is There a Compensation Limit Associated with These Changes?

The compensation limit for 401(k) or similar retirement savings plans will increase from $345,000 to $350,000. If your income is above this level and your plan matches a percentage of pay, you may also see a greater dollar amount in employer matching contributions for 2025.

Make sure to adjust your payroll deduction in January 2025 to ensure that you are taking advantage of the increased limits.

What Other Changes are Included?

Increases for Health Savings Accounts (HSA) will also take effect in 2025. See the table below for a summary.

Are You a Business Owner Without a Retirement Plan?

Small employers are eligible for enhanced tax credits to offset start up costs associated with sponsoring a retirement plan for their employees.

Employers with 100 or fewer employees may be eligible to claim up to $5,000* in start up tax credits for 3 years when establishing a new retirement plan.

You may also be eligible to claim tax credits up to $1,000* per employee to offset the costs of employer match or profit sharing contributions for 5 years when establishing a new defined contribution retirement plan.

A $500 tax credit is also available for 3 years for including an automatic enrollment provision in your plan.

*Tax credits are calculated based on the number of eligible non-highly compensated employees.

As a business owner, investing in the financial wellness of your workforce is a strategic decision that can directly influence productivity, employee turnover, healthcare costs, and the overall success of your business.

Visit the Finerty Retirement Plan Team’s Wisdom and Wealth webpage to see how Moneta can help with financial wellness and retirement plan education. https://team.monetagroup.com/401k-financial-wellness/

Sources:

Internal Revenue Service –

https://www.irs.gov/pub/irs-drop/n-24-80.pdf

American Retirement Association –

FOR FULL DETAILS ON THE 2025 RETIREMENT PLAN LIMITS, VISIT THE IRS WEBSITE (IRS.GOV). THESE MATERIALS ARE OFFERED FOR GENERAL INFORMATIONAL PURPOSES ONLY AND NOT AS TAX OR LEGAL ADVICE. INFORMATION IS BASED ON SOURCES BELIEVED TO BE RELIABLE BUT THE ACCURACY OF SUCH INFORMATION HAS NOT BEEN INDEPENDENTLY VERIFIED.

© 2024 Advisory services offered by Moneta Group Investment Advisors, LLC, (“MGIA”) an investment adviser registered with the Securities and Exchange Commission (“SEC”). MGIA is a wholly owned subsidiary of Moneta Group, LLC. Registration as an investment adviser does not imply a certain level of skill or training. The information contained herein is for informational purposes only, is not intended to be comprehensive or exclusive, and is based on materials deemed reliable, but the accuracy of which has not been verified.

Trademarks and copyrights of materials referenced herein are the property of their respective owners. Index returns reflect total return, assuming reinvestment of dividends and interest. The returns do not reflect the effect of taxes and/or fees that an investor would incur. Examples contained herein are for illustrative purposes only based on generic assumptions. Given the dynamic nature of the subject matter and the environment in which this communication was written, the information contained herein is subject to change. This is not an offer to sell or buy securities, nor does it represent any specific recommendation. You should consult with an appropriately credentialed professional before making any financial, investment, tax or legal decision. An index is an unmanaged portfolio of specified securities and does not reflect any initial or ongoing expenses nor can it be invested in directly. Past performance is not indicative of future returns. All investments are subject to a risk of loss. Diversification and strategic asset allocation do not assure profit or protect against loss in declining markets. These materials do not take into consideration your personal circumstances, financial or otherwise.